This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Posted by Mary Ann Deignan, Rich Thomas, and Kathryn Night, Lazard, on Tuesday, August 1, 2023 Editor's Note: Mary Ann Deignan is Head of Capital Markets Advisory, and Rich Thomas and Kathryn Night are Managing Directors in the Capital Markets Advisory group at Lazard. This post is based on a Lazard memorandum by Ms.

Bebchuk and Roberto Tallarita (discussed on the Forum here ); Companies Should Maximize Shareholder Welfare Not Market Value by Oliver Hart and Luigi Zingales (discussed on the Forum here ); Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Max M. Schanzenbach and Robert H.

The 2023 Say on Pay (SOP) season has a unique hallmark unlike previous SOP years: most companies within the S&P 500 have experienced significant decreases in totalshareholderreturn (TSR) in the most recent performance year (2022) for the first time since SOP was mandated in 2011.

The early filers have median revenue of approximately $15B and median market cap of approximately $29B. We focused our analysis on aspects of the disclosure where companies had choices (i.e., comparator groups, company-selected measure, location of disclosure in the proxy, etc.) and also made observations on unique findings.

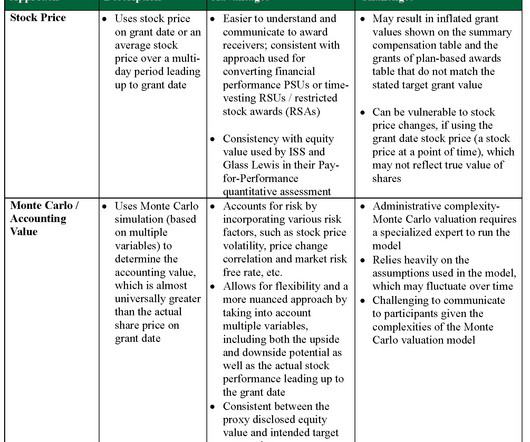

Introduction Thousands of companies, including more than 70% of the S&P 500 companies, grant performance stock units (PSUs) with relative totalshareholderreturn (TSR) or stock price performance-vesting conditions. This post is based on their Pay Governance memorandum.

in 2021, and very few companies reported negative ratios following two strong years of stock market performance 43% of CAP:SCT ratios are greater than 1.0X Vanbastelaer, Kyle McCarthy, Nathan Grantz, and Anish Tamhaney. in 2022, and the greatest clustering of ratios is between 0.0X 75% of CAP:SCT ratios are greater than 1.0X

Daniel Labovitz, the former NYSE head of regulatory policy, is swapping the traditional stock market blues for a greener pasture. As the CEO of the Green Impact Exchange (GIX), he aims to introduce the first US stock market exclusively focused on the $50 trillion-plus global green economy. CEOs and CFOs also like our trading model.

Summary Total vs Actually Paid. Compensation “actually paid” includes certain considerations for changes in pension value, above-market or preferential earnings on non-qualified deferred compensation, and changes in the value of equity awards throughout the year. The average compensation “actually paid” to the non-PEO NEOs.

With respect to a registrant providing initial Pay versus Performance disclosure in its 2023 proxy statement for three years (as permitted by Instruction 1 to Item 402(v) of Regulation S-K), may the registrant present the peer group totalshareholderreturn for each of the three years using the 2022 peer group? Answer: No.

The details for publicly announced programs, include disclosure of announcement dates, dollar amounts approved, expiration dates, if any, programs that expired during the covered period and programs being terminated prior to expiration or under which the company does not intend to make further purchases.

How do you justify making substantial investments and fundamental changes to corporate structures and culture without empirical evidence that it will make a direct impact on shareholder value, totalshareholderreturn, net present value, and individual rates of return? What about stock price?

These key performance metrics include totalshareholderreturn (TSR), peer group TSR, net income, and a measure specific to the company. That serves investors and our markets. Companies will disclose several key performance metrics related to executive compensation.

Large public companies are generally expected to link their CEO pay to totalshareholderreturn over one to three years, whereas a new start-up will tend to focus more on sales growth. Bonus pay may be hard to align following a merger between one firm with huge bonuses and another one with none.

Part of the board’s responsibility is to ensure capital allocation decisions are made with a rationale founded in creating good long-term totalshareholderreturns. The board needs to manage the conflicts between the agents, the principals and indeed between the longer and shorter-term shareholders within the principals.

Josh has been an outstanding leader and partner, growing the business, and successfully bringing the company to the public markets. Goldman Sachs and CDPQ are very pleased with Sterling's performance over the last eight years.

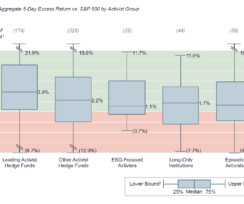

Activist target profile: Top flags for tech and healthcare companies Activists are stock pickers – generally building a position at a target company only if they can drive meaningful risk-adjusted returns. Promoting director share ownership where possible, including through open market director purchases.

The NYSE and Nasdaq adopted listing standards last year to implement the SEC’s clawback rule – these standards became effective on October 2, 2023, and listed companies had until December 1, 2023 to adopt a compliant clawback policy. NOW, THEREFORE, BE IT RESOLVED , that, to the extent required by [Section 303A.14

This suggests that, as we tinker with company goals, we should be careful lest we reduce the substantial benefits already accruing to non-shareholders from the pursuit of shareholderreturn. And the utility function must include criteria to weight tradeoffs between different sets of stakeholders.

On February 22, 2023, the New York Stock Exchange and the Nasdaq Stock Market released their respective versions of a proposed rule that implements the SEC’s clawback rule mandated by Section 954 of the Dodd-Frank Act. Financial reporting measures also include stock price and totalshareholderreturn (TSR).

footnote disclosure to the table for any amounts deducted and added to total compensation of the NEOs to determine the amount of compensation “actually paid” (as described below) and certain related assumptions, as well as the name of each CEO and other NEO included in table for each year and the fiscal year for which they were included.

The transaction is expected to drive attractive totalshareholderreturns, including at least $50 million of synergies, implying expected double-digit Adjusted EPS accretion immediately on a run-rate synergy basis and accelerated earnings growth potential from topline development, synergies, and deleveraging.

As we have previously noted, regardless of industry, size, performance or “newness” to the public markets, no company should consider itself immune from activism. Even companies that are respected industry leaders and have outperformed the market and their peers have been, and are being, attacked.

Moreover, if PVP disclosure was required in a Form 10 (and its accompanying “information statement”), it would not be possible to complete column (f) of the PVP table with respect to the company’s totalshareholderreturn (TSR), since the spin-off company would not have been publicly traded for any of the years covered by the PVP table.

Instead, the Commission is requiring companies to claw back compensation based on stock price and totalshareholderreturn (“TSR”). Chamber of Commerce Center for Capital Markets Competitiveness at 7-8, Sept. Dodd-Frank uses the phrases “based in whole or in part” and “based, in whole or in part” elsewhere. [17]

Although poor economic or stock price performance can increase vulnerability, even companies that are respected industry leaders and have outperformed the market and their peers have been and are being attacked.

Mueller, and Geoffrey Walter, Gibson, Dunn & Crutcher LLP, on Thursday, August 8, 2024 Tags: anti-ESG , ESG , Proxy season , SEC , Shareholder proposals The Credit Markets Go Dark Posted by Jared A.

How do you justify making substantial investments and fundamental changes to corporate structures and culture without empirical evidence that it will make a direct impact on shareholder value, totalshareholderreturn, net present value, and individual rates of return? . Uncertainty in market signals.

In 2024, the rate of CEO turnover following an activist campaign rose to approximately 20% of CEOs of activist targets having left their roles in the past two years (as compared to the 12% market-average CEO turnover for the S&P 500 index). Benchmarking executive compensation relative to peers.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content