This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s used in financial modeling and valuation to estimate the company’s long-term value. In particular, the Terminal Growth Rate is used in a DCF analysis to help calculate the TerminalValue. Different industries have varying Terminal Growth Rates based on growth potential and market maturity.

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the presentvalue of its dividends and that potential future value (either the stock price or the Equity Value via the TerminalValue calculation).

The value of a business is defined by its expected cash flows and their growth, forecasted into perpetuity, and discounted to the present at a discount rate reflective of the risks associated with achieving those cash flows. These cash flows are discounted to the present at an appropriate discount rate and equity value is determined.

It’s also used for calculating a company’s share price, the value of investments, projects, and for budgeting. The DCF method takes the value of the company to be equal to all future cash flows of that business, discounted to a presentvalue by using an appropriate discount rate. Explaining The TerminalValue.

Quoted from Wall Street Oasis.com, it describes discounted cash flow (DCF) process by estimating the total value of all future cash flows (both inflow and outflow), and then discounting them (usually using Weighted Average Cost of Capital – WACC ) to find a presentvalue of the cash flow.

Use DCF analysis to estimate the presentvalue of future cash flows, considering growth rates, discount rates, and terminalvalues. Comprehensive Valuation Process for AI Startups: Start with a financial statement analysis covering the last three years.

Four Mercer Capitalists are here in person, and three of us are presenting. Karolina Calhoun presented yesterday in two sessions on personal goodwill and on a litigation-oriented panel. Atticus Frank will present tomorrow and talk about why market multiples differ between and among industries. million is about $29.0 million.

Debt Usage and TerminalValue In a standard leveraged buyout model , the Debt funding is usually based on a multiple of EBITDA or a percentage of the Purchase Enterprise Value (i.e., the value of the target company’s core business operations in the deal).

Basic Valuation Review The Value of a Business The value of a business is the presentvalue of all expected cash flows from the business (into perpetuity) discounted to the present at a discount rate reflective of the risks associated with achieving those cash flows. 1 – $925,055/$1,000,000).

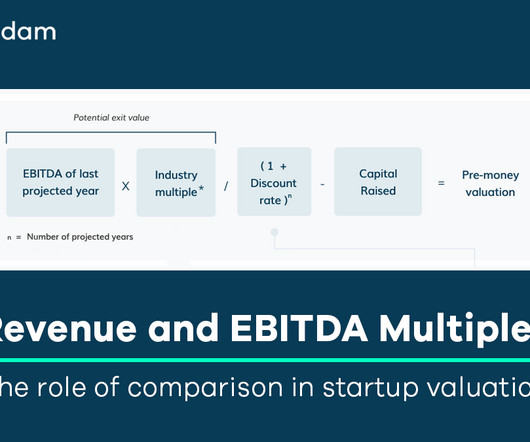

Specifically, in understanding the exit potential of a company, by applying a multiple to the terminalvalue (the last year’s projected EBITDA or revenue). In other words, the ends (like the possible exit values) can justify the means (a seemingly higher present-day valuation).”

For a good example, check out the presentation for Chevron’s acquisition of Noble Energy : “BOE” is “Barrel of Oil Equivalent,” a metric used to convert the energy produced by natural gas into the energy produced by oil to make a proper comparison. Essentially, the NAV Model is a super-long-term DCF without a TerminalValue.

Under a “Capitalization of Earnings” approach, the appraiser will consider both historic and future income probability, based on a steady stream of revenue, and discount these streams to realize a net presentvalue, while using appropriate rates of capitalization. Market Approach. >The

It estimates a company’s intrinsic value based on future cash flows, discounted back to their presentvalue. Calculating terminalvalue. DCF assumes that the value of a business is inherently tied to its ability to generate cash in the future. Selecting an appropriate discount rate.

The ability to communicate complex financial concepts, collaborate with team members, and present findings convincingly is highly valued in valuation roles. Definition: The Dividend Discount Model (DDM) is a valuation approach that establishes the fair value of a stock based on the presentvalue of its anticipated future dividends.

SMEs can present challenges with DCF due to limited historical financial data, unreliable information, inadequate financial forecasts, and difficulty in determining terminalvalue. SMEs, with their unique structures, present specific challenges that can significantly influence their value.

The second section is called “General Principles,” where readers find a discussion of the concept of partial ownership interests, the wide range of possibilities that are raised when such interests, and guidance regarding the differences between valuing businesses versus interests in them.

Discounted Cash Flow (DCF) Method: DCF, a method that calculates the presentvalue of future cash flows, can be challenging to apply to SMEs due to data reliability and future projection issues. SMEs, with their unique structures, present specific challenges that can significantly influence their value.

Cash Flow Discounting: To determine the presentvalue of future cash flows, discounted cash flow (DCF) analysis is employed, taking into account the time value of money.

These methods, such as the Discounted Cash Flow (DCF) analysis, estimate the presentvalue of expected future cash flows generated by the business and directly link valuation to the underlying financial performance of the enterprise. The future cash flows are then discounted back to their presentvalue using a discount rate.

By discounting expected future cash flows to presentvalue, the DCF method enables investors, analysts, and companies to make informed decisions about buying or selling assets. This intrinsic value is the foundation upon which smart investment choices are made. How does the DCF method account for the time value of money?

Fair Market Value Defined Fair market value occurs at the intersection of hypothetical negotiations between hypothetical willing, knowledgeable and able buyers and sellers. Therefore, in every fair market value determination prepared by business appraisers, it is critical that both buyers and sellers are present for the negotiation.

It is the expectation of future returns that give presentvalue to investments. There is no information in any restricted stock study to help business appraisers estimate the value of expected future dividends. And what about the terminalvalue that gives rise to capital appreciation? Refer to the initial figure.

For VC, your strengths should include points like “communication/presentation skills,” “networking ability,” and “being able to update your views quickly” (i.e., So, you could mention a related job, such as strategy, finance, or business development at a portfolio company, and say that you want to return to VC at a higher level eventually.

The value of an interest in a business is a function of the expected cash flows to the interest (which are derivative of the expected cash flows of the business itself, the growth of those cash flows, including a terminalvalue at the end of an expected holding period, and the risks associated with achieving those cash flows.

Here’s an example from the Capstone / Mantos Copper presentation below: Companies often go into detail on individual mines , with estimates for their useful lives, annual production, and “all-in sustaining costs,” or AISC. Again, there is no TerminalValue since you forecast production until the mines stop producing at viable levels.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content