This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

The premium that investors demand over and above the risk free rate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

In computing this implied equity riskpremium for the S&P 500, I start with the dividends and buybacks on the stocks in the index in the most recent year (which is known) and assume that they grow at the rate that analysts who follow the index are projecting for the next five years.

In a third post on July 1, 2022 , I pointed to inflation as a key culprit in the retreat of risk capital, i.e., capital invested in the riskiest segments of every market, and presented evidence of the impact on riskpremiums (bond default spreads and equity riskpremiums) in markets.

Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums. It is true that economists have researched risk aversion for centuries and concluded that investors are collectively risk averse, and that the level of risk aversion varies across age groups, income levels and time.

Key takeaways: The discount rate is primarily used by central banks to manage the economy and investors to calculate the present value of future cash flows from an investment. Investment Discount Rate: In investment analysis, the discount rate is employed to calculate the present value of future cash flows.

By the same token, an investment that delivers a guaranteed return over ten years will not be risk free to an investor with a six month time horizon. Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments.

For example, the market technique compares the company to similar enterprises that have previously been sold, whereas the income approach may involve determining the present value of future cash flows. An Overview of Beneish M-Score Presenting the financial analysis super hero, the Beneish M-Score! Do you recall the dot-com bubble?

A discounted cash flow approach is a type of “income approach” or “present value technique,” two terms used frequently in the FASB Accounting Standards Codification®. The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.”

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equity riskpremium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

Once we estimate the company’s future cash flows, we use a discount rate to find its present value. The discount rate reflects a business’s risks. At Peak , these factors help us determine the company-specific riskpremium. Understanding these for an HVAC litigation valuation is paramount.

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment. in 2022, higher than the 1- 1.5%

Financial statement presentation. As you prepare your financial projections ahead of submitting your loan application package or investor presentation, you want to avoid gaps that require explanation, as they tend to suggest weaknesses in your business. Financial statements are the next step in trying to put a number on your worth.

The logical structure and cleaner aesthetic enhance the presentation of results, all while preserving the customization features that provide the ability to white label your reports. The customization options ensure that your unique insights can be presented in a format that aligns with your preferences and brand identity.

And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the Terminal Value calculation). The DDM is more grounded because it’s based on the company’s actual distributions and potential future value.

Investors will either see more relative risk (or beta) in these companies, if the risks affect an entire sector, or in equity riskpremiums, if they are market-wide. Applications : My argument for using implied equity riskpremiums is that they are dynamic and forward-looking.

The Data As more data has become publicly available, and access to the data becomes easier, the challenge that we face in investing and valuation is that we often have too much data, and information overload is a clear and present danger.

Discounted Cash Flow (DCF) Method: DCF, a method that calculates the present value of future cash flows, can be challenging to apply to SMEs due to data reliability and future projection issues. SMEs, with their unique structures, present specific challenges that can significantly influence their value.

SMEs can present challenges with DCF due to limited historical financial data, unreliable information, inadequate financial forecasts, and difficulty in determining terminal value. Approximations, negotiations, and considering illiquidity premiums help mitigate these challenges. Why Are SME Valuations So Unique and Challenging?

Methods of business valuation by their profitability are presented below. Presentation of the profitability method to evaluate a company Attractions and limits of the method of multiples to value a company How to conduct a company valuation based on profitability? 11% per year. 10% per year.

The definition of "net equity" is as follows: equity of the company = sum of subscribed capital, share premiums, revaluation reserves, reserves and retained earnings, minus the tax value of the company's holdings in associated companies and the tax value of its own shares. riskpremium if the company is an SME as defined by European law).

In this section, I will begin by looking at the evolution of my Tesla value from 2013 to 2021, and then present my updated valuation of the company. My Tesla History I have valued Tesla multiple times over the last decade, and while I have been wrong at each turn, I have tried to learn from my mistakes.

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-free rate. Lower WACC can increase the present value of a firm.

Insurance industry terminology such as risk, premium, loss, deductibles, coverage limits, and perils are some of the fundamental concepts appraisers must grasp. Register for ASA’s PP163 Property Insurance Fundamentals: What Appraisers Need to Know webinar on June 6, 2024 from 2:00-3:00 PM EDT, presented by Thomas Dawson, ASA.

The DCF method takes the value of the company to be equal to all future cash flows of that business, discounted to a present value by using an appropriate discount rate. A discount rate, or discount ‘factor’, is calculated and applied to each year’s cash flow, in order to arrive at the present value. . Does this make sense?

” The hypothetical valuation presented in Mercer’s Musings #2 and “solved” in Mercer’s Musings #3 considered a significant number of factors in developing marketability discounts for two dissimilar, 10% interests in two identical companies. We do so in the context of alternative returns for similar investments.

The income approach focuses on estimating the present value of expected future cash flows. Market volatility, regulatory changes, interest rate fluctuations, tenant turnover, and project-specific risks are examples of factors that can impact a company's value. The asset-based approach assesses the company's net asset value.

The income approach focuses on estimating the present value of expected future cash flows. These factors include market volatility, interest rate fluctuations, regulatory changes, tenant turnover, and property management risks. Common approaches include the income approach, market approach, and asset-based approach.

Market volatility, regulatory changes, interest rate fluctuations, environmental concerns, and construction risks are some examples of factors that can impact a business's value. Assessing and quantifying these risks helps determine an appropriate discount rate or riskpremium when calculating the business's present value.

Don’t miss these industry experts presenting our Business Valuation sessions*: Vanessa Brown Claiborne | ASA, CPA/ABV, AEP | Chief Executive Officer & President, Shareholder | Chaffe and Associates Ms. She has authored articles and presented on valuation topics for numerous organizations.

This method considers the projected cash flows generated by the tax preparation business and applies an appropriate capitalization or discount rate to determine the present value. Factors such as multiples, beta, and equity riskpremium are required for accurate calculations.

Methods such as discounted cash flow (DCF) analysis and capitalization of earnings are commonly used to determine the present value of expected future cash flows. Factors such as multiples, beta, and equity riskpremium are required for accurate calculations.

I also offer online classes in basic finance (present value, risk models and measures) and accounting (or at least my version of it) as background to my main classes. By the end of the class, my objective is not to sell you on the best philosophy but to provide you with a framework where you can find the philosophy that best fits you.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. In computing the latter, I used the current debt ratios for firms, but made no attempt to evaluate whether these mixes were "right" or not.

Risk Surge and Economic Viability : In my last post, I noted the surge in Russia's default spread and country riskpremium, making it one of the riskiest parts of the world to operate in, for any business.

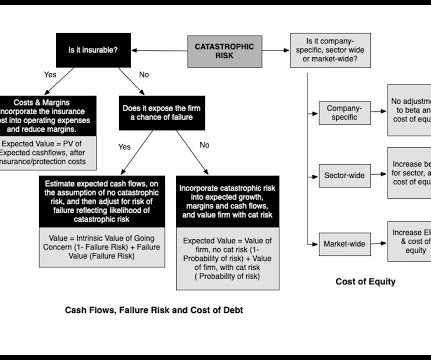

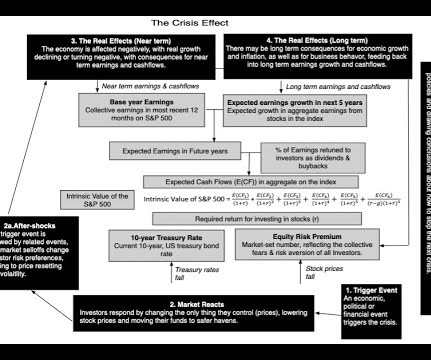

In this section, I will present a crisis cycle, which almost every crisis works its way through, with big differences in how quickly, and with how much damage. In the language of risk, they are demanding higher prices for risk, translating into higher riskpremiums.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

Regulatory changes introduce uncertainty, and their effects are further confounded by the ever-present unpredictability of markets even known variations, whether from unpredictability in inflation and interest rates driven by the Fed, or the basic requirements for capital-raising and deployment set by the SEC equate to risk.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content