This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

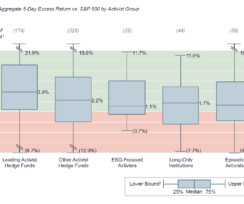

companies with marketcapitalizations greater than $500 million at the time of campaign announcement. We measured totalshareholderreturn (TSR) versus the S&P 500 over one week and one year as proxies for short term and long-term excess return generation.

With respect to a registrant providing initial Pay versus Performance disclosure in its 2023 proxy statement for three years (as permitted by Instruction 1 to Item 402(v) of Regulation S-K), may the registrant present the peer group totalshareholderreturn for each of the three years using the 2022 peer group? Answer: No.

However, in 2023 the market logged a notable uptick in “sell-the-company” and “wind-down-the-company” campaigns at clinical stage companies with marketcapitalizations below cash balances and either very early stage or failed lead programs. Preparing “break the glass” communications plans. Conducting tabletop exercises.

footnote disclosure to the table for any amounts deducted and added to total compensation of the NEOs to determine the amount of compensation “actually paid” (as described below) and certain related assumptions, as well as the name of each CEO and other NEO included in table for each year and the fiscal year for which they were included.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content