This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While there are many events during 2022, some political and some economic, that one can point to as the reason for poor stock returns, it is undeniable that inflation was the driving force behind the market correction. In this section, I will begin with a deconstruction of stock returns in 2022 and the year's place in stock market history.

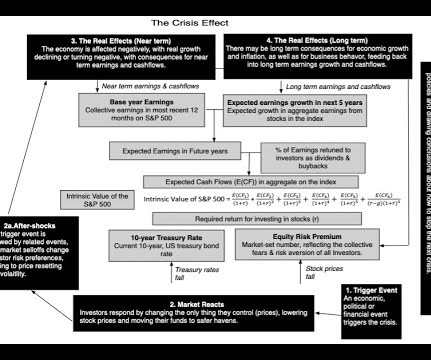

While this may seem perverse, the first step in understanding and assessing where we are in markets now is to go back and examine where things stood then. In my third post at the start of 2023, I looked at US treasuries, the long-touted haven of safety for investors. trillion below their values from the start of 2022.

Put simply, no central bank, no matter how powerful, can force market interest rates down, if inflation expectations stay low, or up, if investor are anticipating high inflation. Note that the decrease in default spreads, at least for the lower ratings, mirrors the drop in the implied equity risk premium during the course of 2021.

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Energy, one of the few survivors of the 2022 market sell-off, had a bad year, as did utilities and consumer staples. increase in marketcapitalization.

The Market Reaction As the rhetoric of war has heated up in the last few months, markets were wary about the possibility of war, but as Russian troops have advanced into the Ukraine, that wariness has turned to sell off across markets. As Russian equities have imploded, the ripple effects again are being felt across the globe.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

The first quarter of 2021 has been, for the most part, a good time for equitymarkets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation.

In my last post , I discussed how inflation's return has changed the calculus for investors, looking at how inflation affects returns on different asset classes, and tracing out the consequences for equity values, in the aggregate.

The overarching questions for us all are whether this crisis will spread to the rest of the economy and market, as it did in 2008, and how banking as a business, at least in the US, will be reshaped by this crisis, and while I am more a dabbler than an expert in banking, I am going to try answering those questions.

Regional Breakdown My data sample for 2022 includes every publicly traded firm that is traded anywhere in the world, with a marketcapitalization that exceeds zero. For debt markets, it takes the form of default spreads, and I report the latest estimates of these corporate bond spreads at this link.

In standard public equity securities, even the most naïve investor is protected, first, by the market price – you pay only for what you get – and, second, by the comfort that nothing else is required of an individual investor to realize the full value of the security. securities markets – not SPACs.

What GameStop put on display was how much has changed—in technology and business models—since 2005 when we last comprehensively updated our equitymarket rules. The markets have moved to overwhelmingly trade electronically, with transaction volume in listed equities tripling in the last 17 years. [3]

The second was that, starting mid-year in 2020, equitymarkets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

rise in return on equity (ROE) to 14.2%; and gains in tier 1 equitycapital and assets of 5% and 4%, respectively. The group’s marketcapitalization in 2023 was at a 17-year high, valuing the enterprise at around the same level in dollar terms as Goldman Sachs. billion; a 2.3% increase in fee income.

The SEC’s remit is overseeing the capitalmarkets and our three-part mission: protecting investors, facilitating capital formation, and maintaining fair, orderly, and efficient markets. There’s no reason to treat the crypto market differently just because different technology is used.

equity interest in Marathon on an issued and outstanding basis; closing is expected to be completed on November 14, 2023 and is not contingent on closing of the Transaction. Through this Transaction, Valentine will be fully funded to production without additional debt, royalties, or shareholder equity.

According to NASDAQ’s Equity Regulatory Alert #2022-9, “when gatekeepers such as underwriters engage in misconduct or otherwise are derelict in their duties, confidence is diminished and investors suffer.” Treasury Department’s Financial Crimes Enforcement Network (“FinCEN”); and. broker-dealers to the U.S.

Cost of Capital & Failure Risk : For the cost of capital, I will assume that Airbnb’s cost of capital will be 6.50%, close to the cost of capital of hotel companies, to start the valuation, but over time, it will rise to 7.23%, reflecting an expected increase in the treasury bond rate from current levels to 2% in 2031.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of marketcapitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

Thus, as you peruse my historical data on implied equity risk premiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

Coming after a few days where the market seemed to have found its bearings (at least partially), it was clear from the initial reactions across the world that the breadth and the magnitude of the tariffs had caught most by surprise, and that a market markdown was coming.

The Hurdle Rate - Intuition and Uses You don't need to complete a corporate finance or valuation class to encounter hurdle rates in practice, usually taking the form of costs of equity and capital, but taking a finance class both deepens the acquaintance and ruins it.

Addressing climate change risk can improve risk-adjusted returns for investors holding a diversified portfolio of equity and other investments. Treasury Secretary Yellin has publicly signaled formal U.S. provides individuals with motive to become sensitive to the potential trade-off of ESG concerns for stock market returns.

It is for this reason that I chose to compute returns differently, using the following constructs: I included all publicly traded stocks in each market, or at least those with a marketcapitalization available for them. I converted all of the marketcapitalizations into US dollars , just to make them comparable.

Following two years of sticky inflation, exorbitant interest rates, and geopolitical tensions, worldwide equity issuance volume surged to $741 billion in 2024. Global inflation eased and major central banks began to cut interest rates: encouraging developments for equity issuers and investors. Thats up 20% from the previous year.

Thus, my estimates of equity risk premiums, updated every month, are not designed to make big statements about markets but more to get inputs I need to value companies. The first is i nterest rates, across the maturity spectrum , since their gyrations will play out across the market.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content