This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equityriskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

Definition of EquityRiskPremium. It is the difference between expected returns from the stock market and the expected returns from risk-free investments. What Impacts the EquityRiskPremium? How Do You Calculate EquityRiskPremium? The post What Is EquityRiskPremium?

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What?

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

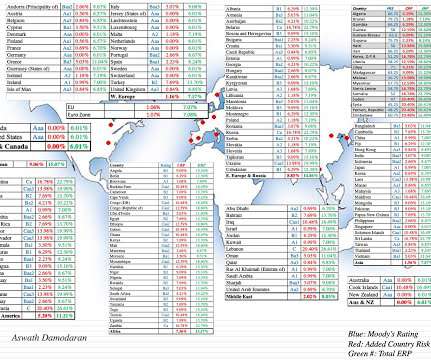

Country Risk: EquityRisk For equity investors, the price of risk is captured by the equityriskpremium, and equityriskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

Some of these differences across sectors reflect reversals from the damage done in 2022, but some of it is reflective of the disparate impact of inflation and higher rates across companies Finally. trillion increase in value US equities, the seven companies that we listed earlier accounted for $3.7

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

It helps an investor understand what to expect to earn in relation to the risk-freerate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-freerate by buying the risk-free asset. How Do You Calculate the Capital Asset Pricing Model? E(r) = Rf + ??(Rm

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums.

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. In fact, there are about a dozen countries that are unrated, where I have used their PRS scores to make estimates of their equityriskpremiums.

Beyond the 10-year maturity, the slope of the yield curve actually flattened out, with the difference between the 30-year rate and the 10-year rate declining by 0.34%. Note that the decrease in default spreads, at least for the lower ratings, mirrors the drop in the implied equityriskpremium during the course of 2021.

Investment Consequences As the storm clouds of higher inflation and interest rates, in conjunction with slower or even negative economic growth, gather, it should come as no surprise that equity markets are struggling to find their footing. At the close of trading on May 5, 2022, the S&P 500 stood at 4147, down 13.3%

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-freerate, cost of equity, or cost of debt, are used contextually in financial analysis.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors.

The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. Investors construct portfolios with unsystematic risks, which are well-diversified to reduce total portfolio risk. Inflation rate: ß = 0.6, The risk-freerate is 5%.

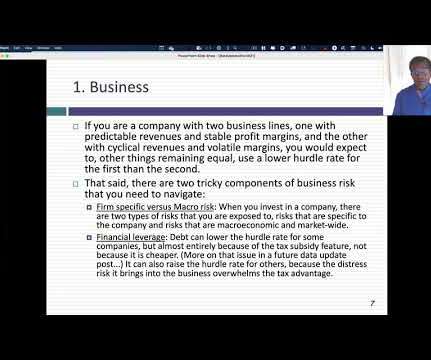

Cost of raising funds (capital) : Since the funds that are invested by a business come from equity investors and lenders, one way in which the hurdle rate is computed is by looking at how much it costs the investing company to raise those funds. But what if the company is looking at a project in Nigeria or Bangladesh? for Ford).

A firm uses a mix of equity and debt to minimize the cost of capital. In general, the cost of debt is lower than the cost of equity due to the tax advantage of debt. The cost of capital also reflects the riskiness of a firm which reflects the required rate of return. WACC is also viewed as appropriate for a discount rate.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

To evaluate a company's value, using the cash flow discounting method, the future cash flows that the firm will generate must be estimated and capitalized at a discount rate appropriate to the firm's risk. The price of equity represents the return shareholders demand on an investment in the company.

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the Terminal Value calculation). And Equity Real Estate Investment Trusts (REITs) must distribute almost all their Net Income, so the DDM can work well in REIT valuations.

Risk : When I valued Tesla last in early 2020, I used a cost of capital of 7%, reflecting a riskfreerate of 1.75% and an equityriskpremium of 5.2% Rather than take issue with my valuation, put your inputs into the attached spreadsheet and estimate your value of equity for the firm.

It is to remedy this defect that analysts scale profits to invested capital, with equity and capital variants: In the equity version, you divide net income by book equity to estimate a return on equity, a measure of what equity investors are generating on the capital they have invested in a company.

In its early years, Tesla was dependent on equity issuances for funding growth investments, and its liberal use of options to reward management (and especially Elon Musk) opened it up to criticism. The Market : The US equity market in January 2023 looks very different from the market at the start of 2022. per share in 2022.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

Ce = Cost of Equity. Rf = Risk-freeRate. Rm – Rf) = Equity Market RiskPremium. Cp = Cost of EquityPremium. Ce = Cost of Equity. E = Equity . t = Tax Rate. Add these to get the free cash flow for that single year (or particular period, like 6 months).

The first of the is as companies scale up, there will be a point where they will hit a growth wall, and their growth will converge on the growth rate for the economy. In short, I am assuming that the price cuts and cost pressures of the fourth quarter are more representative of what Tesla will face in the future, as competition steps up.

Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time. Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

Just to illustrate the contradictions that can result, PRS gives Libya a country risk score that is higher (safer) than the scores it gives United States or France, putting them at odds with most other services that rank Libya among the riskiest countries in the world.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. Riskfree rate will rise.

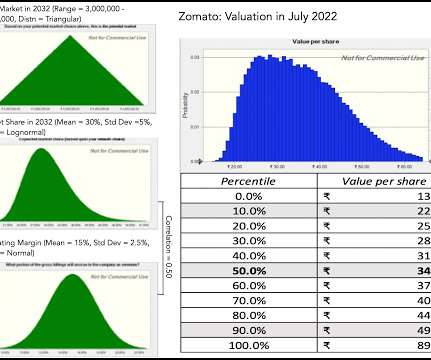

grow at the cost of equity), yielding about ?46 The effects of inflation show up first as higher riskfreerates , across currencies, and next in higher riskpremiums, with both equityriskpremiums and default spreads rising. higher (i.e., 46 in July 2022. 2% from my IPO valuation.

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

Using a different lexicon, the price of risk in the bond market decreased during the course of the year, and if you relate that back to my second data update, where I computed a price of risk for equity markets (the equityriskpremium), you can see the parallels.

It determines the price per share, dictating how much equity founders concede in exchange for the capital raised. [3] 3] , [7] , [6] It sets a benchmark against which future fundraising rounds will be measured and helps investors assess whether the potential upside justifies the significant risks associated with early-stage ventures. [8]

2] Startups typically lack significant historical financial data, often operate with negative profits initially, rely heavily on private equity or venture capital rather than traditional bank loans, and face a much higher risk of failure. [1] This premium rises when perceived market risk increases. [27] 2] [15] [17].

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content