This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term. at the start of that year.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equity riskpremiums , I described the equity riskpremium as the additional return you would demand, over and above the risk free rate.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board. to 25% for the Eurozone.

The adjustment added to the risk-free rate to arrive at the risk-adjusted rate is often referred to as the “riskpremium.” The riskpremium reflects that market participants require compensation for taking on uncertainty. The riskpremium may incorporate factors such as credit risk or market illiquidity.

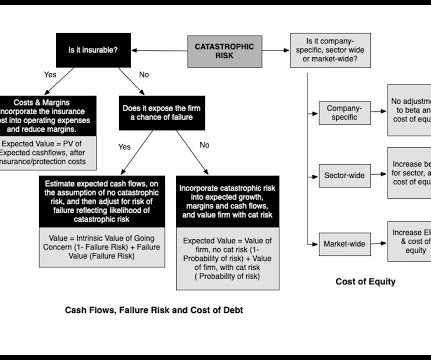

These are three very different stories, but what they share in common is a fear, imminent or expected, of a catastrophic event that may put a company's business at risk. Deconstructing Risk While we may use statistical measures like volatility or correlation to measure risk in practice, risk is not a statistical abstraction.

Just as rising equity riskpremiums push up the cost of equity, rising default spreads push up the cost of debt of companies, with the added complication of higher default risk for those companies that had pushed to the limits of their borrowing capacity in a low interest-rate environment.

When submitting financials as part of your loan package, consider accompanying them with voluntary disclosures similar to the ones that public companies provide about non-GAAP financial measures, and in the MD&A and risk factor sections of their SEC filings.

As I noted in my last post , rising risk free rates and equity riskpremiums have pushed up the costs of equity for all companies, and Tesla is not only no exception but is perhaps even more exposed as an above-average risk company.

Understanding Property Insurance Basics Property insurance serves as a financial safety net for property owners in the event of property damage or total loss. Insurance industry terminology such as risk, premium, loss, deductibles, coverage limits, and perils are some of the fundamental concepts appraisers must grasp.

In the graph below, I look at the 10-year US T.Bond rate and the 10-year TIPs rate on a monthly basis, going back to the start of 2003, when TIPs started trading: The advantage of using interest rates to forecast inflation is that it not only is constantly updated to reflect real world events, but also because there is money riding on these bets.

Therefore, recalculating beta periodically or when significant events occur is advisable for accurate risk assessment. Market Risk-Free Rate: Beta calculations often involve comparing the asset’s returns to a risk-free rate, such as the yield on a government bond with a similar maturity.

We note that the higher the expected rate (in other words, the greater the risk is perceived as necessary, to the point of requiring a substantial "riskpremium"), the lower the multiple that will apply and therefore the lower valuation: we buy cheaper which is less safe. 11% per year. 10% per year. around 1.5%). -

ASA International Conference is the leading event for the global valuation profession. He is a frequent presenter on valuation topics, and is currently a subject matter expert on the Appraisal Foundation’s working group preparing a Valuation Advisory on the Company-Specific RiskPremium.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

It is true that a sovereign CDS spread gives you a more updated measure of default risk, since it is market-set, but as with all market-based measures, it comes with far more volatility and overshooting than a ratings-based spread, and it is available for only a subset of countries.

Risk Surge and Economic Viability : In my last post, I noted the surge in Russia's default spread and country riskpremium, making it one of the riskiest parts of the world to operate in, for any business. On a different note, the events of the recent weeks have also pointed to the elasticity of the ESG concept.

Clearly, this is simplistic, since you can have unusual events during a year that cause inflation in that year to spike. (In In fact, in the graph below, I compare the price of risk in both the equity and bond markets across time: In most years, equity riskpremiums and bond default spreads move in the same direction, as was the case in 2024.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content