This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

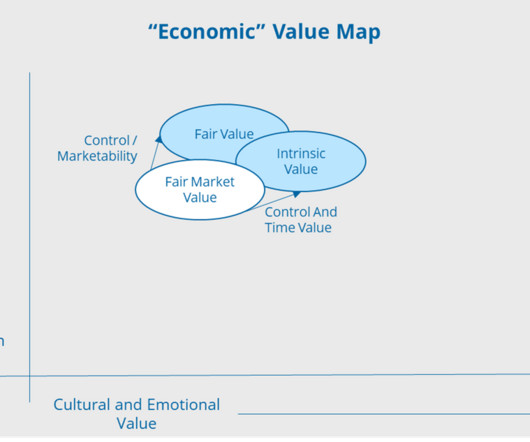

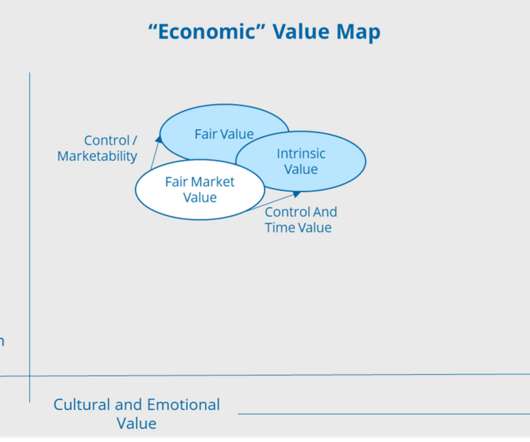

Transcending Value – Intrinsic and Fair Value Blog 1 of 4: This is the first in a series of blogs that attempts to explain and distinguish between various valuation concepts, such as price, fair market value, fair value, liquidation value, intrinsic value, financial value versus strategic value, monetary versus economic value, emotional and psychic value, among others.

What Transaction Options are Available to Business Owners? There are four transaction options available to business owners depending upon how ready they are financially and mentally to sell all or some of their business. Our readiness matrix helps owners determine which of four options may be best for them. Below we detail the rationale of each transaction type.

Business needs are changing, requiring companies to seek new strategic capabilities. Tax and accounting firms are uniquely positioned to be strategic advisors and service providers for their clients—but CPA firms must evolve, too. Modern businesses face unique challenges when trying to grow and stay competitive in a rapidly changing business environment.

The M&A ecosystem has continued to grow, evolve, and morph through the pandemic, economic cycles and the rise and fall of various industries. Building on buyside and sellside M&A conferences last year, this 201-level virtual conference focused on studying the most notable, recent M&A deals from the point of view of their respective GCs and CFOs.

Speaker: Susan Spencer, Principal of Spencer Communications

Intent signal data can go a long way toward shortening sales cycles and closing more deals. The challenge is deciding which is the best type of intent data to help your company meet its sales and marketing goals. In this webinar, Susan Spencer, fractional CMO and principal of Spencer Communications, will unpack the differences between contact-level and company-level intent signals.

Transcending Value – Intrinsic and Fair Value. Blog 1 of 4: . This is the first in a series of blogs that attempts to explain and distinguish between various valuation concepts, such as price, fair market value, fair value, liquidation value, intrinsic value, financial value versus strategic value, monetary versus economic value, emotional and psychic value, among others.

Report to Congress: Annual Report on Self-Insured Group Health Plans (Mar. 2021); Appendix A, Group Health Plans Report: Abstract of 2018 Form 5500 Annual Reports Reflecting Statistical Year Filings (Jan. 2021, v. 1.0); Appendix B, Self-Insured Health Benefit Plans 2021: Based on Filings Through 2018 (Dec. 22, 2020). Report. Appendix A. Appendix B. The DOL has made available its required annual report to Congress on self-insured health plans.

QUESTION: We will be using a third-party preparer and approved third-party software to submit our Form 5500 under the DOL’s EFAST-2 electronic filing system. As the plan administrator, do we need to obtain electronic credentials? ANSWER: Plan administrators must obtain electronic credentials for Form 5500 filing unless they decide to use the e-signature option (described below).

QUESTION: We will be using a third-party preparer and approved third-party software to submit our Form 5500 under the DOL’s EFAST-2 electronic filing system. As the plan administrator, do we need to obtain electronic credentials? ANSWER: Plan administrators must obtain electronic credentials for Form 5500 filing unless they decide to use the e-signature option (described below).

Bartnett v. Abbott Labs., 2021 WL 428820 (N.D. Ill. 2021). A federal trial court has dismissed certain of a 401(k) plan participant’s claims stemming from an identity thief’s unauthorized withdrawal of $245,000 from her plan account. The thief had accessed the participant’s account through a website maintained by the plan’s TPA and added deposit information for a new bank account.

Doe v. Catholic Relief Servs., 2021 WL 1164227 (D. Md. 2021). Available at [link]. Doe%20v%20CRS%2026%20Mar%2021.pdf. An employee sued his employer under Title VII and other federal and state laws after the employer dropped health plan coverage for the employee’s same-sex spouse. The employer—an organization affiliated with the Catholic Church—had assured the employee during the recruitment process that “all dependents” were covered under the plan, and the spouse was initially covered without c

In a new episode of the Tax & Tech Talks podcast series, experts from KPMG and Thomson Reuters discuss how companies are turning to automation and analytics software to stay ahead of changes buffeting indirect tax management. _. Listen to the entire episode. Listen and subscribe to Tax & Tech Talks podcast on Spotify , Libsynpro , and Apple Podcast apps. _.

International tax professionals can feel the winds shifting. Upcoming developments in international tax regulations — plus ongoing disruptions such as digital transformation, marketplace volatility, and remote work — are building the perfect storm. You need to prepare your tax team to keep your organization’s head above water. But that’s easier said than done if you’re relying on manual processes and legacy tools.

Speaker: Wayne Spivak - President and Chief Financial Officer of SBA * Consulting LTD, Industry Writer, and Public Speaker

The old adages that "cash is king" and "you can’t spend profits" still hold true today. But however well-known these sayings might be, it requires a change in mindset to properly implement a cash flow management system that predicts your business's runaway as accurately as possible. Key to this new mindset is understanding the difference between the Statement of Cash Flows, a historical look at the source and uses of cash, and the Cash Flow Statement, which uses transaction history and forward-l

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content