This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on market capitalization and price to book ratios.

Zacks Rank & Price Performance MetLife carries a Zacks Rank #2 (Buy) at present. Valuation Price-to-book (P/B) is one of the multiples used for valuing insurance stocks. The stock has gained 10% in the past three months compared with the industry's growth of 5.3%. and 2.4%, respectively, in the said time frame.

By comparing key financial metrics such as price-to-earnings (P/E) ratios, price-to-sales (P/S) ratios, and price-to-book (P/B) ratios, analysts can estimate the target company’s value. DCF involves estimating future cash flows and applying a discount rate to bring those future cash flows to their present value.

Here are some of the most common approaches: Discounted Cash Flow (DCF) Analysis : This method calculates a security’s present value based on its expected future cash flows. The cash flows are discounted back to their present value using a discount rate, reflecting the investment’s risk.

This approach involves forecasting a company’s future cash flows and discounting them back to their present value using an appropriate discount rate. This model estimates the present value of future dividends an investor expects to receive from owning the stock.

Here are some of the most common approaches: Discounted Cash Flow (DCF) Analysis : This method calculates a security’s present value based on its expected future cash flows. The cash flows are discounted back to their present value using a discount rate, reflecting the investments risk.

Here are some of the most common approaches: Discounted Cash Flow (DCF) Analysis : This method calculates a security’s present value based on its expected future cash flows. The cash flows are discounted back to their present value using a discount rate, reflecting the investments risk.

It predicts a company’s future cash flows and adjusts them to their present value using an appropriate discount rate. Dividend Discount Model DDM estimates the present value of expected future dividends from owning a stock. This model evaluates the stock’s fair price based on its dividend yield and expected growth rate.

A DCF analysis considers the projected future cash flows of the business and discounts them back to their present value, taking into account factors such as risk and the time value of money. This method relies on finding appropriate comparables.

The valuation is based on key financial metrics such as Price-to-Earnings (P/E) ratios, Price-to-Sales (P/S) ratios, or Price-to-Book (P/B) ratios. Discounted Cash Flow (DCF): DCF is a fundamental valuation method that estimates the present value of a company’s future cash flows.

Analysts use financial metrics and multiples such as Price to Earnings (P/E), Price to Book (P/B), Enterprise Value to Sales (EV/Sales), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios derived from trading data of similar public companies or deal pricing data of similar M&A transactions.

The ability to communicate complex financial concepts, collaborate with team members, and present findings convincingly is highly valued in valuation roles. Definition: The Dividend Discount Model (DDM) is a valuation approach that establishes the fair value of a stock based on the present value of its anticipated future dividends.

Relative Distribution of ESG Performance and MVA Spread across the Five Regions The box plot presented below depicts the distribution of ESG scores across five regions (Figure 1). MVA can be understood as the Price-to-Book ratio; however, the book value has been refined to account for economic adjustments.

Key Financial Ratios: Ratios such as Price-Earnings Ratio (P/E), Price-to-Book Ratio (P/B), and Debt-to-Equity Ratio provide valuable insights into the company's performance and market position. Understanding the company's financial health is fundamental to valuation.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. In this section, I will list the data that I estimate and report, as well as explain how I consolidate company-level data into more usable group statistics.

The results are similar if you break stocks down based upon price to book ratios or revenue growth rates. This approach is built on the proposition that the intrinsic value of stocks is the present value of the expected cash flows that you generate in perpetuity, from holding these stocks, but it is model agnostic.

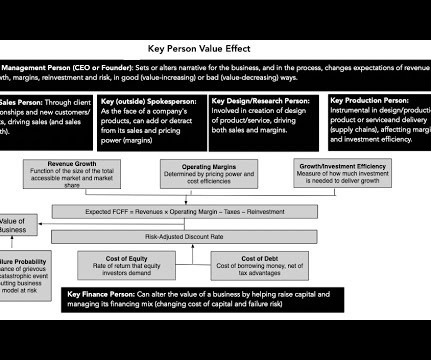

For companies that buy insurance, the key person value then become monetized as a cost, reducing the value of these companies when the key person is present, while increasing its value, when it loses that person.

Using the statement of cashflows from Adani Enterprises, I present a picture of how the company funded its investments: Download data As you can see from the percentages of financing that Adani Enterprises raised from debt and equity, it is incontestable that the company funded almost all of its growth with debt through this period.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content