This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

That recovery notwithstanding, uncertainties about inflation and the economy remained unresolved, and those uncertainties became part of the market story in the third quarter of 2023. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023.

I am not a market prognosticator for a simple reason. I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis.

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term.

The nature of markets is that they are never quite settled, as investors recalibrate expectations constantly and reset prices. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

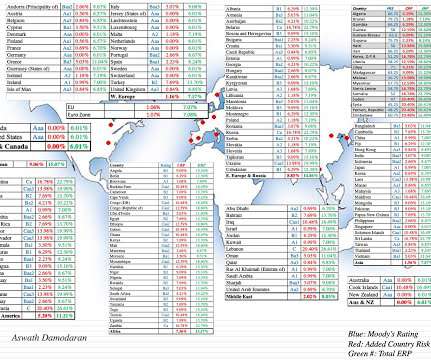

Country Risk: Equity Risk For equity investors, the price of risk is captured by the equity riskpremium, and equity riskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. As a result, treasury bond investors faced one of their worst years in history, losing close to a fifth of their principal, as bonds were repriced.

That positive result notwithstanding, the recovery was uneven, with a big chunk of the increase in market capitalization coming from seven companies (Facebook, Amazon, Apple, Microsoft, Alphabet, NVidia and Tesla) and wide divergences in performance across stocks, in performance. increase in market capitalization.

With this investment, you face price risk , since even though you know what you will receive as a coupon or cash flow in future periods, since the present value of these cash flows, will change as rates change. For an investment to be risk free then, it has to meet two conditions.

By the end of 2021, it was clear that this bout of inflation was not as transient a phenomenon as some had made it out to be, and the big question leading in 2022, for investors and markets, is how inflation will play out during the year, and beyond, and the consequences for stocks, bonds and currencies.

Investors are constantly in search of a single metric that will tell them whether a market is under or over valued, and consequently whether they should buying or selling holdings in that market. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums.

As we start 2024, the interest rate prognosticators who misread the bond markets so badly in 2023 are back to making their 2024 forecasts, and they show no evidence of having learned any lessons from the last year. The Fed Effect: Where's the beef?

Discounted cash flow approaches are also utilized within other functions of an organization, such as treasury, budgeting, financial planning and analysis, and tax planning. An entity may draw from its own experience as well as that of its peers, industry, geography, market, or other pertinent source.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. All of these measures, no matter how carefully designed, give a measure of inflation in the past, and markets are ultimately concerned more with inflation in the future.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms.

The idea is not new to encourage companies to increase their capitalization and reduce their bank debt (partly through more recourse to the capital market - CMU project). The rate would be calculated based on a 10-year "risk-free interest" rate depending on the currency, increased by a 1% riskpremium (1.5%

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasury rates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. against developed market currencies.

But here, we use what interest we could get from an alternative investment in the market, called the Market Rate. Discount Factor (using Market Rate: r=10%). But first, a quick aside, which you can feel free to skip if you want to jump ahead: Why Do We Use the Market Rate to Calculate the Discount Factor? You get: Year.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

As inflation has taken center stage, markets have gone into retreat globally, and across asset classes. In 2022, as bond rates have risen, stock prices have fallen, and crypto has imploded, even true believers are questioning what the bottom for markets might be, and when we will get there.

As the world's attention is focused on the war in the Ukraine, it is the human toll, in death and injury, that should get our immediate attention, and you may find a focus on economics and markets to be callous. The increase in default spreads was not restricted to foreign markets, as fear also pushed up spreads in the corporate bond market.

The other is pragmatic , since it is almost impossible to value a company or business, without a clear sense of how risk exposure varies across the world, since for many companies, either the inputs to or their production processes are in foreign markets or the output is outside domestic markets.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation.

Encourage savings/ capital formation : In an economy, where private capital is behind the bulk of economic investment and growth, governments are dependent up the health of capital markets (stocks and bonds) for continued growth.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

Coming after a few days where the market seemed to have found its bearings (at least partially), it was clear from the initial reactions across the world that the breadth and the magnitude of the tariffs had caught most by surprise, and that a market markdown was coming.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Equity RiskPremiums 2. Buybacks 2.

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. In this post, I will begin by looking at movements in treasury rates, across maturities, during 2024, and the resultant shifts in yield curves.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

The second was a comment that I made on a LinkedIn post that had built on my implied equity premium approach to the Indian market but had run into a roadblock because of an assumption that, in an efficient market, the return on equity would equate to the cost of equity.

The Indian and Chinese markets cooled off in 2024, posting single digit gains in price appreciation. The Indian and Chinese markets cooled off in 2024, posting single digit gains in price appreciation. I converted all of the market capitalizations into US dollars , just to make them comparable.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. Many of these hiring firms have supply chains that stretch across the world and sell their products and services in foreign markets.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content