This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

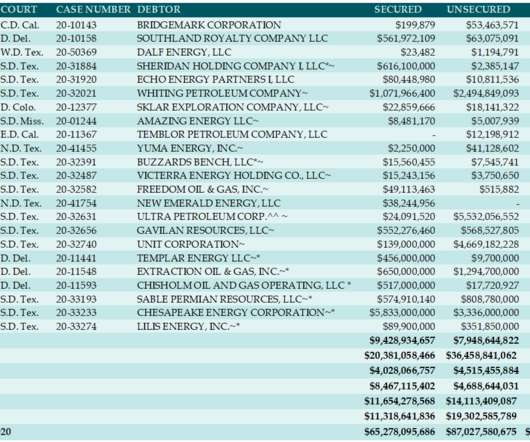

Click to Download: How to Avoid Chapter 22 in Restructuring Work for Energy Companies. Executive Summary. Issue. It takes time and money to go through a Chapter 11 restructuring, so going through it twice in a couple of years is unwise and inefficient. Recently, it has been an issue with companies operating in the energy complex. The challenges and complexities of energy markets make reorganization plans hard to properly formulate.

In Heinze v. Tesco Corp. , No. 19-20298, 2020 WL 4814094 (5th Cir. Aug. 19, 2020), the United States Court of Appeals for the Fifth Circuit affirmed the dismissal of a putative class action suit under Section 14(a) of the Securities Exchange Act of 1934 (“Exchange Act”), 15 U.S.C. § 78(b) alleging that defendant Tesco Corporation (“Tesco”), former members of Tesco’s board of directors and Nabors Industries, Ltd.

Speaker: Susan Spencer, Principal of Spencer Communications

Intent signal data can go a long way toward shortening sales cycles and closing more deals. The challenge is deciding which is the best type of intent data to help your company meet its sales and marketing goals. In this webinar, Susan Spencer, fractional CMO and principal of Spencer Communications, will unpack the differences between contact-level and company-level intent signals.

Definition of Inventory Conversion Period. The inventory conversion period is the timeframe that encompasses the process of obtaining the raw materials, manufacturing, to selling the product. It helps the firms estimate the timespan between the day raw materials are bought to the day the product is sold. The ideal inventory conversion ratio differs between industries.

Although its final episode aired more than a decade ago, there is still debate about the ending of HBO’s critically-acclaimed series, the Sopranos. In fact, as one critic notes, “the only objectively true statement that can be made about that ending is that it’s ambiguous.” [1] This ambiguity was embraced and lauded by some fans, while others felt cheated by not knowing, with certainty, the fate of one of television’s most well-known anti-heroes.

Click to Download: Oil and Natural Gas Prices-Are They Sustainable at These Levels? Executive Summary. Issue. There are three primary drivers that must be considered when looking at oil and gas prices. First, they are commodities, and move with the complex economics of global supply and demand. Second, they are very volatile. And third, they can be significantly influenced by global, geopolitical factors.

Click to Download: Oil and Natural Gas Prices-Are They Sustainable at These Levels? Executive Summary. Issue. There are three primary drivers that must be considered when looking at oil and gas prices. First, they are commodities, and move with the complex economics of global supply and demand. Second, they are very volatile. And third, they can be significantly influenced by global, geopolitical factors.

August 2020 Update With the advent of a “small global pandemic” – and the near universal move to “Work From Home” environments- the impact of Cyber Security threats has dramatically increased. Think “Cyber” was a risk to value previously? A trend we’ve seen is that not only has the pace of due diligence slowed as […].

Definition of the Receivable Collection Period. The receivable collection period is a period when a firm receives the amount owed by their customers (Account receivable). Firms need to know this because they have to make sure they have enough in hand for their current obligations. Because of the time value of money, firms aim to keep this period as short as possible without losing other benefits.

Speaker: Wayne Spivak - President and Chief Financial Officer of SBA * Consulting LTD, Industry Writer, and Public Speaker

The old adages that "cash is king" and "you can’t spend profits" still hold true today. But however well-known these sayings might be, it requires a change in mindset to properly implement a cash flow management system that predicts your business's runaway as accurately as possible. Key to this new mindset is understanding the difference between the Statement of Cash Flows, a historical look at the source and uses of cash, and the Cash Flow Statement, which uses transaction history and forward-l

Definition of the Payables Deferral Period. The period of time a firm takes to pay back their suppliers or creditors for their material purchases is known as payable deferral. Firms with a high payable deferral period have the ability to use the available cash for other short term investments and would benefit from the time value of money. For that reason, some suppliers give discounts to firms who pay faster.

Definition of Cash Conversion Cycle. The amount of time it takes a firm to convert its inventory into cash is known as the cash conversion cycle. In other words, it is the time taken for firms to convert their resources into cash. What is the Formula for the Cash Conversion Cycle? The cash conversion cycle (CCC) is calculated by adding days inventory outstanding and days sales outstanding and subtracting them by days payable outstanding. .

Definition of Gross Profit Margin. The gross profit margin compares the difference between the revenue and cost of goods sold, against revenue. It is represented in the form of a percentage. It is used to evaluate the company’s financial health. A higher markup price and lower cost of goods sold would increase the gross profit margin. What is the Formula for Gross Profit Margin?

Definition of EBIT Margin. EBIT margin stands for Earning Before Interest and Tax margin. This margin helps stakeholders understand the cost of running the firms as well as profitability. The higher the EBIT the better it is for the firm. What is the Formula for the EBIT Margin? EBIT margin is calculated by dividing EBIT by revenue. EBIT margin = EBIT / Revenue .

In this webinar, Joe Apfelbaum, CEO of Ajax Union and business strategist, will take you through the ABCs of intent data. You'll learn how to effectively use it to drive business results, with practical tips on how to leverage both company and contact intent data to maximize your marketing efforts. Whether you're a seasoned marketer or just getting started, this webinar is a must-attend for anyone looking to stay ahead in the ever-evolving world of digital marketing.

Definition of EBIT Return on Assets. EBIT return on asset measures the firm’s earnings before interest and tax with respect to the firm’s total asset. The main focus on this ratio is the income and the total asset. The reason EBIT is used and not net income is because EBIT focuses only on operating cash flows. . What is the Formula for EBIT Return on Assets?

Definition of Return on Invested Capital (ROIC). Return on invested capital is a method of calculation in which you measure the performance of a company in terms of profitability. The ROIC is expressed in terms of percentages. The ratio also helps you understand how efficient a company is at utilizing its capital to generate returns. The more income generated from the investment, the more efficient the company is.

Definition of Return on Equity (ROE). ROE is another method to measure the profitability of a company. The ROE divides the net income of a company with the shareholder’s equity. The ROE is expressed as a percentage. The shareholder’s equity is the company’s assets minus the company’s debt. Therefore the ROE is arguably the net return on assets.

Definition of Du Pont Analysis. The Du Pont analysis was created by the Du Pont corporation and is similar to the Return on Equity (ROE) but more accurate. The Du Pont analysis is known to decompose the drivers of ROE. The Du Pont analysis helps you understand the strengths and weaknesses of a company. What is the Formula for Du Pont Analysis? The formula for the Du Pont is the Net Profit Margin multiplied by the Asset Turnover and Equity Multiplier.

Definition of Net Profit Margin. The net profit margin is a financial ratio that tells you how much profit a company makes compared to its revenue in the form of a percentage. For example, if a company has a net profit margin of 20%, then they make 20 cents a dollar. The net profit margin can only be calculated when all the expenses have been deducted from the revenues.

Definition of Asset Turnover Ratio. The asset turnover ratio is used to measure the efficiency of a company. The higher the ratio, the more efficient the company is. . The asset turnover ratio looks at how efficiently a company uses its assets to produce sales. What is the Formula for Asset Turnover Ratio? The asset turnover ratio can be calculated by dividing the revenue by the average total assets.

Definition of Return on Assets. The return on assets focuses on how profitable a company is in relation to its total assets. The ratio is always presented in the form of a percentage. The higher the ratio, the more efficient and productive a company is. What is the Formula for Return on Assets? The return on assets can be calculated by dividing the net income by the average assets.

Definition of Assets to Equity Ratio. The assets to equity ratio allow you to understand to what extent a business is funded by equity or debt. The ratio measures the total assets in relation to total equity. In the case of the assets to equity, the higher the ratio, the more debt a company holds. What is the Formula for Assets to Equity Ratio? To find this ratio, you would have to take the total assets and divide it by the total equity.

Definition of Growth YoY. The YoY growth looks at a company’s performance/profit year after year or period after period. . The YoY compares the performance/profit and looks at how well the company is doing. The growth YoY is essential to investors as it allows them to see whether or not the business is worth investing in. What is the Formula for Growth YoY?

Definition of Liabilities to Assets Ratio. The liabilities to assets ratio is also known as the debt to asset ratio. The liabilities to assets ratio shows the percentage of assets that are being funded by debt. The higher the ratio is, the more financial risk there is in the company. What is the Formula for Liabilities to Assets Ratio? The liabilities to assets ratio can be found by adding up the short term and long term liabilities, dividing them by the total assets, and then multiplying the an

Definition of Risk Assessment. Risk assessment is an evaluation method used to understand an investor’s risk rating, which helps them come up with a suitable investment strategy to achieve their financial goals. What Impacts Risk Assessment? Financial risk assessment evaluates where a client stands in regards to taking risks. This can be understood through three approaches, including the client’s attitude towards risk, the tolerance for risk, and the capacity for risk.

Definition of Current Ratio. The current ratio or working capital ratio is a liquidity ratio that measures a firm’s ability to pay its short term liabilities. Short term liabilities are debts or any obligation that is due within one year. An ideal current ratio is between 1.2 and 2. . If the ratio is low, it means the firm does not have enough liquid assets to offset its short term liabilities.

Definition of Quick Ratio. The quick ratio is a liquidity ratio that measures a firm’s ability to pay its short term liabilities with its most liquid assets. Unlike the current ratio, the quick ratio is only calculated using the most liquid assets. The ideal current ratio is 1:1. The higher the ratio, the safer is the firm as that would mean they have excess cash.

Definition of the Agency Problem. Within corporate finance, the agency problem is considered as the conflict of interest between the company’s managers and its stockholders. This conflict occurs when personal interests are given a priority over the professional duties each party needs to fulfill. The core of the conflict is that managers want higher compensation, and shareholders want higher profits.

Definition of Compound Interest. Compound interest is the interest on the initial principal as well as the interest from the prior periods. . It is also referred to as interest on interest. With the same period of time, the sum of compound interest is always greater than simple interest because simple interest is the interest only on the initial value.

Definition of Optimal Capital Structure. The optimal capital structure of a firm is the right combination of equity and debt financing. It allows the firm to have a minimum cost of capital while having the maximum market value. The lesser the cost of capital, the more the market value of the company. Debt financing may have the lowest cost, but having too much of it would increase risks to the shareholders.

Definition of Capital Budgeting. When businesses want to buy new long term assets such as new machinery or start a new project, it is crucial to consider if it would be worth it or not. . Companies only have limited resources, so capital budgeting helps them prioritize the projects. Capital budgeting includes making decisions on implementing new projects, new plants, new equipment, and everything else that the company would spend on.

Definition of Stock Valuation. Stock valuation is the process of determining the current (or projected) worth of a stock at a given time period. There are 2 main ways to value stocks: absolute and relative valuation. . Absolute valuation is a method to calculate the present worth of businesses by forecasting their future income streams. Relative valuation is a method that compares a stock value to that of its competitors and peers within the same industry to assess the stock’s worth.

Definition of the Gordon Growth Model. The Gordon growth model, or GGM, is used to calculate the intrinsic value of a stock from future dividends. The model only works for companies that pay out dividends, which have a constant growth rate. What Impacts the Gordon Growth Model? The required rate of return . Dividend . Dividend growth rate . How to Calculate the Gordon Growth Model?

Definition of the Modigliani-Miller Theorem. The theory suggests that a company’s capital structure and the average cost of capital does not have an impact on its overall value. . The company’s value is impacted by its operating income or by the present value of the company’s future earnings. It doesn’t matter whether the company raises capital by borrowing money, issuing new shares, or by reinvesting profits in daily operations.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content