This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

That recovery notwithstanding, uncertainties about inflation and the economy remained unresolved, and those uncertainties became part of the market story in the third quarter of 2023. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023. billion.

I am not a market prognosticator for a simple reason. I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis.

That positive result notwithstanding, the recovery was uneven, with a big chunk of the increase in market capitalization coming from seven companies (Facebook, Amazon, Apple, Microsoft, Alphabet, NVidia and Tesla) and wide divergences in performance across stocks, in performance. increase in market capitalization.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

An entity may draw from its own experience as well as that of its peers, industry, geography, market, or other pertinent source. The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.” Understanding the Calculation and the Output.

A wide range of techniques, such as the asset-based strategy, market approach, and income approach, have been employed by analysts. For example, the market technique compares the company to similar enterprises that have previously been sold, whereas the income approach may involve determining the present value of future cash flows.

I have been writing about, and valuing, Tesla for most of its lifetime in public markets, and while it remains a company that draws strong reactions, it is also one that I truly enjoy valuing. Tesla: The Back Story I first valued Tesla in 2013 , as a "luxury automobile company" and I have valued almost every year since.

My last valuation of Tesla was in November 2021, towards its market peak, and given its steep fall from grace, in conjunction with Elon Musk's Twitter experiment, it is time for a revisit.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The Interest Rates Story To me the biggest story of markets in 2021 has been the rise of interest rates, especially at the long end of the maturity spectrum.

It helps owners determine the fair market value of their business, which is essential when considering a sale, merger, or acquisition. Market Conditions and Industry Trends Evaluating the current market conditions and industry trends is critical in assessing the value of a tax preparation business.

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

The various problems facing the company led the court to embrace the respondents’ theory that SWS would continue to face an uphill climb given its relatively small size, which prevented it from scaling its substantial regulatory, technological, and back-office costs. Hilltop’s Influence on the Sale Process Rendered Merger Price Unreliable.

Geographic Location and Market Demand The geographic location of a disaster restoration business plays a significant role in its valuation. The local market dynamics, competition, and potential for future growth are crucial factors to consider when valuing a business. The total value of these assets forms the basis for the valuation.

I take the point of view that uncertainty should not stop you from valuing companies, that your value estimates will have more error in them, but since the market also faces the same uncertainty, your best bargains may be in the midst of uncertainty. That tells me three things.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. against developed market currencies.

Kevin holds an MBA in finance from Georgia State University and a Bachelors in Chemical Engineering from the Georgia Institute of Technology. He is the Director of the Pepperdine Private Capital Markets Project (privatecap.org) and Executive Director for the Pepperdine Most Fundable Companies competition (pepperdine.edu/mfc).

If equity markets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equity markets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

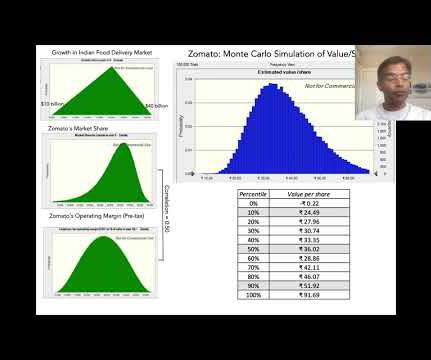

Zomato, an Indian online food-delivery company, was opened up to public market investors on July 14, 2021, and its market debut is being watched for clues by a number of other online ventures in India, waiting in the wings to go public.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms. Are US companies more levered than they were a decade ago?

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. All of these measures, no matter how carefully designed, give a measure of inflation in the past, and markets are ultimately concerned more with inflation in the future.

As the world's attention is focused on the war in the Ukraine, it is the human toll, in death and injury, that should get our immediate attention, and you may find a focus on economics and markets to be callous. The increase in default spreads was not restricted to foreign markets, as fear also pushed up spreads in the corporate bond market.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Note that this framework applies for all businesses, from the smallest, privately owned businesses, where debt takes the form of bank loans and even credit card borrowing and equity is owner savings, the largest publicly traded companies, where debt can be in the form of corporate bonds and equity is shares held by public market investors.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Equity RiskPremiums 2. Buybacks 2.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

For those of you who have been tracking the market, the AI segment in the market has held its own since September, but even before the last weekend, there were signs that investors were sobering up on not only how big the payoff to AI would be, but how long they would have to wait to get there.

The second was a comment that I made on a LinkedIn post that had built on my implied equity premium approach to the Indian market but had run into a roadblock because of an assumption that, in an efficient market, the return on equity would equate to the cost of equity.

Corporate control : There are companies that choose to borrow money, even though debt may not be the right choice for them, because the inside investors in these companies (family groups, founders) do not want to raise fresh equity from the market, concerned that the new shares issued will reduce their power to control the firm.

Thus, my estimates of equity riskpremiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. Many of these hiring firms have supply chains that stretch across the world and sell their products and services in foreign markets.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content