This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While there are many events during 2022, some political and some economic, that one can point to as the reason for poor stock returns, it is undeniable that inflation was the driving force behind the market correction. In this section, I will begin with a deconstruction of stock returns in 2022 and the year's place in stock market history.

While this may seem perverse, the first step in understanding and assessing where we are in markets now is to go back and examine where things stood then. trillion in market value in the first six months in the year , but the severity of last year's decline has still left them $14.4 US Equities in 2023: Into the Weeds!

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. Energy, one of the few survivors of the 2022 market sell-off, had a bad year, as did utilities and consumer staples. increase in marketcapitalization.

The first quarter of 2021 has been, for the most part, a good time for equitymarkets, but there have been surprises. The arrival of the COVID in February 2020, and the ensuing market meltdown, causing treasury rates to plummet across the spectrum, with three-month T.bill rates dropping from 1.5% Riskfree rate will rise.

Corporate Bonds: No Shortage of RiskCapital In my last post, I chronicled the movement in the equityriskpremium, i.e. the price of risk in the equitymarket, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

The graph below contains Tesla's stock price, adjusted for stock splits, going back to 2010, and ending in November 2021: While the graph illustrates the surge in the stock price, the table embedded in the graph conveys the rise more vividly, by listing Tesla's marketcapitalization in millions of dollars. for mature markets.

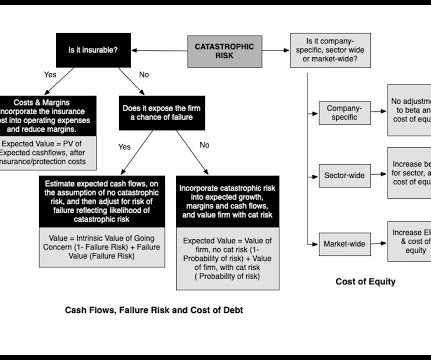

Minuses : As in the last approach, you still have to estimate a probability that a catastrophe will occur, and in addition, and there can be challenges in estimating the value of a business, if the company fails in the face of catastrophic risk. 4 & 5 Uninsurable Risk. Note that these higher discount rates apply in both scenarios.

In selecting the appropriate equityriskpremium, the court observed that whether to use supply-side or historical ERP should be determined on a case-by-case basis.

Finally, my starting cost of capital of 10.15% reflects the reality that the riskfree rate and equityriskpremiums have risen over 2022, and my ending number of 9% is an indication that I expect Tesla to become less risky over time. It was the reason that I argued at a $1.2

If equitymarkets surprised us with their resilience in 2020, not just weathering a pandemic for the ages, but prospering in its midst, US equitymarkets, in particular, managed to find light even in the darkest news stories, and continued their rise through 2021. The year that was.

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world.

The second was that, starting mid-year in 2020, equitymarkets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

The Market Reaction As the rhetoric of war has heated up in the last few months, markets were wary about the possibility of war, but as Russian troops have advanced into the Ukraine, that wariness has turned to sell off across markets. As Russian equities have imploded, the ripple effects again are being felt across the globe.

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

Regional Breakdown My data sample for 2022 includes every publicly traded firm that is traded anywhere in the world, with a marketcapitalization that exceeds zero. For debt markets, it takes the form of default spreads, and I report the latest estimates of these corporate bond spreads at this link.

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. Beta & Risk 1. Return on Equity 1. EquityRiskPremiums 2. Return on Equity 2.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of marketcapitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

Thus, as you peruse my historical data on implied equityriskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

Since the companies involved in building the AI infrastructure are the ones that are most tangibly (and immediately) benefiting from the AI boom, they are also the companies that have seen the biggest boost in market cap, as the AI story heated up.

Effective and well-designed laws governing investment and financial markets are the single most important foundation for financial markets to allocate capital efficiently while providing optimal reassurance to investors and lenders. In the United States, the cost of capital is lower than elsewhere. 3] [link]. [4]

It is for this reason that I chose to compute returns differently, using the following constructs: I included all publicly traded stocks in each market, or at least those with a marketcapitalization available for them. I converted all of the marketcapitalizations into US dollars , just to make them comparable.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content