This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Definition of Risk-FreeRate. The risk-freerate is the minimum rate of return on an investment with theoretically no risk. Government bonds are considered risk-free because technically, a government can always print money to pay its bondholders. Treasury Bill. 10-Year U.S.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a riskfree investment? Why does the risk-freerate matter?

If you have been reading my posts, you know that I have an obsession with equityrisk premiums, which I believe lie at the center of almost every substantive debate in markets and investing. How, you may ask, can equityrisk premiums be that divergent, and does that imply that anything goes?

Put simply, no central bank, no matter how powerful, can force market interest rates down, if inflation expectations stay low, or up, if investor are anticipating high inflation. Note that the decrease in default spreads, at least for the lower ratings, mirrors the drop in the implied equityrisk premium during the course of 2021.

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. Stocks: The What?

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. As a result, treasury bond investors faced one of their worst years in history, losing close to a fifth of their principal, as bonds were repriced.

The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023. At the start of October, the ten-year and thirty-year rates were both approaching 15-year highs, with the 10-year treasury at 4.59% and the 30-year treasuryrate at 4.73%.

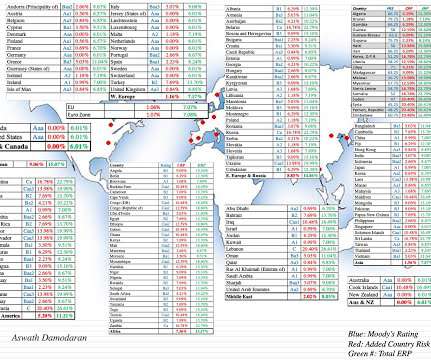

Country Risk: EquityRisk For equity investors, the price of risk is captured by the equityrisk premium, and equityrisk premiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

There are three possible explanations for the divergence: Short term versus Long term : The consumer survey extracts an expectation of inflation in the near term, whereas the treasury markets are providing a longer term perspective, since I am using ten-year rates to derive the market-implied inflation.

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasuryrates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. for 2021 and inflation of 2.2%

While the Federal Open Market Committee controls the Fed Funds rate, there are a whole host of rates set by buyer and sellers in bond markets. In fact, in the quarters after the Fed Funds rate increases, US treasuryrates (short and long term) are more likely to decrease than increase, and the median change in rates is negative.

While everyone seems to know about equity research and trading stocks, fixed income research gets far less attention. Equity Research vs. Fixed Income Research Common Myths What Do You Do as a Fixed Income Research Analyst or Associate? a credit rating vs. an investment recommendation). closer to the work at a quant fund ).

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery. The Fed Effect: Where's the beef?

Risk Premiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equityrisk premium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasuryrates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

Ce = Cost of Equity. Rf = Risk-freeRate. Rm – Rf) = Equity Market Risk Premium. Cp = Cost of Equity Premium. Ce = Cost of Equity. E = Equity . t = Tax Rate. Depending on the exact methodology and discount rate used, this could be the Enterprise Value or Equity Value.

Just to illustrate the contradictions that can result, PRS gives Libya a country risk score that is higher (safer) than the scores it gives United States or France, putting them at odds with most other services that rank Libya among the riskiest countries in the world.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

In this post, I will begin by looking at movements in treasuryrates, across maturities, during 2024, and the resultant shifts in yield curves. I will follow up by examining changes in corporate bond rates, across the default ratings spectrum, trying to get a measure of how the price of risk in bond markets changed during 2024.

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content