This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Using S&P's sector classification, I take a look at how each one did in 2022, looking at the percent changes in market capitalization: In contrast to 2020, when technology and consumer discretionary firms ran well ahead of the pack, the best performing sectors in 2021 were energy and real estate, two of the biggest laggards in 2020.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. Technology and cyclical companies dominate raw highest risk rankings.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year.

The first is that it was an uneven recovery, if you break stocks down be sector, which I have, for both US and global stocks, in the table below: As you can see, technology was the biggest winner of the year, up almost 58% (44%) for US (global) stocks, with communication services and consumer discretionary as the next best performers.

Price of Risk The drop in stock and bond prices in the third quarter of 2023 can partly be attributed to rising interest rates, but how much of that drop is due to the price of risk changing? below the index value of 4288, confirming my base case conclusion.

The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.” The riskpremium reflects that market participants require compensation for taking on uncertainty. The riskpremium may incorporate factors such as credit risk or market illiquidity.

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equity riskpremium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

By identifying earnings manipulation and guaranteeing more accurate firm values, this clever little technology is here to save the day. A high M-Score could indicate higher risk, warranting a higher discount rate and thus a lower valuation. It's like adding a riskpremium, but based on hard data rather than gut feeling.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Debt breakdown 2.

By focusing so much attention on a small subset of companies, you risk developing tunnel vision, especially when doing peer group comparisons. In the same dataset where I compute historical equity riskpremiums, I report historical returns on corporate bonds in two ratings classes (Moody’s Aaa and Baa ratings).

Having watched Tesla reinvest and grow over the last few years, it is clear to me that the company's been able to generate its growth with far less money invested in plant and more in technology and R&D than a typical auto company. The Market : The US equity market in January 2023 looks very different from the market at the start of 2022.

I would be lying if I said that I have had clarity about Tesla's story over the last decade, because it has so many tangents, distractions and shifts along the way, flirting with narratives about being a battery company, an energy company and a technology company. for mature markets.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

The various problems facing the company led the court to embrace the respondents’ theory that SWS would continue to face an uphill climb given its relatively small size, which prevented it from scaling its substantial regulatory, technological, and back-office costs. Hilltop’s Influence on the Sale Process Rendered Merger Price Unreliable.

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

There are a few arguing that the shift to a technology-based economy has removed inflationary pressures permanently, pointing to the last decade where inflation fears never came to fruition. Consequently, as inflation increases, equity riskpremiums will tend to increase.

Changes in tax regulations, technology advancements, and shifts in customer preferences can impact the future prospects and growth potential of the business. Technology and Infrastructure In today's digital age, the technology and infrastructure employed by a tax preparation business can greatly influence its value.

For much of the last year, I tracked the S&P 500 and the NASDAQ, the first standing in for large cap stocks and the broader market, and the latter proxying for technology and growth stocks, with some very large market companies included in the mix. Riskpremiums No effect or even a decrease. Riskfree rate will rise.

Equipment, Technology, and Infrastructure The quality and condition of equipment, technology, and infrastructure directly influence the value of a disaster restoration business. Stay updated on the latest advancements, changes in regulations, and emerging technologies that can impact the business's value.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. Amanda holds a PhD, dual master’s degrees from Stanford University and dual bachelor’s degrees from the California Institute of Technology.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. at least with technology companies). Me-to-ism : The second and almost as powerful a force in determining debt policy is peer group behavior.

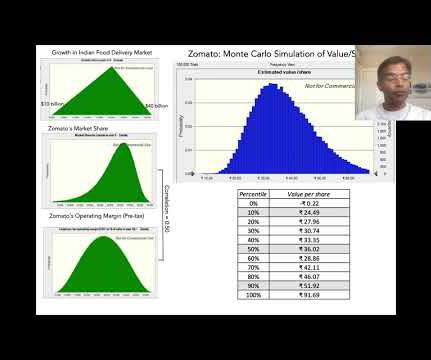

It would be churlish on my part to take issue with the bloat and selective disclosure in Zomato's prospectus, since they are following the script that other technology companies around the world have written for going public, but it is frustrating to read through 420 pages, and still be left in the dark on key numbers.

The last decade, with it influx of user based companies and technology platforms forced me to think seriously about how to value a user, subscriber or rider and extrapolate from there to company value. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

I use the data through the end of 2023 to compute all three measures for every company, and in my first breakdown, I look at these risk measures, by sector (globally): Utilities are the safest or close to the safest , on all three price-based measures, but there are divergences on the other risk measures.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

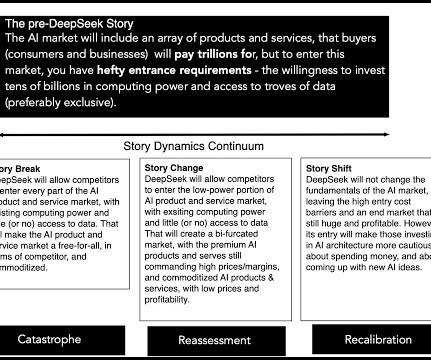

The AI story, before DeepSeek The AI story has been building for a while, reflecting the convergence of two forces in technology - more computing power, often in smaller and smaller packages, and the accumulation of data, on technology platforms and elsewhere. What is it that makes the DeepSeek story so compelling?

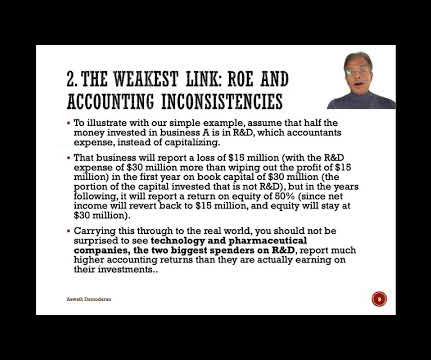

Carrying this through to the real world, you should not be surprised to see technology and pharmaceutical companies, the two biggest spenders on R&D, report much higher accounting returns than they are actually earning on their investments.

Breaking down the remaining sectors, real estate and utilities are the heaviest users of debt, and technology and health care the lightest. Reda estate and utilities continue to look highly levered, and technology carries the least debt burden.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. That said, to value companies today, I have no choice but to bring in the economics and politics of the world that these companies inhabit.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content