This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

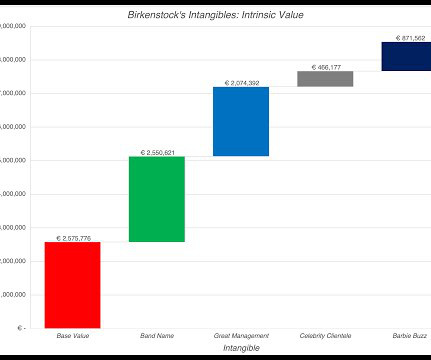

The Value of IntangibleAssets Accounting has historically done a poor job dealing with intangibleassets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

This is accomplished through methods like Comparable Company Analysis, Precedent Transaction Analysis, and MarketCapitalization, which collectively offer insights into the company’s value within the context of the broader market landscape. It represents the total market value of the company’s equity.

This pivotal metric is typically calculated by summing the marketcapitalization and net debt of the organization. Understanding equity value is essential as it provides a clear indication of what shareholders truly own in the business, reflecting the residual claim on assets once all debts and obligations are settled.

Asset Composition : The nature of assets held by the company, including both tangible and intangibleassets, affects valuation. Intellectual property, real estate, and equipment are examples of tangible assets, while patents and trademarks represent intangibleassets.

Two commonly used asset-based approaches are: a) Book Value Method: The book value method calculates a company’s net asset value by subtracting total liabilities from the fair market value of total assets. It indicates how much value the market assigns to each dollar of the company’s revenue.

Two commonly used asset-based approaches are: a) Book Value Method: The book value method calculates a company’s net asset value by subtracting total liabilities from the fair market value of total assets. It indicates how much value the market assigns to each dollar of the company’s revenue.

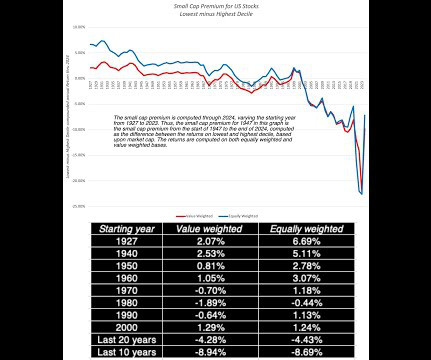

I follow up by looking at companies broken down by marketcapitalization, with an eye on whether the much-vaunted small cap premium has made a comeback. In the process, I also look how much the market owes its winnings to its biggest companies, with the Mag Seven coming under the microscope. Where does that leave us?

Accounting Inconsistencies : I have written about the inconsistency in how accountants calculate capital expenditure at firms with significant investments in intangibleassets and R&D, and that inconsistency can play out in your FCFE computation.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content