This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The S&P 500 currently trades at a price to book value of 4.2, suggesting that book value accounts for less than 20% of the S&P 500’s market value. The remaining 80%, appears nowhere in these firms’ balance sheets—it is invisible to contemporary accounting techniques and constitutes “dark accounting matter.”

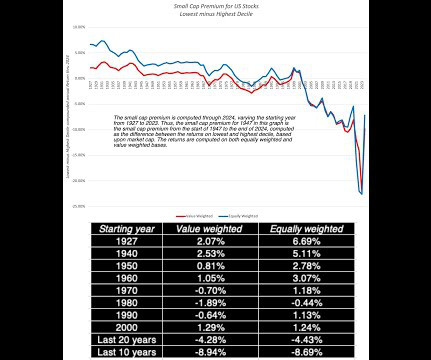

In my last post , I discussed how inflation's return has changed the calculus for investors, looking at how inflation affects returns on different asset classes, and tracing out the consequences for equity values, in the aggregate. The former is short hand for the small cap premium and the latter is the proxy for the value factor in returns.

Significantly, Mizuho CEO Masahiro Kihara said the bank will either pass on the proceeds from its sales of equity holdings to investors as dividends or invest them in growth-directed activities, and Sumitomo Mitsui aims to reduce the market value of its equity holdings to less than 20% of the value of its consolidated net assets.

In my second data update post from the start of this year , I looked at US equities in 2022, with the S&P 500 down almost 20% during the year and the NASDAQ, overweighted in technology, feeling even more pain, down about a third, during the year. US Equities in 2023: Into the Weeds! that was lost last year.

Corporate Bonds: No Shortage of Risk Capital In my last post, I chronicled the movement in the equity risk premium, i.e. the price of risk in the equity market, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

Jeremy Stuber is a global equity analyst at Newton Investment Management , leading on valuation and accounting issues across all sectors. Searching for stocks with low price-to-book ratios was a good indication of a potential bargain. Comment: The importance of (and challenges with) valuing intangibles.

This evaluation is pivotal because it dictates the terms of investment, directly influencing how much equity (ownership) a founder must relinquish in exchange for funding from the Sharks. Conversely, a lower valuation may require founders to give up more equity.

Analysts use financial metrics and multiples such as Price to Earnings (P/E), Price to Book (P/B), Enterprise Value to Sales (EV/Sales), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios derived from trading data of similar public companies or deal pricing data of similar M&A transactions.

Different Methods of Benchmark Valuation There are several ways to conduct a benchmark valuation, each with its unique focus and methodology: Price-to-Earnings Ratio (P/E) The P/E ratio compares a company’s current share price to its earnings per share (EPS). Investors compare stock prices to similar companies or industry standards.

Understanding the Concept: In essence, FCFF encapsulates the cash that can be distributed to both debt and equity holders after meeting operational needs and capital expenditures. The resulting value represents the cash available to all contributors of capital—both debt and equity. What is Free Cash Flow to Equity?

I do report on a few market-wide data items especially on risk premiums for both equity and debt. I also report on pricing statistics, again broken down by industry grouping, with equity (PE, Price to Book, Price to Sales) and enterprise value (EV/EBIT, EV/EBITDA, EV/Sales, EV/Invested Capital) multiples.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

Looking at US equities, the S&P 500 is up about 11% and the NASDAQ about 5%, from start of the year levels, and the underperformance of the latter has led to a wave of stories about whether this is start of the long awaited comeback of value stocks, after a decade of lagging growth stocks.

Book value is the value attributable to shareholders in case the company sells all its assets and repays its liabilities (also called liquidation value). A price-to-book ratio of less than 1x indicates that the market values the net assets less than the balance sheet suggests. What does a PB-ratio of less than 1x indicate?

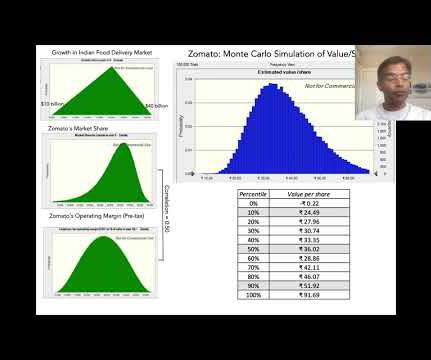

Uber's ownership in Zomato is a result of Zomato's acquisition of Uber Eats India, where Uber received a share of Zomato's equity in exchange. Finally, dismissing Zomato as an investment, just because it does not make money now, or fails to meet some conventional value tests on pricing (PE, Price to Book), is investing malpractice.

Key Financial Ratios: Ratios such as Price-Earnings Ratio (P/E), Price-to-Book Ratio (P/B), and Debt-to-Equity Ratio provide valuable insights into the company's performance and market position. Understanding the company's financial health is fundamental to valuation.

In this post, I will begin by looking at how to value banks and follow up with an examination of investor views of banking have changed, by looking at pricing, before examining divergences in how banks are priced in the market today. All Equity, All the time!

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. Those rates stayed low through the rest of 2020, even as equity markets recovered and corporate bond spreads fell back to pre-crisis levels. to close to zero, and the ten-year T.Bond rate declining to close to 0.70%.

In this post, I will begin with a historical assessment of stock returns in the recent past, then move on to evaluate the returns that investors can expect to make, given how they are priced at the start of 2022, and end with a do-it-yourself valuation of the index right now. The year that was.

In this section, I will begin by looking at the bond market effects and then move on to equities and other asset classes, starting by looking at the localized reaction (for Ukranian and Russian securities) and then the global ripple effects. As Russian equities have imploded, the ripple effects again are being felt across the globe.

For the market, it is often built on papers (or books) that look at the historical data on what equity markets have delivered as returns over long periods, relative to what you would have made investing elsewhere.

The first was the response that I received to my last data update , where I looked at the profitability of businesses, and specifically at how a comparison of accounting returns on equity (capital) to costs of equity (capital) can yield a measure of excess returns.

Adani's Debt Load The investment side of the Adani story is not complete without bringing in the financing part, since the money for these investments has to come from somewhere, either internally, residual cash flows from existing operations, or externally, from new debt or equity.

In my first two data posts for 2025, I looked at the strong year that US equities had in 2024, but a very good year for the overall market does not always translate into equivalent returns across segments of the market. In this post, I will remain focused on US equities, but I will break them into groupings, looking for differences.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content