This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In particular, the Terminal Growth Rate is used in a DCF analysis to help calculate the TerminalValue. The Terminal Growth Rate and the TerminalValue are important figures in valuations, because they usually represent a significant contributor to the final valuation estimate.

My conclusion is that the various restricted stock studies are inadequate to meet current business valuation standards and that they should not be used as a basis for “guessing” the magnitude of marketability discounts for illiquid interests of closely held businesses.

This post provides a discussion of several implications of the definition of the standard of value known as fair marketvalue. We focus first on the definition of fair marketvalue. We then look at the implications for the so-called “marketability discount for controlling interests.”

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the TerminalValue calculation).

But here, we use what interest we could get from an alternative investment in the market, called the Market Rate. Discount Factor (using Market Rate: r=10%). But first, a quick aside, which you can feel free to skip if you want to jump ahead: Why Do We Use the Market Rate to Calculate the Discount Factor? You get: Year.

So, it turns out that the real application in private markets is enabling investors to quickly justify the pricing they were already aiming for, with some multiple-based voodoo — which recent history tells us can often end in a procyclical tailspin. A shortcut that many investors attempt to use is to apply a multiple.

Introduction and Conclusion My musings on the use of restricted stock discounts to estimate marketability discounts (or DLOMs) have led me to the conclusion: Restricted stock studies/discounts cannot be used to estimate DLOMs in any credible, standards-compliant manner. Three of the first four Mercer’s Musings posts address this issue.

While a growing number of appraisers use a discounted cash flow model to value illiquid minority interests of businesses ( 22% according to a recent Business Valuation Resources Survey ), the majority of appraisers continue to rely on restricted stock studies and pre-IPO studies in their marketability discount determinations.

Research the AI industry and competition to assess the company’s market position. Use DCF analysis to estimate the present value of future cash flows, considering growth rates, discount rates, and terminalvalues. Rapid tech and market changes challenge industry growth and competitive advantage predictions.

The term “Project Finance” at large banks refers to a group that operates like Debt Capital Markets or Leveraged Finance but for infrastructure rather than normal companies. What if market rates for electricity fall? the value of the target company’s core business operations in the deal).

Atticus Frank will present tomorrow and talk about why market multiples differ between and among industries. It is essential to normalize the earnings of operating companies when providing appraisals either at the financial control/marketable minority level or the nonmarketable minority level. These sessions are always lots of fun.

Business owners likely have particular ideas about the value of their company and how best to calculate it, given their experience and knowledge of their financial history, and understanding of the market and industry in which they operate. Market Approach. >The Asset Approach.

It estimates a company’s intrinsic value based on future cash flows, discounted back to their present value. Calculating terminalvalue. DCF assumes that the value of a business is inherently tied to its ability to generate cash in the future. Goodwill : The general reputation of the business in its market.

The second and third musings address the issue of marketability discounts and conclude that it is not possible to comply with any valuation standards, whether USPAP or not, using only averages of restricted stock studies as a basis for “guessing” marketability discounts. The relevant pool of potential buyers, if any.

These examples cover a range of topics, including discounted cash flow (DCF) analysis, comparable company analysis (CCA), and market multiples. Continuous Learning in Valuation Given the dynamic nature of financial markets, continuous learning is essential for professionals in valuation.

Valuing a Small and Medium-sized Enterprise (SME) involves assessing the company’s financial performance, assets, market position, and growth potential. Discounted Cash Flow analysis), Market Approach (e.g. net asset value calculation). The three main methods for SME valuation are the Income Approach (e.g.

Different methods are used, like looking at market prices, predicting future profits, and evaluating assets. Some techniques include comparing companies in the market, estimating future cash flows, and assessing the value of tangible assets. to its marketvalue.

Key Concepts to Know: Before diving into the valuation techniques, it's important to understand concepts like the time value of money, risk and return trade-off, and the significance of growth rates. Various Approaches to Valuation: Valuation can be approached through three main methods - market-based, asset-based, and income-based valuation.

Invested Capital Growth (ICG), as defined by The Economic Times, is “the appreciation in the value of an asset over a period of time.” It is calculated by comparing the current value of a stock, sometimes known as the marketvalue of an asset or investment, to the amount paid when you originally bought it.

As we proceed, we’ll simplify the complex SME valuation process, factoring in unique SME attributes such as inconsistent cash flows, reliance on a restricted client base, and constrained access to capital, which heavily influence their value. How to value an SME? What are the Key Valuation Methods Used for SMEs?

One critical component of the terminalvalue is the perpetual growth rate. the value of all its shares added up). The perpetual growth rate is an assumption of the annual growth rate until the end of time. . inflation). For the UK, for example, the long-term inflation target is 2% whereas for South Africa it is 5%.

The second is that barring the oil companies, whose revenues and margins ebb and flow with oil prices, the only firm on this list that generates double digit margins is Apple, which has been rewarded with the largest market capitalization of any company in the world. It was the reason that I argued at a $1.2

Were also bigger and had higher market capitalizations and better operating performance, on average. Market Pricing and Restricted Stock Discounts. The next figure examines the offer amounts, size of the transactions, and market pricing of the dividend-paying restricted stock issuers. We make observations from the second figure.

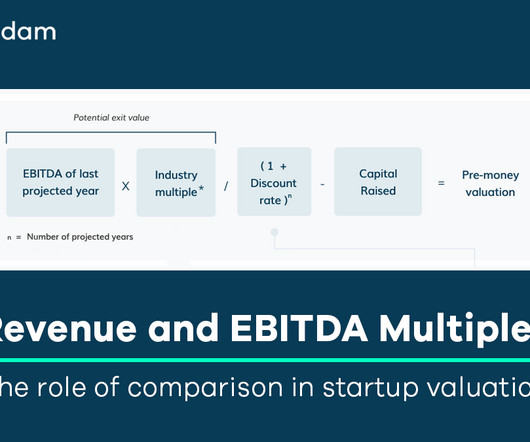

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 21.44 ↑ 2.14% Advertising & Marketing 10.55 34.85 ↑ 178.58% Financial & Commodity Market Operators & Service Providers 153.4 6.38 ↓ -29.42% Food Markets 9.04

No Right or Wrong Answers – Some technical questions have correct answers, but many market and investment ones do not. Market and Investment Questions – Which startup would you invest in? Which market is attractive? Which markets should we avoid? Q: Tell me about the current IPO, M&A, and VC funding markets.

The accuracy of these projections can be influenced by external factors and market conditions, making them inherently uncertain. Any inaccuracies in the inputs, such as revenue forecasts, discount rates, or terminalvalues, can lead to misleading valuations.

On the one hand, the market’s excess liquidity might be a factor. These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. Advertising & Marketing. Financial & Commodity Market Operators & Service. 5%. Food Markets.

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 20.99 ↓ -43% Advertising & Marketing 12.74 12.51 ↓ -32% Financial & Commodity Market Operators & Service † 30.92 ↔ 0% Food Markets 9.05 ↔ 0% Food Markets 9.05

Oil & Gas Investment Banking Definition: In oil & gas investment banking, professionals advise companies that search for, produce, store, transport, refine, and market energy on raising debt and equity and completing mergers and acquisitions. Also, there are few “independent” Downstream companies in major markets like the U.S.,

The sources of growth also matter; emerging markets’ infrastructure spending drove up metal consumption for a long time, but now there’s a rising demand in developed markets due to EVs and renewable energy. As a result, they operate in more of a global market, with fewer regional disparities. and Industrias Peñoles (Mexico).

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 17.71 -18.24% Advertising & Marketing 11.94 12.43 -26.06% Financial & Commodity Market Operators & Service Providers 28.48 13.31 43.27% Food Markets 9.29

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content