This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Using S&P's sector classification, I take a look at how each one did in 2022, looking at the percent changes in market capitalization: In contrast to 2020, when technology and consumer discretionary firms ran well ahead of the pack, the best performing sectors in 2021 were energy and real estate, two of the biggest laggards in 2020.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

These assertions may very well be true, but cheap and expensive, at least in pricing terms, is relative, and looking at the data can help you detect rules of thumb that work from those that do not. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Price to Book 3.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. By focusing so much attention on a small subset of companies, you risk developing tunnel vision, especially when doing peer group comparisons.

There are a few arguing that the shift to a technology-based economy has removed inflationary pressures permanently, pointing to the last decade where inflation fears never came to fruition. Consequently, as inflation increases, equity riskpremiums will tend to increase.

For much of the last year, I tracked the S&P 500 and the NASDAQ, the first standing in for large cap stocks and the broader market, and the latter proxying for technology and growth stocks, with some very large market companies included in the mix. Riskpremiums No effect or even a decrease. Riskfree rate will rise.

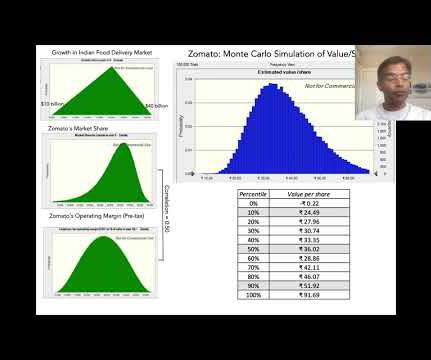

It would be churlish on my part to take issue with the bloat and selective disclosure in Zomato's prospectus, since they are following the script that other technology companies around the world have written for going public, but it is frustrating to read through 420 pages, and still be left in the dark on key numbers.

The first is that if markets are efficient, the price to book ratios will reflect the quality of these companies. In this example, for instance, business A, with a market value of equity of $150 million and a book value of equity of $60 million, will trade at 2.50

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content