This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s used in financial modeling and valuation to estimate the company’s long-term value. In particular, the Terminal Growth Rate is used in a DCF analysis to help calculate the TerminalValue. Different industries have varying Terminal Growth Rates based on growth potential and market maturity.

The DDM is more grounded because it’s based on the company’s actual distributions and potential future value. And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the EquityValue via the TerminalValue calculation).

Well, the short answer is after that forecast period where we estimate each year’s cash flows then discount them, we add a single number at the end to account for all the theoretical years in the future, called the TerminalValue (TV). Explaining The TerminalValue. How do I calculate the TerminalValue?”

Project Finance Definition: “Project Finance” refers to acquisitions, debt/equity financings, and new developments of capital-intensive infrastructure assets that provide essential utilities and services. However, many people also use the term more broadly to refer to equity, debt, and advisory for infrastructure assets.

Discount Future Cash Flows – either by using the Mid-Year discount or a simple discount period, it is fairly simple to calculate the present value of future cash flows. This action will cause fluctuations in the overall value of equity and debt ratio. These concerns add intricacies to the terminalvalue computation.

The value of all remaining cash flows after the finite forecast period is captured in the terminalvalue, which is, effectively, a capitalization of earnings or cash flows at the end of the forecast period. These cash flows are discounted to the present at an appropriate discount rate and equityvalue is determined.

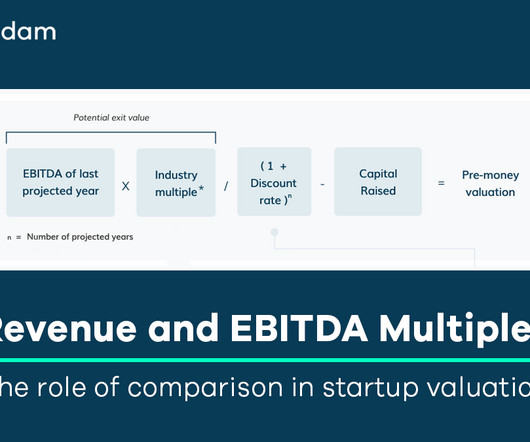

Imagine comparing products in the supermarket, where different box sizes and a range of pricing may make it hard to determine the value; labels that give you the price per kg of product can greatly simplify that process. This is more useful than trying to establish current pricing, as the ultimate outcome always depends on the exit.

Understanding the Concept: In essence, FCFF encapsulates the cash that can be distributed to both debt and equity holders after meeting operational needs and capital expenditures. The resulting value represents the cash available to all contributors of capital—both debt and equity. What is Free Cash Flow to Equity?

To discover how blue sky valuation combined with the Discounted Cash Flow (DCF) method helps assess intangible assets like brand equity, intellectual property, and goodwill. It estimates a company’s intrinsic value based on future cash flows, discounted back to their present value. Calculating terminalvalue.

Analysts use financial metrics and multiples such as Price to Earnings (P/E), Price to Book (P/B), Enterprise Value to Sales (EV/Sales), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios derived from trading data of similar public companies or deal pricing data of similar M&A transactions.

Since, in most valuations, we assume an ongoing business basis where most of the value comes from the terminalvalue, a smooth transition of cashflows from the discrete to the fade, and then to the terminal period is needed. as well as valuing the investment profitability. References.

The emerging attractiveness of the entity for equity offering, sale, merger or acquisition. The determination of the present value of expected future cash flows is inherently a quantitative exercise. The final cash flow for minority interests is the expectation of a terminalvalue at the end of the expected holding period.

Key Financial Ratios: Ratios such as Price-Earnings Ratio (P/E), Price-to-Book Ratio (P/B), and Debt-to-Equity Ratio provide valuable insights into the company's performance and market position. Understanding the company's financial health is fundamental to valuation.

Q: Why not private equity, growth equity, hedge funds, or entrepreneurship? Growth equity is a bit closer, but you’re more interested in early-stage companies that need VC support rather than already successful companies that need more capital. Q: What’s the difference between pre-money and post-money valuations?

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. OK, now to the good news: This situation is starting to change.

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equity risk premiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time.

The median market value of equity (MVE) for dividend-paying stocks was $133 million, and the average MVE was $248 million. There is no information in any restricted stock study to help business appraisers estimate the value of expected future dividends. And what about the terminalvalue that gives rise to capital appreciation?

This is a summary statement of the discounted cash flow model in which normalized expected cash flows of the business are projected into the future for a finite period of time and then, a terminalvalue is calculated to represent the then value of all remaining cash flows beyond the finite forecast period.

The value of an interest in a business is a function of the expected cash flows to the interest (which are derivative of the expected cash flows of the business itself, the growth of those cash flows, including a terminalvalue at the end of an expected holding period, and the risks associated with achieving those cash flows.

Oil & Gas Investment Banking Definition: In oil & gas investment banking, professionals advise companies that search for, produce, store, transport, refine, and market energy on raising debt and equity and completing mergers and acquisitions. Midstream: 85 (mix of asset deals, M&A, debt, and even some private equity activity).

Otherwise, the appraiser is not valuing the appropriate asset. Assume further that the appropriate EBITDA multiple is 6x and that the underlying equity discount rate is 14%. This is the only way that hypothetical buyers can understand the value of the entire asset, a small interest of which they are buying. million (6 x $2.0

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content