This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equityrisk premiums, which I believe lie at the center of almost every substantive debate in markets and investing. How, you may ask, can equityrisk premiums be that divergent, and does that imply that anything goes?

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. at the start of that year.

We started the year with significant uncertainty about whether the surge in inflation seen in 2022 would persist as well as about whether the economy was headed into a recession. The NASDAQ also gave back gains in the third quarter, but is up 27.27% for the year, but those gaudy numbers obscure a sobering reality.

Inflation: Measurement and Determinants As the inflation debate was heating up in the middle of last year, I wrote a comprehensive post on how inflation is measured, what causes it and how it affects returns on different asset classes. Rather than repeat much of that post, let me summarize my key points.

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors.

Convertible bonds are hybrid instruments with elements of debt and equity, and some groups that trade convertible bonds also combine elements of S&T and IB. But before delving into the best candidates for these roles, typical trades, careers, and more, let’s start with the basic definitions: What is a Convertible Arbitrage Hedge Fund?

Investors all talk about risk, but there seems to be little consensus on what it is, how it should be measured, and how it plays out in the short and long term. In closing, I will talk about some of the more dangerous delusions that undercut good risk taking. What is risk?

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. for 2021 and inflation of 2.2%

In most time periods, those recalibrations and resets tend to be small and in both directions, resulting in the ups and downs that pass for normal volatility. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

While everyone seems to know about equity research and trading stocks, fixed income research gets far less attention. Equity Research vs. Fixed Income Research Common Myths What Do You Do as a Fixed Income Research Analyst or Associate? a credit rating vs. an investment recommendation). closer to the work at a quant fund ).

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. Thus, I took a detour to value Tesla , around the time of their most recent earnings report on January 26, and added a second post to respond to the pushback that I got.

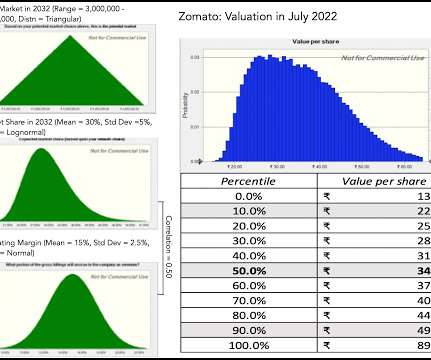

grow at the cost of equity), yielding about ?46 In addition, the growth has come in fits and starts, and given Zomato's active acquisition strategy, it is not clear how much of the revenue growth is organic and how much is acquired. higher (i.e., 46 in July 2022.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of risk premiums.

The truth, though, is that the Fed sets only one interest rate, the Fed Funds rate, and that none of the rates that we face in our lives, either as consumers (on mortgages, credit cards or fixed deposits) or businesses (business loans and bonds), are set by or even indexed to the Fed Funds Rate.

When I started offering financial modeling training , I never expected to get questions about a methodology like the Dividend Discount Model (DDM). It can be useful for certain companies, such as power and utility firms and midstream (pipeline) operators in oil & gas … …but it’s also much harder to set up and use than a standard DCF.

As I have valued Tesla over the years, I have come to the realization that it is the most 'uncar-like" automobile company in the world, and its uniqueness shows up on two dimensions. Put simply, the company has been able to scale up more quickly, while reinvesting less in capacity, than any other automobile company.

Thus, almost everything I know and practice, when valuing young and start-up companies, I learned in the process of valuing Amazon in the 1990s. Just as impressively, the company finally started delivering on its promise of profitability, going from barely making money in 2019 to an operating margin of 16.57% in 2022.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery. The Fed Effect: Where's the beef?

To set the stage, I will start by laying out the differences measure of earnings that reported on an income statement: At the top of the profit ladder is gross income , the earnings left over after a company has covered the direct cost of producing whatever it sells.

Use of Special purpose acquisition (SPAC) vehicles have spiked over the past year because private equity and venture capital firms have excess cash they need to put to work, accounting practitioners said mid-June. These standards require companies to assess whether the warrants should be equity or liability classified.

The first of the is as companies scale up, there will be a point where they will hit a growth wall, and their growth will converge on the growth rate for the economy. Firms with large revenues find it difficult to maintain high growth, as they scale up. On both fronts, I am more cautious.

I also start thinking about my passion, which is teaching, the spring semester to come, and the classes that I will be teaching, repeating a process that I have gone through every year since 1984, my first year as a teacher. Face up to uncertainty, rather than avoid or deny it : Uncertainty is a feature of investing/ business, not a bug.

In fact, the standard practice that most analysts and investors follow to estimate the riskfreerate is to use the government bond rate, with the only variants being whether they use a short term or a long term rate. where I looked at the possibility that we live in a world where nothing is truly riskfree.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

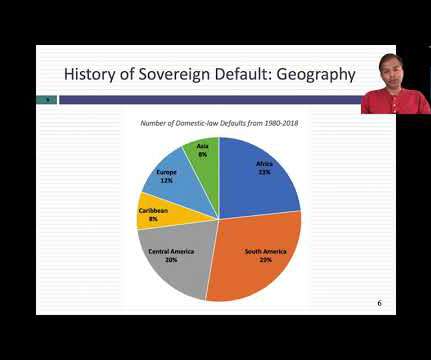

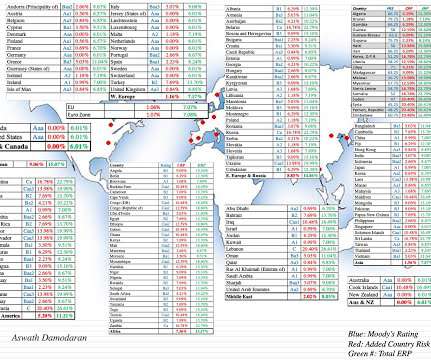

It has been my practice for the last two decades to take a detailed look at how risk varies across countries, once at the start of the year and once mid-year. Country Risk: Default Risk and Ratings For investors, the most direct measures of country risk come from measures of their capacity to default on their borrowings.

In my last three posts, I looked at the macro (equityrisk premiums, default spreads, riskfreerates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In this post, I will start by looking at the role that hurdle rates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdle rates to vary across companies.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

The share price is up 35% YTD. Western countries fear that Russia starts to gain control over Ukraine again. Germany delayed the approval as it uses the pipeline as a sanction threat in case Russia starts a war. Its net-debt to equity ratio stood at 0.3 Russia has a massively high risk-freerate of 10%.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings! Sometimes, less is more!

First, these categorizations were created close to twenty years ago, when I first started looking a global data, and many countries that were emerging markets then have developed into more mature markets now. Beta & Risk 1. Return on Equity 1. EquityRisk Premiums 2. Ratings & Spreads 2. Tax rates 4.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound. Analysts often try to bring company-specific components, i.e,

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of market capitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

Since country risk is multidimensional and dynamic, my annual country risk update runs to more than a hundred (boring) pages , but I will try to summarize what the last year has brought in this post. Drivers of Country Risk What makes some countries riskier than others to operate a business in?

It was an interesting year for interest rates in the United States, one in which we got more evidence on the limited power that central banks have to alter the trajectory of market interest rates. We started 2024 with the consensus wisdom that rates would drop during the year, driven by expectations of rate cuts from the Fed.

The results, broken down broadly by geography are in the table below: As you can see, the aggregate market cap globally was up 12.17%, but much of that was the result of a strong US equity market. I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content