This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Privateequityfirms provide meaningful investment capital to growth-oriented businesses. Unlike venture capital firms, they do not invest primarily in start-ups. Businesses seeking expansion, change of investors, or even exit may benefit from privateequityfirms.

If you search for “how to start a privateequityfirm” online, you’ll find results that range from useless to tangentially useful to occasional nuggets of real wisdom. Starting a privateequityfirm is a bad decision for ~95% of people who work in the finance industry. How Does It Work?

Privateequity value creation came on my radar a few years ago when I noticed something: Even though traditional PE deal roles were not doing well, “operational” or “value creation” teams still seemed to be recruiting. What Does the PrivateEquity Value Creation Team Do in Real Life?

If you ever tire of the hype around tech, industrials privateequity might be an ideal hiding spot. Morgan’s acquisition of Carnegie Steel in 1901 – was an industrials privateequity deal. Table Of Contents Industrials PrivateEquity Defined What Has Drawn PrivateEquityFirms to Industrials Companies?

This is music to the ears of strategic acquirers and privateequityfirms. Strong EBITDA (earnings before interest, taxes, depreciation, and amortization) margins are always going to be a green flag for buyers. Privateequity buyers who are after targets with stable cash flows and growth potential.

But this started changing in the 2010s and early 2020s as team values skyrocketed and billionaires, sovereign wealth funds , and sports privateequityfirms all jumped into the sector. Regulations – Does the league allow privateequity or other financial sponsor ownership? What is Sports Investment Banking?

At the lower end of the market, individuals are still leaving their jobs to buy businesses and at the higher end, institutional investors and privateequityfirms have more capital available than ever before. multiple of SDE or EBITDA. Aggregators vs. PrivateEquityFirms.

The buyer (the “sponsor”) raises debt and equity to acquire the target. It borrows the majority of the purchase price and contributes proportionately small equity investment. The LBO ratios can go to 90% of debt and 10% of equity. A privateequityfirm aims a target return of around 20 – 25% (WallStreetMojo, 2018).

Leveraged Buyouts (LBOs) are powerful tools in the financial world, used by privateequityfirms and savvy investors to maximize returns. They involve acquiring a company using a mix of debt and equity, where the acquired company’s cash flows are used to service the debt. Ready to master the art of LBOs?

But over the years, they morphed into a well-known topic and then a commonly derided topic – as many people argue that search fund experience is worthless, while others claim it’s “just as good” as working in banking or privateequity. As usual, the truth is somewhere in between. appeared first on Mergers & Inquisitions.

Project Finance Definition: “Project Finance” refers to acquisitions, debt/equity financings, and new developments of capital-intensive infrastructure assets that provide essential utilities and services. However, many people also use the term more broadly to refer to equity, debt, and advisory for infrastructure assets.

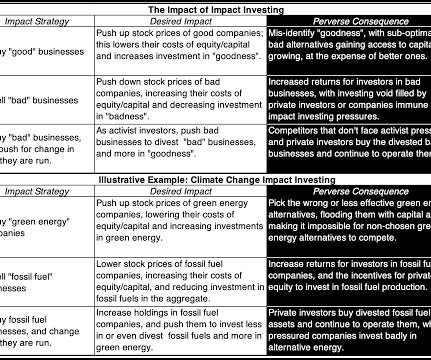

The effect of impact investing in the inclusionary and exclusionary paths is through the stock price , with the buying (selling) in inclusionary (exclusionary) investing pushing stock prices up (down), which, in turn, decreases (increases) the costs of equity and capital at these firms. in the 1998-2010 time period to 5.95

"Boundary Devices was at an inflection point in 2016 and we decided to seek an equity partner to help us reach our next level of potential. " Since Montage Partners' investment in 2016, revenue and EBITDA at Boundary Devices have each grown approximately fourfold, driven entirely by organic growth initiatives.

REAG specializes in the lower middle market , focusing on companies with profitability and growth potential, with an emphasis on serving: Regional, national and global markets $2M+ EBITDA Scalable businesses We provide tailored solutions for companies across diverse geographic scales, matching each business’s unique scope and ambitions.

MCM Capital Partners (MCM) is a lower-middle market privateequity fund. Founded in 1992, MCM is a Cleveland-based privateequityfirm focused on acquiring niche manufacturers, value-added distributors and service companies generating up to $75 million in annual revenues and having enterprise values of less than $50 million.

GF: Are you seeing more mergers and acquisitions involving self-funded public companies and privateequityfirms? Eventually, privateequity will lead coming out of this. We’re in a relatively stable environment, and it provides an opportunity for privateequityfirms to step back into the deal arena.

These ratios, like the EBITDA multiple, compare a company’s financial performance (EBITDA, revenue, etc.) These multiples are applied to target company’s latest financials such as revenue, earnings and book value of equity to arrive at an estimate of enterprise value or equity value. to its market value.

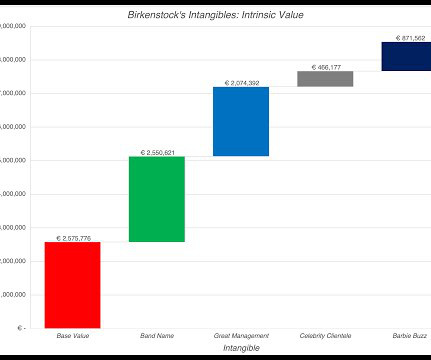

In this post, I will look at another initial public offering, Birkenstock, that is likely to get more attention in the next few weeks, given that it is targeting to go public at a pricing of about €8 billion, for its equity, in a few weeks. So, how far has accounting come in bringing intangible assets on to balance sheets?

Balance Sheet A Balance Sheet is an accounting record for a company that lists a company’s assets, liabilities, and shareholders’ equity. In particular, a Buy-Sell Agreement will typically provide for what happens in the event that one of the shareholders leaves the business and he or she needs to dispose of an equity stake in the business.

At the lower end of the market, individuals are still leaving their jobs to buy businesses and, at the higher end, institutional investors and privateequityfirms have more capital available than ever before. When your SaaS is effectively implemented and protected, your risk for disruption becomes much more minimal. and Team.

For example, corporate investors or privateequityfirms can be interested in a more mature company with slower growth, if it corresponds to less risk, compared to venture capital or angel investors who are generally looking for younger startups with the potential to become billion dollar companies.

Financial buyers are typically privateequityfirms or family offices. Financial buyers often prioritize increasing EBITDA and market share over a shorter investment period (usually three to seven years). The Financial Buyer. Many sellers confuse financial buyers with strategic buyers , but the two are very different. .

While some corporate buyers and privateequityfirms see the advantages of purchasing smaller businesses, companies with less than $5 million in sales and an EBITDA of less than $1 million may be more dependent on continuing outside financing and lack the critical mass for both buying and selling power. Grow in size.

Such reports are increasingly common in larger transactions, especially where the buyer is a privateequityfirm. “A It shows a buyer the business’s true profitability by adjusting EBITDA to reflect any non-recurring revenues and expenses.

Ever since the 2008 financial crisis, there has been massive hype about both privateequity and technology. Over the past few decades, technology privateequity has gone from “barely existing” to representing the largest single sector in PE by both deal value and deal count. Why Did PE Firms Start Buying Tech Companies?

According to some, you do almost no modeling or technical work in this group, and it’s one of the easier jobs in IB, similar equity or debt capital markets. But if you read other accounts, FSG runs models, Analysts get hands-on technical work, and the hours could be longer and more stressful because your clients are privateequityfirms.

When you hear the words “healthcare privateequity,” two thoughts probably come to mind: Wait a minute, isn’t healthcare a risky/growth-oriented sector? Why do PE firms operate there? In most of the world, healthcare is either government-run or a mixed public/private sector.

Power and Utilities Investment Banking Definition: In power/utilities IB, bankers advise companies that produce, transmit, and distribute electricity, natural gas, and water on raising debt and equity and completing mergers and acquisitions. For example, let’s say the company’s Rate Base is $1,000, as in the Lazard example above.

Renewable Energy Investment Banking Definition: In renewable energy investment banking, bankers advise companies in the solar, wind, biofuel, storage, battery, smart grid, electric vehicle, hydrogen, hydroelectric, and carbon capture verticals on equity and debt issuances, asset deals, and mergers and acquisitions.

Oil & Gas Investment Banking Definition: In oil & gas investment banking, professionals advise companies that search for, produce, store, transport, refine, and market energy on raising debt and equity and completing mergers and acquisitions. Midstream: 85 (mix of asset deals, M&A, debt, and even some privateequity activity).

This shift has created a more balanced market, especially for firms with less than $2 million in EBITDA, where multiples are under more pressure. Despite these challenges, top-quartile firms continue to command premiums. In some cases, smaller firms are coming together to bolster their EBITDA and achieve higher multiples.

This shift has created a more balanced market, especially for firms with less than $2 million in EBITDA, where multiples are under more pressure. Despite these challenges, top-quartile firms continue to command premiums. In some cases, smaller firms are coming together to bolster their EBITDA and achieve higher multiples.

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. Most of the differences emerge on the mining side.

In the second quarter, growth in Ebitda [earnings before interest, taxes, depreciation and amortization] outpaced interest expense growth for high-yield corporates. GF: How does it look for privateequityfirms? That, combined with lower rates, makes it much more economical for privateequity sponsorship.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content