This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The current price of $133 represents a marketcapitalization of $145 billion. At the current level Salesforce has a P/E ratio of 100x and an EV/EBITDA ratio of 47x for 2022. This was mainly driven by operating expenses growth exceeding sales growth and thus putting strain on EBITDA margin.

The current price of $133 represents a marketcapitalization of $145 billion. At the current level Salesforce has a P/E ratio of 100x and an EV/EBITDA ratio of 47x for 2022. This was mainly driven by operating expenses growth exceeding sales growth and thus putting strain on EBITDA margin.

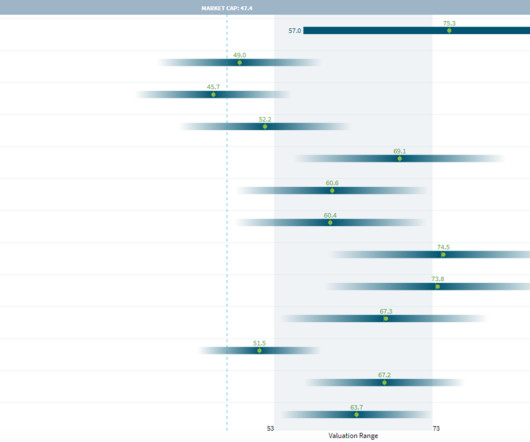

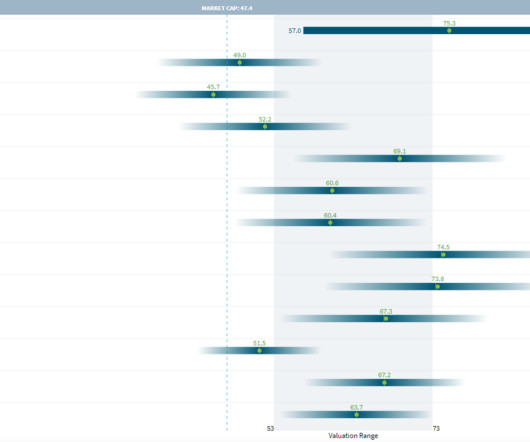

billion with EBIT margin increasing to 16.6% Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. from 15.1%

billion with EBIT margin increasing to 16.6% Currently the company is trading at CHF 30 per share with a marketcapitalization of CHF 56.1 The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. from 15.1%

billion, driven by lower interest expense and lower non-cash impairment losses, offset by lower Adjusted EBITDA, an accrual related to the securities class action lawsuit, and higher supply chain and commodity costs. Adjusted EBITDA decreased 5.8% billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E.

billion, driven by lower interest expense and lower non-cash impairment losses, offset by lower Adjusted EBITDA, an accrual related to the securities class action lawsuit, and higher supply chain and commodity costs. Adjusted EBITDA decreased 5.8% billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E.

This led to a market cap of €78 billion after the IPO, which is higher than the current marketcapitalization of its parent company Volkswagen AG (€72 billion). . In the fo rmer, we compared Porsche with peers such as BMW, Mercedes-Benz, Ferrari and Ford using thethe EV/EBITDA and the EV/EBIT multiples.

The company also was able to increase its EBITDA by 6.5% with an overall EBITDA margin of 35.2%. The Trading Comparables analysis resulted in a valuation range of €98 to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. billion which is an increase of 5.7% compared to last year’s Q3.

The company also was able to increase its EBITDA by 6.5% with an overall EBITDA margin of 35.2%. The Trading Comparables analysis resulted in a valuation range of €98 to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. billion which is an increase of 5.7% compared to last year’s Q3.

It sustains its FY 2023 production and capital spending outlook. Share Price Performance The company has a marketcapitalization of more than $32 billion, however, its share price is still down roughly 30% from highs set last year. billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E.

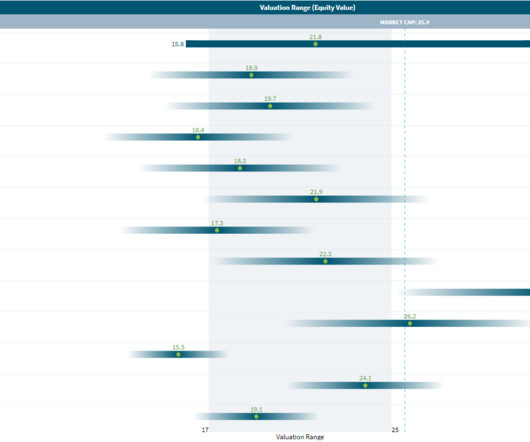

2022 saw a robust cash and capital structure with a staggering USD 967 million adjusted EBITDA in Q4, up by 14% from the previous year. billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. In comparison to Oneok marketcapitalization of USD 25.9 billion to USD 32.3

With a marketcapitalization of €395 billion, it is the most valuable company in Europe. The Trading Comparables analysis resulted in a valuation range of €305 billion to €492 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E.

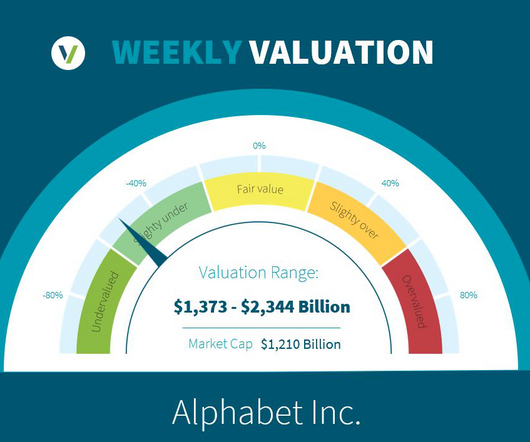

The company is one of the world’s largest companies with a marketcapitalization of $1.34 The Trading Comparables analysis resulted in a valuation range of $1,517 billion to $2,344 billion by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E.

Emphasizing the company’s robust market performance, Nvidia’s marketcapitalization has hit the USD 1 trillion milestone, joining the elite league of tech behemoths such as Apple and Amazon. Reflecting strong Q1 2023 performance and favorable market trends, NVIDIA’s current share price stands at USD 430.39.

We used the observed trading multiples EV/EBITDA, EV/EBIT and P/E of a group of similar listed peers for our Trading Comparables analysis, arriving at a valuation range of $193 billion to $237 billion. Alibaba’s current marketcapitalization of $167 billion suggests that the company is undervalued.

billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT, P/E and P/B. In comparison to Cameco marketcapitalization of CAD 18.3 The Trading Comparables analysis resulted in a valuation range of CAD 6.4 billion to CAD 28.1 and Peninsula Energy Limited. billion to CAD 19 billion.

The Trading Comparables analysis resulted in a valuation range of $257 billion to $296 billion by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Visa’s marketcapitalization of $471 billion we suggest that the company is significantly overvalued.

Market-based approaches gauge a company’s value by analyzing comparable market transactions and valuations. While many people are familiar with marketcapitalization as a method for understanding the general worth of publicly traded companies based on the current market sentiment (itself based on company performance, etc.),

billion to USD 108 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. In comparison to PMI marketcapitalization of USD 140 billion we suggest that the company is fairly valued. The Trading Comparables analysis resulted in a valuation range of USD 57.2

The Trading Comparables analysis resulted in a valuation range of $83 billion to $118 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Starbucks’ marketcapitalization of $120 billion we suggest that the company is slightly overvalued. . billion to $118 billion.

The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Home Depot’s marketcapitalization of $319 billion we suggest that the company is overvalued.

The Trading Comparables analysis resulted in a valuation range of $83 billion to $118 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Starbucks’ marketcapitalization of $120 billion we suggest that the company is slightly overvalued. . billion to $118 billion.

The Trading Comparables analysis resulted in a valuation range of $202 billion to $231 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Home Depot’s marketcapitalization of $319 billion we suggest that the company is overvalued.

The Trading Comparables analysis resulted in a valuation range of USD 503 billion to USD 812 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. In comparison to Meta’s marketcapitalization of USD 730 billion we suggest that the company is fairly valued. Microsoft Corporation.

The Trading Comparables analysis resulted in a valuation range of USD 106 billion to USD 235 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. In comparison to IBM marketcapitalization of USD 114 billion we suggest that the company is undervalued. and Alphabet Inc.

The Trading Comparables analysis resulted in a valuation range of GBP 98 (USD 199) billion to GBP 137 (USD 166) billion by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. In comparison to BP’s marketcapitalization of GBP 101 (USD 122) billion we suggest that the company is slightly undervalued.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Tencent’s marketcapitalization of HKD 3,070 (USD 386.6) The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

We came up with this valuation range by using the observed trading multiples EV/EBITDA, EV/EBIT and P/E of peers such as Nike and Puma. . By combining these two approaches we arrive at a fairly wide valuation range of €15.6 billion to €44.9

Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. At TotalEnergies’ current marketcapitalization of €148 billion, our analysis suggests that the company is undervalued.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Tencent’s marketcapitalization of HKD 3,070 (USD 386.6) The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

billion to HKD 3,905 (USD 501) billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Tencent’s marketcapitalization of HKD 3,070 (USD 386.6) The Trading Comparables analysis resulted in a valuation range of HKD 1,752 (USD 221.5) billion to HKD 3,905 (USD 501) billion.

Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. At TotalEnergies’ current marketcapitalization of €148 billion, our analysis suggests that the company is undervalued.

We came up with this valuation range by using the observed trading multiples EV/EBITDA, EV/EBIT and P/E of peers such as Nike and Puma. . By combining these two approaches we arrive at a fairly wide valuation range of €15.6 billion to €44.9

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. EBIT & EBITDA multiple s 5. Revenue Multiples 4. Long term Reinvestment (Cap Ex & Acquisitons) 4.

Comparable companies are companies that operate in the same industry or market and have similar financial metrics, such as revenue, earnings, and marketcapitalization. Selecting Peer Companies Based on Size Size and marketcapitalization are important criteria in selecting comparable companies.

Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses. Data universe : In my sample, I include all publicly traded firms with marketcapitalizations that exceed zero, traded anywhere in the world.

billion to USD 150 billion, by utilizing observed metrics such as EV/EBITDA, EV/EBIT, and P/E ratios. For a robust comparative landscape, we enlisted similar market players like Alphabet Inc.(Youtube), Additionally, the Trading Comparables analysis generated a valuation range of USD 85.4 Youtube), Apple Inc. Amazon Prime Video).

Visa is currently the 11th most valuable company globally in terms of marketcapitalization. Additionally, the Trading Comparables analysis generated a v aluation range of USD 220 billion to USD 290 billion, by utilizing observed metrics such as EV/EBITDA, EV/EBIT, and P/E ratios.

The Trading Comparables analysis resulted in a valuation range of $121 billion to $150 billion by applying the observed trading multiples EV/EBITDA and EV/EBIT. In comparison to Boeing’s marketcapitalization of $127 billion we suggest that the company is fairly valued. billion to $150 billion.

Recent Financial Performance In Q1 2023, Marriott exceeded market expectations with gross lodging fees reaching USD 1.13 billion and an EBITDA of USD 1.09 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. In comparison to Marriott marketcapitalization of USD 52.9

In the last two decades, I have seen free cash flow measures stretched to cover adjusted EBITDA, where stock-based compensation is added back to EBITDA, and with WeWork, to community-adjusted EBITDA, where almost all expenses get added back to get to the adjusted value.

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

The Trading Comparables analysis resulted in a valuation range of $174 billion to $391 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Oracle’s marketcapitalization of $219 billion we suggest that the company is slightly undervalued. .

The Trading Comparables analysis resulted in a valuation range of $174 billion to $391 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. In comparison to Oracle’s marketcapitalization of $219 billion we suggest that the company is slightly undervalued. .

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content