This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equityriskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

Definition of EquityRiskPremium. It is the difference between expected returns from the stock market and the expected returns from risk-free investments. What Impacts the EquityRiskPremium? How Do You Calculate EquityRiskPremium? The post What Is EquityRiskPremium?

It is the nature of stocks that you have good years and bad ones, and much as we like to forget about the latter during market booms, they recur at regular intervals, if for no other reason than to remind us that risk is not an abstraction, and that stocks don't always win, even in the long term. Stocks: The What?

That recovery notwithstanding, uncertainties about inflation and the economy remained unresolved, and those uncertainties became part of the market story in the third quarter of 2023. The Markets in the Third Quarter Coming off a year of rising rates in 2022, interest rates have continued to command center stage in 2023.

I am not a market prognosticator for a simple reason. I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis.

As inflation has taken center stage, markets have gone into retreat globally, and across asset classes. In 2022, as bond rates have risen, stock prices have fallen, and crypto has imploded, even true believers are questioning what the bottom for markets might be, and when we will get there.

By the start of 2022, the window for early action had closed and for much of this year, inflation has been the elephant in the room, driving markets and forcing central banks to be reactive, and its presence has already induced me to write three posts on its impact.

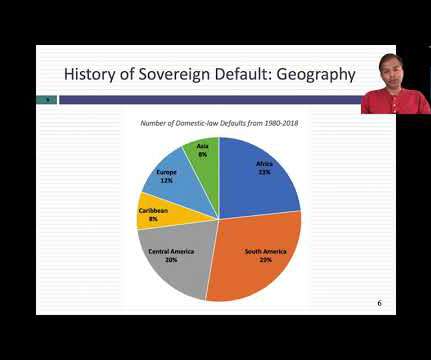

In the month since, I have added two more data updates, one on US equities and one on interest rates , but my attention was drawn away by other interesting stories. Default Risk As with individuals and businesses, governments (sovereigns) borrow money and sometimes struggle to pay them back, leading to to the specter of sovereign default.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Energy, one of the few survivors of the 2022 market sell-off, had a bad year, as did utilities and consumer staples. increase in market capitalization.

The nature of markets is that they are never quite settled, as investors recalibrate expectations constantly and reset prices. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

Investors are constantly in search of a single metric that will tell them whether a market is under or over valued, and consequently whether they should buying or selling holdings in that market. Note that nothing that I have said so far is premised on modern portfolio theory, or any academic view of riskpremiums.

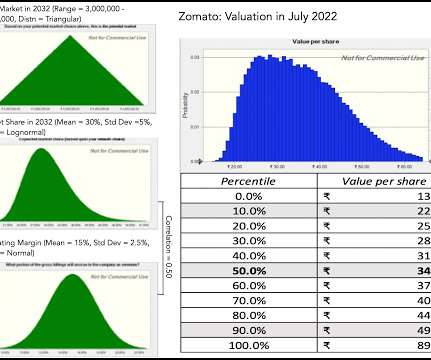

The market clearly had a very different view, as the stock premiered at ? I argued then that notwithstanding the potential growth in the market, and Zomato's advantageous positioning, it was being over priced for its IPO, at ? grow at the cost of equity), yielding about ?46 41 per share. 169 per share in late 2021. higher (i.e.,

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors. in 2022, higher than the 1- 1.5%

In leveraged buyouts (LBOs), a private equity (PE) sponsor acquires controlling ownership of a target company, typically by using a significant amount of bank loans. The findings of our study have important implications for debates about the role of private equity firms.

It helps an investor understand what to expect to earn in relation to the risk-free rate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-free rate by buying the risk-free asset. Investments are exposed to two types of risk: systematic and unsystematic. E(r) = Rf + ??(Rm

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-free rate, cost of equity, or cost of debt, are used contextually in financial analysis.

The first quarter of 2021 has been, for the most part, a good time for equitymarkets, but there have been surprises. The Interest Rates Story To me the biggest story of markets in 2021 has been the rise of interest rates, especially at the long end of the maturity spectrum.

By the end of 2021, it was clear that this bout of inflation was not as transient a phenomenon as some had made it out to be, and the big question leading in 2022, for investors and markets, is how inflation will play out during the year, and beyond, and the consequences for stocks, bonds and currencies.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery. In fact, treasury bill rates consistently rise ahead of the Fed's actions over the two years.

The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. Investors construct portfolios with unsystematic risks, which are well-diversified to reduce total portfolio risk. In theory, arbitrage provides investors with a high chance of success. 1 + RP1 + ??2+

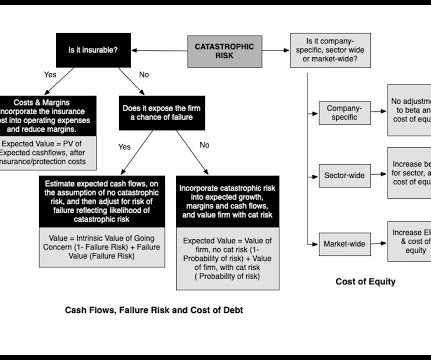

Deconstructing Risk While we may use statistical measures like volatility or correlation to measure risk in practice, risk is not a statistical abstraction. Its impact is not just financial, but emotional and physical, and it predates markets. 4 & 5 Uninsurable Risk.

I have been writing about, and valuing, Tesla for most of its lifetime in public markets, and while it remains a company that draws strong reactions, it is also one that I truly enjoy valuing. Tesla: The Back Story I first valued Tesla in 2013 , as a "luxury automobile company" and I have valued almost every year since.

My last valuation of Tesla was in November 2021, towards its market peak, and given its steep fall from grace, in conjunction with Elon Musk's Twitter experiment, it is time for a revisit.

A firm uses a mix of equity and debt to minimize the cost of capital. In general, the cost of debt is lower than the cost of equity due to the tax advantage of debt. The cost of equity (Ke) is an expected return that a firm pays to an equity investor to compensate for the risk of investing capital.

In Finance - the beta represents how sensitive the stock price is concerning the market price change (index). The beta measures the return of the stock relative to the market return. For example, when the stock market goes up 1%, and the stock goes up 0.5%, then the stock beta is equal to 0.5.

It is to remedy this defect that analysts scale profits to invested capital, with equity and capital variants: In the equity version, you divide net income by book equity to estimate a return on equity, a measure of what equity investors are generating on the capital they have invested in a company.

And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the Terminal Value calculation). And Equity Real Estate Investment Trusts (REITs) must distribute almost all their Net Income, so the DDM can work well in REIT valuations.

With limited features and formulas, it can be difficult to account for all the necessary parameters in a valuation, such as interest rates, equityriskpremiums, and beta. Additionally, Excel does not have market analysis reports or all the necessary parameters to create an accurate valuation.

In selecting the appropriate equityriskpremium, the court observed that whether to use supply-side or historical ERP should be determined on a case-by-case basis.

But here, we use what interest we could get from an alternative investment in the market, called the Market Rate. Discount Factor (using Market Rate: r=10%). But first, a quick aside, which you can feel free to skip if you want to jump ahead: Why Do We Use the Market Rate to Calculate the Discount Factor? E = Equity .

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equityriskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. It was the reason that I argued at a $1.2

I take the point of view that uncertainty should not stop you from valuing companies, that your value estimates will have more error in them, but since the market also faces the same uncertainty, your best bargains may be in the midst of uncertainty. That tells me three things.

In my last post , I described the wild ride that the price of risk took in 2020, with equityriskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

The second and third musings address the issue of marketability discounts and conclude that it is not possible to comply with any valuation standards, whether USPAP or not, using only averages of restricted stock studies as a basis for “guessing” marketability discounts. The relevant pool of potential buyers, if any.

If equitymarkets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equitymarkets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

It helps owners determine the fair market value of their business, which is essential when considering a sale, merger, or acquisition. Market Conditions and Industry Trends Evaluating the current market conditions and industry trends is critical in assessing the value of a tax preparation business.

Geographic Location and Market Demand The geographic location of a disaster restoration business plays a significant role in its valuation. The local market dynamics, competition, and potential for future growth are crucial factors to consider when valuing a business. The total value of these assets forms the basis for the valuation.

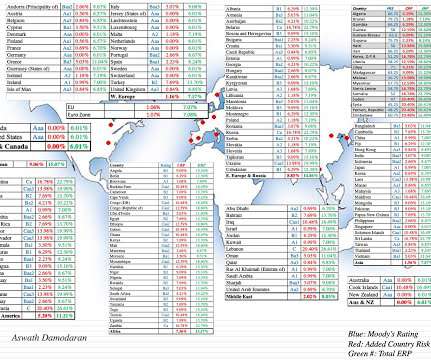

Country Risk: EquityRisk For equity investors, the price of risk is captured by the equityriskpremium, and equityriskpremiums will vary across countries. Please do not attach any political significance to my country groupings, or take them personally.

He is the Director of the Pepperdine Private Capital Markets Project (privatecap.org) and Executive Director for the Pepperdine Most Fundable Companies competition (pepperdine.edu/mfc). His teaching and research interests include entrepreneurial finance, private capital markets, and entertainment finance. Dr. Everett He holds a Ph.D.

Expected returns for Risky Investments : The risk-free rate becomes the base on which you build to estimate expected returns on all other investments. For instance, if you read my last post on equityriskpremiums , I described the equityriskpremium as the additional return you would demand, over and above the risk free rate.

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

As we approach the mid point of 2021, financial markets, for the most part, have had a good year so far. All of these measures, no matter how carefully designed, give a measure of inflation in the past, and markets are ultimately concerned more with inflation in the future.

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content