This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the TerminalValue calculation).

For public companies, this is made easier by reporting requirements for financial information, as well as the liquid nature of those shares — meaning the current share price is always known. For private companies, it’s a whole different ball game. In reality, this fails on a number of fronts.

Well, the short answer is after that forecast period where we estimate each year’s cash flows then discount them, we add a single number at the end to account for all the theoretical years in the future, called the TerminalValue (TV). Explaining The TerminalValue. How do I calculate the TerminalValue?”

Discount Future Cash Flows – either by using the Mid-Year discount or a simple discount period, it is fairly simple to calculate the present value of future cash flows. This causes difficulties in future performance forecasting since there is limited or no comparable historical information.

The value of all remaining cash flows after the finite forecast period is captured in the terminalvalue, which is, effectively, a capitalization of earnings or cash flows at the end of the forecast period. These cash flows are discounted to the present at an appropriate discount rate and equity value is determined.

Because most of these assets are private , finding substantial information for deal discussions can be very difficult. Debt Usage and TerminalValue In a standard leveraged buyout model , the Debt funding is usually based on a multiple of EBITDA or a percentage of the Purchase Enterprise Value (i.e.,

The expected terminalvalue for the illiquid investment based on the financial control value of $18.0 The present value based on these assumptions is $11.65 The expected terminalvalue based on a $12.0 million value with non-normalized earnings is $19.3 million is about $29.0 million ($29.0

It estimates a company’s intrinsic value based on future cash flows, discounted back to their present value. Calculating terminalvalue. DCF assumes that the value of a business is inherently tied to its ability to generate cash in the future. This precision helps stakeholders make more informed decisions.

Key Takeaways: Valuing Small and Medium-sized Enterprises (SMEs) is crucial for various financial decisions like mergers and acquisitions, investments, and reporting. It determines the economic worth of a company and is essential for informed decision-making.

Access to, availability of, and reliability of information regarding the underlying asset or entity. It is fairly standard to consider the ownership structure and configuration and influence that management might have on the value of illiquid minority interests. An asset example is included the right to partition.

Whether you are an investor, a business owner, or a finance professional, the ability to accurately assess the worth of a company is crucial for making informed decisions. This article aims to provide you with a comprehensive guide on how to value a company, covering different valuation methods, financial analysis, and qualitative factors.

Additionally, a shrewd evaluation of the industry landscape, competition, and potential for expansion helps gauge the growth prospects that contribute to its value. While the DCF method is widely applicable, implementing it to value SMEs often presents some hurdles due to their unique characteristics.

Economic Information in Pre-IPO Discounts? The information we can glean from this definition and example is limited to the following: A transaction occurred at some point prior to an IPO (perhaps three months, six months, nine months, or a year or more) The pre-IPO price was $6.50 per share The price at the subsequent IPO was $13.00

Can TerminalValue be Negative? Navigating Theoretical and Practical Aspects: Theoretical scenarios where terminalvalue might be negative can be explored by considering the perpetuity growth method. LBO, on the other hand, relies heavily on terminalvalue and expected Internal Rate of Return (IRR).

This 2008 version had information on 477 restricted stock transactions, up from 430 transactions in the 2004 version. It is the expectation of future returns that give present value to investments. We have just seen very little information about dividends in the Stout/FMV Restricted Stock Database. Refer to the initial figure.

Uncover the secrets behind making informed investment choices and explore alternative valuation methods to enhance your financial decision-making skills. Introduction In the world of finance, making informed decisions about investments, acquisitions, or assessing the value of a company is crucial.

Valuation is crucial in mergers and acquisitions (M&A) because it informs several key aspects of the transaction. Since cash flow projections cannot be made indefinitely, a terminalvalue is often calculated to account for the value of cash flows extending beyond the forecast period. Petitt and Kenneth R.

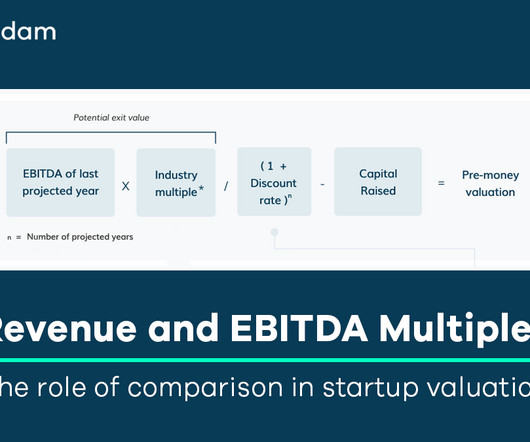

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 13.59 ↑ 20.59% Professional Information Services 18.25 The data is based on the early 2024 estimate, published annually by Prof. Aswath Damodaran of New York University. 6.17 ↓ -43.81% Aluminum 5.3

For example, the definition of fair market value found in Revenue Ruling 59-60 is: 2.2 Court decisions frequently state in addition that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well informed about the property and concerning the market for such property.

A: You would start by reading about the market and its current startups and finding product, team, and financial information. You’ll usually review each startup’s pitch deck or meet with them, and if they’re of interest, you’ll go through additional meetings and request more information before investing (see above).

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 11.27 ↓ 32% Professional Information Services 32.31 The data is based on the early 2023 estimate, published annually by Prof. Aswath Damodaran of New York University. 9.48 ↓ -40% Airlines 24.89

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. Professional Information Services. You can refer to the table below to see how the EBITDA multiples for the industries available on the Equidam platform will change on November 29th, 2021.

Companies tend to present their results in a high-level way, rarely going down to the level of individual mines: So, you tend to create equally high-level forecasts for these firms unless one is a client company sharing much more detailed information with you.

These are applied to compute the Terminalvalue in the DCF method with Multiple and the potential exit value in the VC method. 15.49 9.39% Professional Information Services 11.38 The data is based on our analysis of more than 30,000 public companies as of the 31st of December 2024. 8.81 -29.35% Airlines 8.42

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content