This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

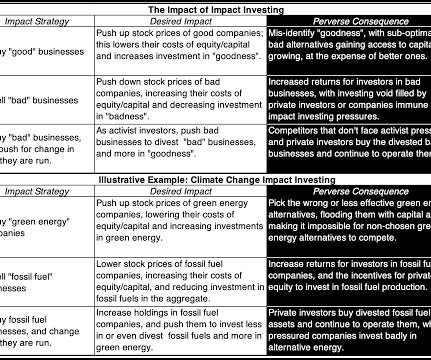

On the alternative energy front, as money has flowed into these companies, there has been a surge in enterprisevalue (equity and netdebt) and market capitalization (equity value); I report both because impact investing can also take the form of green bonds, or debt, at these companies.

iii) Income Multiplier Method The income multiplier method uses a multiple of a company’s earnings or cash flows to determine its value. iv) Dividend Discount Model (DDM) Focuses specifically on valuing companies that pay dividends to their shareholders. It represents the total market value of the company’s equity.

Billion and Adjusted EBITDA of $1.4 billion and adjusted EBITDA of $1.4 billion and adjusted EBITDA of $1.4 The transaction values McGrath at an enterprisevalue of $3.8 billion, including approximately $800 million of netdebt, and the per-share consideration represents a premium of 10.1%

billion on an enterprisevalue basis. Included in the Q3 2021 net sales are revenues of approximately $41.3 Net Income for the third quarter of 2022 was $33.6 Non-GAAP adjusted EBITDA* was $92.1 The Company ended the quarter with total gross debt of $1.06 million, or 7.2% of revenues. million, or 19.8%

Cash generating capacity : Debt payments are serviced with operating cash flows, and the more operating cash flows that firms generate, as a percent of their market value, the more that they can afford to borrow. The answer lies in looking at a company's earnings and cash flow capacity, relative to its debt obligations.

d/b/a H&E Rentals (NASDAQ: HEES ) ("H&E") today announced their entry into a definitive agreement under which United Rentals will acquire H&E for $92 per share in cash, reflecting a total enterprisevalue of approximately $4.8 billion of netdebt. billion, including approximately $1.4

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content