This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

Definition of Equity RiskPremium. It is the difference between expected returns from the stock market and the expected returns from risk-free investments. What Impacts the Equity RiskPremium? How Do You Calculate Equity RiskPremium? Why is the Equity RiskPremium Important?

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

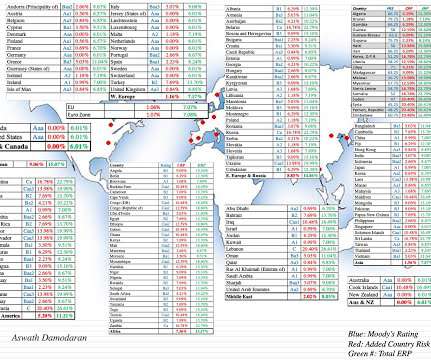

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

The premium that investors demand over and above the riskfreerate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

It helps an investor understand what to expect to earn in relation to the risk-freerate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-freerate by buying the risk-free asset. How Do You Calculate the Capital Asset Pricing Model? E(r) = Rf + ??(Rm

If, on the other hand, investors are risk neutral, the price of risk will be zero, and investors will buy risky business, stocks and other investments, and settle for the riskfreerate as the expected return. Estimation Approaches Why is it so difficult to estimate an equity riskpremium?

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Beyond the 10-year maturity, the slope of the yield curve actually flattened out, with the difference between the 30-year rate and the 10-year rate declining by 0.34%. Note that the decrease in default spreads, at least for the lower ratings, mirrors the drop in the implied equity riskpremium during the course of 2021.

The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. Investors construct portfolios with unsystematic risks, which are well-diversified to reduce total portfolio risk. Inflation rate: ß = 0.6, The risk-freerate is 5%.

Price of Risk The drop in stock and bond prices in the third quarter of 2023 can partly be attributed to rising interest rates, but how much of that drop is due to the price of risk changing? below the index value of 4288, confirming my base case conclusion.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

The Codification often provides guidance on how to select a discount rate for a particular area of accounting. The Codification may require the use of a risk-freerate in some places and a risk-adjusted rate in others. The riskpremium may incorporate factors such as credit risk or market illiquidity.

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-freerate, cost of equity, or cost of debt, are used contextually in financial analysis.

Note that in all three cases, it is not the Fed that is driving rates, but what is happening to inflation. As the inflation bogeyman returns, the worries of what may need to happen to the economy to bring inflation back under control have also mounted.

The answer, to me, seems to be obviously yes, though there are still some who argue otherwise, usually with the argument that country risk can be diversified away. In that post, I computed the equity riskpremium for the S&P 500 at the start of 2021 to be 4.72%, using a forward-looking, dynamic measure. as mature markets.

The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors. That view has never made sense, because central banking power over rates is at the margin, and the key fundamental drivers of rates are expected inflation and real growth.

Next, we need to estimate the risk-freerate and the riskpremium for each risk factor. Let's say the risk-freerate is 3%, the riskpremium for market risk is 5%, the riskpremium for industry risk is 4%, and the riskpremium for country risk is 2%.

Note also that during 2022 and 2023, the movements in these government bond rates mimic the US treasuries, rising strongly in 2022 and declining or staying stable in 2023.

We’ve added a ‘date picker’ across key resources sections, allowing you to examine risk-freerates, corporate tax rates, market riskpremium, and country ratings across any historic date you select. Resources Section Date Improvement: What? Why Important?

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-freerate. Suitability and limitation.

According to the CAPM model - the return required by the shareholders can be described using the following equation: Cost of Equity = Risk-FreeRate + Beta x RiskPremium. That is - if you do not know the beta, you cannot calculate the equity cost and, as a result, not the weighted average equity price.

Market Risk-FreeRate: Beta calculations often involve comparing the asset’s returns to a risk-freerate, such as the yield on a government bond with a similar maturity. Ensure that you have access to accurate and up-to-date data for the chosen benchmark index.

Risk : When I valued Tesla last in early 2020, I used a cost of capital of 7%, reflecting a riskfreerate of 1.75% and an equity riskpremium of 5.2% for mature markets.

As I noted in my last post , rising riskfreerates and equity riskpremiums have pushed up the costs of equity for all companies, and Tesla is not only no exception but is perhaps even more exposed as an above-average risk company.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Interest Rates : The most direct link between inflation and equity value is through the riskfreerate (interest rate) that forms the base for the expected returns that investors demand for investing in a company's equity, and for lending it money.

The first of the is as companies scale up, there will be a point where they will hit a growth wall, and their growth will converge on the growth rate for the economy. In short, I am assuming that the price cuts and cost pressures of the fourth quarter are more representative of what Tesla will face in the future, as competition steps up.

the returns you can make on investments of equivalent risk, and that game became a lot more difficult to win in 2022. Conclusion If 2022 was a reminder to investors that the end game for every business is to not just generate profits, but to generate enough profits to cover its opportunity costs, i.e,

Dividend Discount Model, Part 4: Present Value of Terminal Value and Dividends Since the Dividend Discount Model is based on Equity Value, not Enterprise Value, the Discount Rate is the Cost of Equity: Risk-FreeRate + Equity RiskPremium * Levered Beta.

Rf = Risk-freeRate. Rm – Rf) = Equity Market RiskPremium. Cp = Cost of Equity Premium. Now, we need to calculate the discount rate. . Riskfreerate (can use 10y Treasury). Ce = Cost of Equity. B = Beta. (Rm We will use the CoE and WACC formulas described above. .

Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

Risk Differences across Countries In this final section, I will look risk differences across countries, both in terms of why risk varies across, as well as how these variations play out as equity riskpremiums.

Equity Risk across Countries Default risk measures how much risk investors are exposed to, when investing in bonds issued by a government, but when you own a business, or the equity in that business, your risk exposure is not just magnified, but also broader.

The effects of inflation show up first as higher riskfreerates , across currencies, and next in higher riskpremiums, with both equity riskpremiums and default spreads rising. As a company with the bulk of its business in India, Zomato again is more exposed to these developments.

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equity riskpremium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic riskfreerate of 8.7%. The Stocks Story As treasury rates have risen in 2021, equity markets have been surprisingly resilient, with stocks up during the first three months.

Computing the returns in real terms , by taking out inflation in each year from that year's returns, and recomputing the equity riskpremiums: Download historical data Note that the equity riskpremiums move only slightly, because inflation finds its way into both stock and treasury returns.

Using a different lexicon, the price of risk in the bond market decreased during the course of the year, and if you relate that back to my second data update, where I computed a price of risk for equity markets (the equity riskpremium), you can see the parallels.

Discount Rates / RiskPremiums: The discount rate used in DCF analysis (often the WACC) incorporates elements sensitive to market conditions. [21] 21] [22] [24] [27] The cost of equity component includes the market riskpremium the excess return investors expect for investing in the broader market over a risk-freerate.

10] , [23] , [2] Discount Rate: The rate used to discount future cash flows is typically the cost of equity, calculated via the Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-FreeRate + Beta * Market RiskPremium. [23] 23] Risk-FreeRate: Tied to government bond yields (e.g.,

I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies. The logical step in looking across countries is measuring risk in countries, and bringing that risk into your analysis, by incorporating that risk by demanding higher expected returns in riskier countries.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content