This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on market capitalization and price to book ratios.

Searching for stocks with low price-to-book ratios was a good indication of a potential bargain. However, book values are no longer so informative as lots of intangibles are missing from the balance sheet, and some intangibles that are on the balance sheet, including many acquired intangibles and goodwill, are very hard to interpret.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. trillion in the first six months of 2023, 97.2%

Special considerations for valuing M&A deals include synergies, regulatory issues, economic conditions, tax implications, technology/IP valuation, financing structure, buyer type, and purchase price allocation. Other techniques like Leveraged Buyout (LBO) and Real Options Valuation offer unique perspectives on valuation.

That may explain why Berkshire's stock price was unaffected by Munger's passing. Are markets building in the recognition that Berkshire Hathaway's future will be in the hands of someone other than the two legendary leaders?

For much of the last year, I tracked the S&P 500 and the NASDAQ, the first standing in for large cap stocks and the broader market, and the latter proxying for technology and growth stocks, with some very large market companies included in the mix.

Book value is the value attributable to shareholders in case the company sells all its assets and repays its liabilities (also called liquidation value). A price-to-book ratio of less than 1x indicates that the market values the net assets less than the balance sheet suggests. What does a PB-ratio of less than 1x indicate?

Candidates should highlight their commitment to staying updated on industry trends, regulations, and emerging technologies. One key emphasis is on the Price to Book Value multiple. The Price to Book Value multiple, which compares a bank's market value to its book value, becomes crucial.

MVA can be understood as the Price-to-Book ratio; however, the book value has been refined to account for economic adjustments. Intriguingly, three out of the 11 sectors exhibit a negative percentage (Materials, Information Technology, and Real Estate). and 11.2%, respectively.

Key Financial Ratios: Ratios such as Price-Earnings Ratio (P/E), Price-to-Book Ratio (P/B), and Debt-to-Equity Ratio provide valuable insights into the company's performance and market position. Understanding the company's financial health is fundamental to valuation.

There are a few arguing that the shift to a technology-based economy has removed inflationary pressures permanently, pointing to the last decade where inflation fears never came to fruition. Conversely, the decades where value underperformed growth were 1990-99 and 2010-19, when inflation was much lower than expected.

Using S&P's sector classification, I take a look at how each one did in 2022, looking at the percent changes in market capitalization: In contrast to 2020, when technology and consumer discretionary firms ran well ahead of the pack, the best performing sectors in 2021 were energy and real estate, two of the biggest laggards in 2020.

Slicing the data based on sector yields the following: Against, there are no surprises, with energy being the only sector to post positive returns and with consumer discretionary and technology generating the most negative returns.

I also report on pricing statistics, again broken down by industry grouping, with equity (PE, Price to Book, Price to Sales) and enterprise value (EV/EBIT, EV/EBITDA, EV/Sales, EV/Invested Capital) multiples. Standard deviation in stock price 2. Price to Book 3. High-Low Price Risk Measure 5.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. By focusing so much attention on a small subset of companies, you risk developing tunnel vision, especially when doing peer group comparisons.

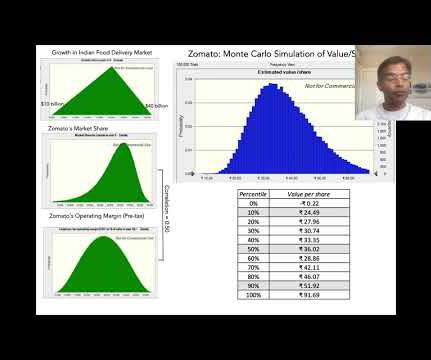

It would be churlish on my part to take issue with the bloat and selective disclosure in Zomato's prospectus, since they are following the script that other technology companies around the world have written for going public, but it is frustrating to read through 420 pages, and still be left in the dark on key numbers.

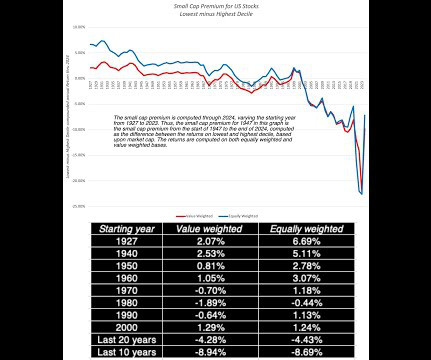

In the next section, I look at stock returns for companies in different price to book deciles, in a simplistic assessment of the value premium. As with the size premium, low price to book (value) stocks have struggled to deliver in the twenty first century, and as with the small size premium, investors have waited for it to return.

You see similar movements in the price to book, where the stock has gone from trading under book value to 6.7 times book value, and the enterprise value, which was less than revenue in 2016-21 to 2.71 times revenues in the most recent two years.

The first is that if markets are efficient, the price to book ratios will reflect the quality of these companies. In this example, for instance, business A, with a market value of equity of $150 million and a book value of equity of $60 million, will trade at 2.50

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content