This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Research shows that socially responsible activities enhance firmvalue while irresponsible social activities destroy value and that firms with more women directors tend to do better on social and environmental issues.

As a social-policy instrument, forced board-gender balancing is in principle unrelated to firms’ economic performance. Nonetheless, imposing such a policy may have unintended consequences (positive or negative) for firmvalue, which is important for all of a firm’s constituencies – not only shareholders – to understand properly.

"The bankruptcy of banks can have a ripple effect on the value of companies that work with the bank, and it's an aspect of valuation that cannot be ignored." A firm'svalue and the risk of the financial crisis that banks must deal with can have complicated and diverse relationships. Says Tamir Levy, Ph.D.,

By understanding these regulations thoroughly, your firm can foster deeper relationships and move from transactional compliance work to a proactive advisory role. For example, advising a client on how to strategically sell a tokenized asset to minimize taxes could save them thousands, cementing your firmsvalue beyond tax preparation.

Likewise, judges in cases involving corporate governance matters such as anti-takeover devices and fiduciary duties have cited those studies when assessing the consequences of different governance mechanisms for firmvalue. The second is to evaluate what happens to firms’ values after they adopt or remove a governance provision.

Few topics in the corporate and securities law literature are as controversial as securities class actions – that is, actions in which shareholders of public firms seek to collectively obtain compensation for damages resulting from false or misleading statements in corporate disclosures.

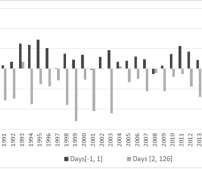

Cleanup Measures Around Turnover Events The figure shows the mean cleanup activity (writeoffs) around the CEO turnover year (t=0). The time window is three years before to three years after the event year [-3;+3]. For each t there are 2428 observations, which is the number of turnover events in our sample. REFERENCES Ali, A.,

There are several ways that firms can support and upskill talent, including sending professionals to seminars and training. data mining and visualization, predictive analytics) ranked high, with 87 percent of firmsvaluing that skill, followed by advanced taxation (e.g., Furthermore, advanced analytics (e.g.,

However, the study found little support for the idea that DEI’s value stems primarily from pleasing other stakeholders. The researchers were careful to rule out alternative explanations for their findings. None of these alternative explanations held up to scrutiny.

As a (predominantly) equity investor, a sponsor will tend to be biased toward postponing events such as a sale of the distressed business or a bankruptcy. Postponing an event that would wipe out the sponsor’s interest becomes paramount, even if the means to do so entail negative expected enterprise value and substantial litigation risk.

The anti-fraud provisions of federal securities laws require plaintiffs to specify in a complaint the misleading statements, which provides attorneys with a strong incentive to comb through defendant firms’ ESG statements to identify material misrepresentations or omissions. Unlike many regulatory or legal events that affect only U.S.

Additional analyses find that the increased association occurred after the adoption of the reforms, and the result is robust to using alternative samples, event windows, and estimation methods. A natural question is whether the post-reform changes in boardroom gender diversity are in line with changes in firm performance.

We also predict that young life-cycle firms are less likely to improve financial reporting as a result of financial regulation because a significant portion of young life-cycle firms’ value stems from intangible assets that are not recorded or disclosed in financial statements under current accounting rules.

Pratt & ASA Educational Foundation Valuing Fraction Interests in Real Estate 2.0 , by Dennis A. Why: ASA Educational Foundation’s annual auction raises funds to give course-taking grants to up-and-coming appraisers which benefits our future membership, supports development of appraisal textbooks, and much more.

Proactive follow-ups and keeping clients informed about case progress show that the firmvalues them. Digital marketing techniques, such as search engine optimization (SEO) and content marketing, help law firms establish a strong online presence. Leveraging AI-powered legal research tools enhances efficiency and accuracy.

One drawback is that conventional models, like the discounted cash flow analysis, might not effectively account for the features of startup firms. Valuing startups demands a strategy due to their high-risk nature and limited historical financial data. It is important to acknowledge that they do have their limitations.

One drawback is that conventional models, like the discounted cash flow analysis, might not effectively account for the features of startup firms. Valuing startups demands a strategy due to their high-risk nature and limited historical financial data. It is important to acknowledge that they do have their limitations.

This is direct evidence that the announcement causes expectations of firmvalue to be biased upward. Returns are adjusted for firm size and book-to-market of equity. Firms seeking strategic alternatives may have confounding characteristics or experience other corporate events that also lead to low future returns.

Whether to make this news public is a key decision since it can have significant consequences that affect investor reactions, the subsequent sale process (should one occur), firm operations, employees, and ultimately firmvalue. In a recent paper , I look for empirical evidence supporting arguments on both sides.

39] ESG ratings are proprietary weighting schemes, often grounded in self-reported company data, published by for-profit firms angling for subscription revenue. In any event, the most recent scholarly research indicates that there may be a performance premium associated with certain ratings schemes. [40] Available at [link].

It takes effect on September 1, 2022, and approximately 20 percent of Russell 3000 issuers will have to apply it at their 2022 annual general meetings in the event of a contested election. The new rule lowers the barriers for nominations from traditional activists as well as from labor and climate activists and employees.

I think that view misses a key difference between default risk and goodness, insofar as default is an observable event and services were able to learn from corporate defaults and fine tune their ratings.

16] See, e.g. , Austin Moss, James Naughton, and Clare Wang, The Effect of ESG Press Releases on Retail Investors , (June 12, 2020), [link] (“Our tests do not detect any retail investor response to ESG press releases, suggesting that these disclosure events do not inform retail trading decisions. Overall we conclude that the average U.S.

How do you justify making substantial investments and fundamental changes to corporate structures and culture without empirical evidence that it will make a direct impact on shareholder value, total shareholder return, net present value, and individual rates of return? . Do ESG programs impact firmvalue? Reputation.

News events provide an ideal setting because they allow us to overcome measurement challenges, such as investors’ frictions in becoming aware of and subsequently understanding companies’ underlying ESG performance. Our approach complements prior research by focusing on how investors transact around nearly all newsworthy ESG-related events.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content