This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Significant volatility continues to disrupt the equitymarkets, with the major stock indexes swinging multiple percentage points often on a daily basis. This additional regulatory delay means that transactions, and in particular deals involving stock consideration, are increasingly vulnerable to marketrisk over a longer time horizon.

Over the past few decades, growth equity (GE) has gone from an afterthought to a major asset class for huge investment firms. Some argue that GE offers the best of both worlds: the opportunity to fund innovation and growth – as in venture capital – plus the ability to limit downside risk and invest in proven companies – as in private equity.

They all think they can make a fortune buying and selling stocks; in other words, they’re fans of the long/short equity strategy. When the average person thinks of hedge funds, long/short equity is often the first thing that comes to mind. Probably 90% of hedge fund stock pitches use long/short equity or related strategies.

On the flip side, if the merger generates synergies and increased profitability, debt financing can yield substantial rewards, as debt is often lower than equity. Equity Financing: Dilution vs. Stability Equity financing involves issuing new shares to raise capital for the M&A transaction.

If an investor moves money from the risk-free asset into the stock market, they should expect to earn a return in excess of the risk-free rate, what is called an equityrisk premium. Investments are exposed to two types of risk: systematic and unsystematic. What Impacts the Capital Asset Pricing Model?

Convertible bonds are hybrid instruments with elements of debt and equity, and some groups that trade convertible bonds also combine elements of S&T and IB. If you’re using a strategy like long/short equity , you could long or short a company’s stock, and your results would depend heavily on the stock market’s overall direction.

The discount rate effectively encapsulates the risk associated with an investment; riskier investments attract a higher discount rate. Different types of discount rates such as risk-free rate, cost of equity, or cost of debt, are used contextually in financial analysis.

For policymakers, our findings suggest that the token market may to some extent become more efficient on its own because intermediaries reduce costly frictions and have an incentive to do so because they benefit from above-marketrisk-adjusted returns. This post comes to us from Paul P.

A firm uses a mix of equity and debt to minimize the cost of capital. In general, the cost of debt is lower than the cost of equity due to the tax advantage of debt. The cost of equity (Ke) is an expected return that a firm pays to an equity investor to compensate for the risk of investing capital.

First, note that these terms apply only to investment banks and related finance firms (private equity firms, hedge funds, etc.). Saying that you work in “the front office” of a technology company or a marketing firm makes little sense – or, at least, it means something different from the definitions in this article.

Cost of Equity and Capital: The Terminal Growth Rate is used to calculate the cost of equity in the Dividend Discount Model (DDM) and the cost of capital in the Weighted Average Cost of Capital (WACC) formula. Market Maturity: Mature industries, like utilities or traditional consumer goods, tend to have lower Terminal Growth Rates.

Significant volatility continues to disrupt the equitymarkets, with the major stock indexes swinging multiple percentage points often on a daily basis. We outline below certain transaction structures that can be deployed to shift or address certain of these risks to account for the greater volatility in the current market environment.

Factors such as market growth, competitive landscape, product innovation, and expansion opportunities can all affect the company’s value. Risk Factors: Evaluating the risks associated with the business, including marketrisks, operational risks, legal risks, and financial risks, is essential in determining its value.

There would be no change in the capital framework for smaller firms, except that those firms with significant trading activities would be subject to the market-risk capital provisions. This new approach would include standardized risk-weights for credit, equity, operational, and credit valuation adjustment risk.

Ce = Cost of Equity. Rf = Risk-free Rate. Rm – Rf) = EquityMarketRisk Premium. Cp = Cost of Equity Premium. Ce = Cost of Equity. E = Equity . Depending on the exact methodology and discount rate used, this could be the Enterprise Value or Equity Value. Market Return.

Transaction costs have come down, and efficiency and fairness have increased in many markets. However, increased use of, and reliance on, technology has introduced new risks and, in some cases, amplified better-known marketrisks. Similarly, markets are more interconnected and interdependent than ever.

Private Funds : Exams observed that more than 5,000 registered investment advisers (RIAs) manage roughly $18 trillion in private fund assets in strategies that include hedge funds, private equity funds, and real estate funds, whose investors include state and local pensions, family beneficiaries, charities, and endowments.

We did it in the 1960s when we first offered guidance on disclosure related to risk factors. [12] 12] We did so in the 1970s regarding disclosure related to environmental risks. [13] 14] We did it again in the 1990s when we required disclosure about executive stock compensation [15] and in 1997 regarding marketrisk. [16]

Financing the Acquisition Funding Options There are several funding options available, including bank loans, private equity, and seller financing. Common pitfalls include overlooking intangible assets, underestimating operational inefficiencies, and failing to account for marketrisks.

For the cost of capital, I followed the traditional route of estimating the company's costs of equity (based upon its exposure to marketrisk) and after-tax cost of debt, to arrive at an initial cost of capital of 10.25%, which I lowered over time to 8.97%, with both numbers in Indian rupees.

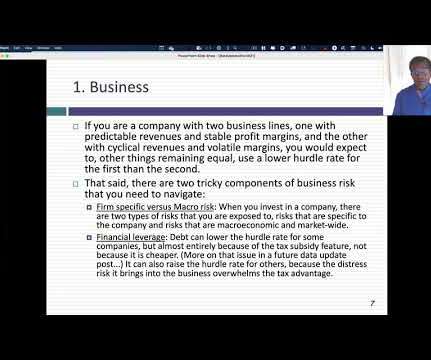

Cost of raising funds (capital) : Since the funds that are invested by a business come from equity investors and lenders, one way in which the hurdle rate is computed is by looking at how much it costs the investing company to raise those funds. as mature markets.

The risk that a party may have to make or receive future payment(s) based on the evolution of the referenced variable is called “marketrisk.” This would recognize offsetting marketrisk – potentially with conservatism built into the model. As part of rulemaking and lower-level relief (e.g.,

Innovation: AI-Based Fund Monitoring Company: Eurasian Bank In Kazakhstan, would-be homeowners often engage in shared-equity construction, a process in which future owners buy shares in a house under construction. Launched in March 2024, the chatbot is dynamic, meaning it improves the more it is used.

Possible Role for Private Equity In contrast to the aftermath of the 2008 financial crisis, we have not yet seen private equity investors play a significant role during the recent turmoil. Some large private equity firms have said publicly that they are interested in providing capital to regional banks by buying loan assets.

Dr. Henry has over 20 years of diverse experience in the fields of business economics, consulting/advisory services, interest rate and marketrisk modeling, and government affairs. Mr. Fries specializes in private-equity related valuations as well as providing valuations in the context of partner buy-outs and disputes.

In my last data updates for this year, I looked first at how equitymarkets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

Further, while US regulators initially signaled that capital levels would not be materially impacted by the Endgame Standard, the Capital Proposal is now expected to increase common equity Tier 1 (“CET1”) capital by around 16% for banking organizations subject to the Capital Proposal.

Of most importance for financial institutions, the identified categories also include downstream activities such as “investments” (Category 15 of the GHG Protocol’s Scope 3 emissions categories), which would capture financed emissions ( i.e. , emissions from companies to which the financial institution provides debt or equity financing).

The Hurdle Rate - Intuition and Uses You don't need to complete a corporate finance or valuation class to encounter hurdle rates in practice, usually taking the form of costs of equity and capital, but taking a finance class both deepens the acquaintance and ruins it. Corporate Default Risk , i.e,

Introduction: Why ESOP Valuations Matter Startup founders often focus on product development, market fit, and fundraisingrightly so. Yet one of the critical elements that intersects nearly all these aspects is the valuation of the companys equity. By presenting a conservative but defensible valuation, the startup can mitigate risk.

When Continental suddenly collapsed in May 1984, rather than place the bank into receivership, it was supported by an equity injection from the FDIC and a consortium of other banks, extensive borrowing from the Federal Reserves Discount Window, and a blanket guarantee on its uninsured deposits and general creditors by the FDIC.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content