This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

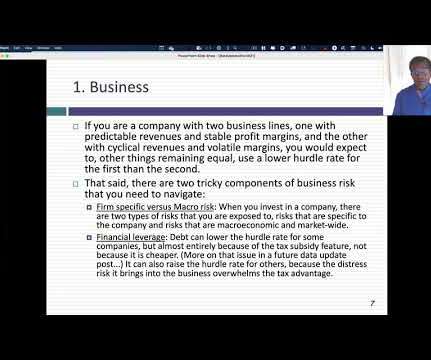

Company-specific risk is not an ideal name for this risk. All firms face company-specific risks, many of which are somewhat similar across industries and companies. For example, how many firms have you valued that had to deal with the risk of customer concentration? Is anything “company-specific” per se?

Definition of Equity RiskPremium. It is the difference between expected returns from the stock market and the expected returns from risk-free investments. What Impacts the Equity RiskPremium? How Do You Calculate Equity RiskPremium? Why is the Equity RiskPremium Important?

Understanding risk factors is essential in determining how a business will be valued. Let’s consider what your business-owning clients need to know about company-specific risks and how they come into play when it’s time for a business valuation.

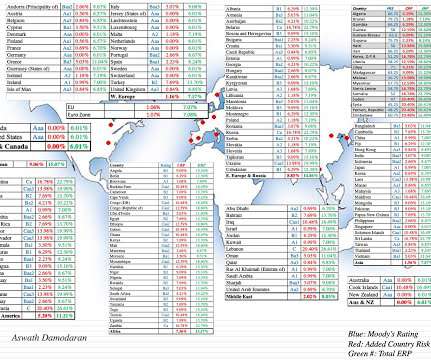

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

The premium that investors demand over and above the risk free rate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

In computing this implied equity riskpremium for the S&P 500, I start with the dividends and buybacks on the stocks in the index in the most recent year (which is known) and assume that they grow at the rate that analysts who follow the index are projecting for the next five years.

If a large shareholder or a group of investors becomes concerned with the firm’s operations and management, and takes legal steps to assert their claims, it may affect a firm’s outlook, competitive position, its riskpremium, and hence discounted value.

In a third post on July 1, 2022 , I pointed to inflation as a key culprit in the retreat of risk capital, i.e., capital invested in the riskiest segments of every market, and presented evidence of the impact on riskpremiums (bond default spreads and equity riskpremiums) in markets.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Equity RiskPremium Path : The equity riskpremium of 5.24%, estimated at the start of May 2022, is at the high end of historical equity riskpremiums , but we have seen higher premiums, either in crises (end of 2008, first quarter of 2020) or when inflation has been high (the late 1970s).

Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums. It is true that economists have researched risk aversion for centuries and concluded that investors are collectively risk averse, and that the level of risk aversion varies across age groups, income levels and time.

To capture the market's mood, I back out the expected return (and equity riskpremium) that investors are pricing in, through an implied equity riskpremium: Put simply, the expected return is an internal rate of return derived from the pricing of stocks, and the expected cash flows from holding them, and is akin to a yield to maturity on bonds.

And Consequences If you are wondering why you should care about risk capital's ebbs and flows, it is because you will feel its effects in almost everything you do in investing and business. That pullback has had its consequences, with equity riskpremiums rising around the world.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes.

Price of Risk The drop in stock and bond prices in the third quarter of 2023 can partly be attributed to rising interest rates, but how much of that drop is due to the price of risk changing? below the index value of 4288, confirming my base case conclusion.

For example, in business valuation, the multiples and riskpremiums relied upon under the market and income approaches may vary considerably depending on the specific company and industry involved.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equity riskpremiums , I described the equity riskpremium as the additional return you would demand, over and above the risk free rate.

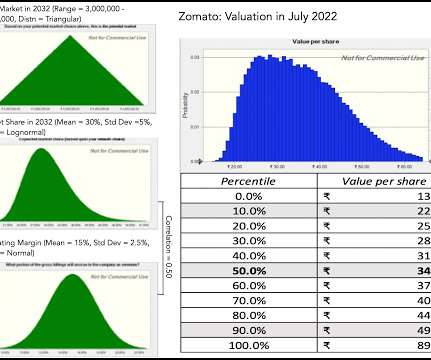

The effects of inflation show up first as higher risk free rates , across currencies, and next in higher riskpremiums, with both equity riskpremiums and default spreads rising. As a company with the bulk of its business in India, Zomato again is more exposed to these developments. 2% from my IPO valuation.

(authored by RSM US LLP) For the first time in years, the riskpremium has been positive, which is an important signal that interest rates are indeed returning to normal. The post The great rate reset: The end of easy money, rising yields and the onset of a new era first appeared on LaPorte.

Capital Asset Pricing Model (CAPM): According to CAPM, the expected return on a stock has two main components: the risk-free rate and a riskpremium. The risk-free rate represents the return an investor can get without taking on any risk, typically derived from government bonds.

If an investor moves money from the risk-free asset into the stock market, they should expect to earn a return in excess of the risk-free rate, what is called an equity riskpremium. These risks can be reduced through the diversification of a portfolio. How Do You Calculate the Capital Asset Pricing Model?

The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.” The riskpremium reflects that market participants require compensation for taking on uncertainty. The riskpremium may incorporate factors such as credit risk or market illiquidity.

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equity riskpremium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. Investors construct portfolios with unsystematic risks, which are well-diversified to reduce total portfolio risk. In theory, arbitrage provides investors with a high chance of success. 1 + RP1 + ??2+

Beta & Risk 1. Equity RiskPremiums 2. I also have implied equity riskpremiums (forward-looking and dynamic estimate of what investors are pricing stocks to earn in the future) for the S&P 500 going back annually to 1960 and monthly to 2008, and equity riskpremiums for countries. Buybacks 2.

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment.

A high M-Score could indicate higher risk, warranting a higher discount rate and thus a lower valuation. Using our sliding scale, we might apply a 10% discount to the valuation:$100 million - (10% $100 million) = $90 millionThis adjusted valuation reflects the increased risk associated with potential earnings manipulation.

And the factor loading for country risk might be 0.1, meaning that 10% of the stock's risk is specific to the country in which the company is based. Next, we need to estimate the risk-free rate and the riskpremium for each risk factor. x 5%) + (0.2 x 4%) + (0.1 x 5%) + (0.2 x 4%) + (0.1

The answer, to me, seems to be obviously yes, though there are still some who argue otherwise, usually with the argument that country risk can be diversified away. In that post, I computed the equity riskpremium for the S&P 500 at the start of 2021 to be 4.72%, using a forward-looking, dynamic measure. as mature markets.

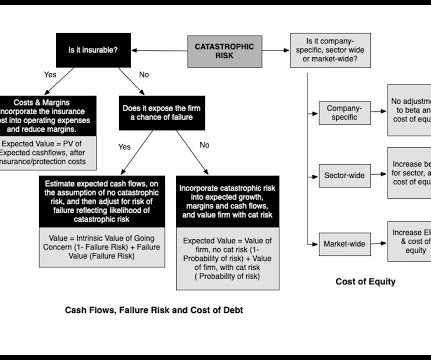

At Peak , these factors help us determine the company-specific riskpremium. Customer Concentration: Having customers who make up a large part of revenue risks the company losing a large part of its revenue. Understanding these for an HVAC litigation valuation is paramount.

In my last data update, I measured the price of risk in the equity market in the form on an implied equity riskpremium, and chronicled how it rose sharply in 2022 and dropped in 2023, paralleling the movements in default spreads.

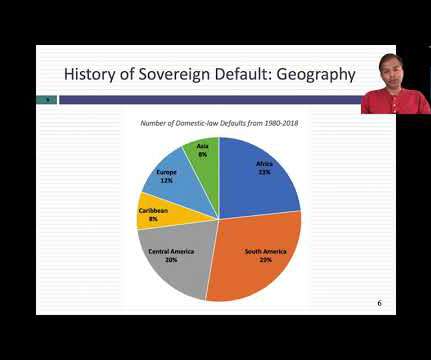

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Debt breakdown 2.

Our study also indicates that market awareness of these issues is growing, as seen in the higher riskpremiums demanded by loan investors when these relationships are perceived to compromise the integrity of loan agreements. This lack of demand often forces lead banks to offer loans at higher interest rates or with greater discounts.

The macro variables that I track on my site relate to the price of risk, a key input into valuation, in both equity and debt markets: US Equity RiskPremiums : The equity riskpremium is the price of risk in equity markets.

Investors will either see more relative risk (or beta) in these companies, if the risks affect an entire sector, or in equity riskpremiums, if they are market-wide. Applications : My argument for using implied equity riskpremiums is that they are dynamic and forward-looking.

When submitting financials as part of your loan package, consider accompanying them with voluntary disclosures similar to the ones that public companies provide about non-GAAP financial measures, and in the MD&A and risk factor sections of their SEC filings.

With limited features and formulas, it can be difficult to account for all the necessary parameters in a valuation, such as interest rates, equity riskpremiums, and beta. It lacks interest rates, equity riskpremiums, beta, and other important data.

Corporate Bonds: No Shortage of Risk Capital In my last post, I chronicled the movement in the equity riskpremium, i.e. the price of risk in the equity market, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

We’ve added a ‘date picker’ across key resources sections, allowing you to examine risk-free rates, corporate tax rates, market riskpremium, and country ratings across any historic date you select. Resources Section Date Improvement: What? Explore this feature in the Resources section. Why Important?

The definition of "net equity" is as follows: equity of the company = sum of subscribed capital, share premiums, revaluation reserves, reserves and retained earnings, minus the tax value of the company's holdings in associated companies and the tax value of its own shares. riskpremium if the company is an SME as defined by European law).

As I noted in my last post , rising risk free rates and equity riskpremiums have pushed up the costs of equity for all companies, and Tesla is not only no exception but is perhaps even more exposed as an above-average risk company.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content