This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

The premium that investors demand over and above the riskfreerate is the equity riskpremium , and practitioners in finance have wrestled with how best to estimate that number, since it is not easily observable (unlike the expected return on a bond which manifests as a current market interest rate).

That said, the three primary inflation indices in the US, the CPI, the PPI and the GDP deflator all told the same story in 2021: Download historical inflation numbers The inflation rate during the course of the year reached levels not seen in close to 40 years, with every price index registering a surge.

If, on the other hand, investors are risk neutral, the price of risk will be zero, and investors will buy risky business, stocks and other investments, and settle for the riskfreerate as the expected return. Estimation Approaches Why is it so difficult to estimate an equity riskpremium?

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. At the start of 2022, the ten sectors (US) with the highest and lowest relative risk (unlettered betas), are shown below.

Price of Risk The drop in stock and bond prices in the third quarter of 2023 can partly be attributed to rising interest rates, but how much of that drop is due to the price of risk changing? below the actual index level of 4288, making it close to fairly valued.

The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors. Download data US Treasury rates rose across all maturities, but more so at the short end of the term structure (3 months, 1 year and 2 year) than at the long end (10 year or 30 year).

Note that in all three cases, it is not the Fed that is driving rates, but what is happening to inflation. Since 2020, though, inflation has become a key story line in almost every post that I write about the overall market, and I have had multiple posts just on the topic.

In this section, I will begin measures of country default risk, including sovereign ratings and CDS spreads, before moving to more expansive measures of country risk before concluding with measures of equity riskpremiums for countries, a pre-requisite for estimating the values of companies with operations in those countries.

The answer, to me, seems to be obviously yes, though there are still some who argue otherwise, usually with the argument that country risk can be diversified away. In that post, I computed the equity riskpremium for the S&P 500 at the start of 2021 to be 4.72%, using a forward-looking, dynamic measure. as mature markets.

A Ride to Nowhere - US Treasury Rates in 2023 It was undoubtedly a relief for bond market investors to see US treasury markets settle down in 2023, though there were bouts of volatility, during the course of the year.

As I noted in my last post , rising riskfreerates and equity riskpremiums have pushed up the costs of equity for all companies, and Tesla is not only no exception but is perhaps even more exposed as an above-average risk company.

Risk : When I valued Tesla last in early 2020, I used a cost of capital of 7%, reflecting a riskfreerate of 1.75% and an equity riskpremium of 5.2% for mature markets.

the returns you can make on investments of equivalent risk, and that game became a lot more difficult to win in 2022. To explore differences in profit margins across industry groups, I broke stocks down into 94 industry groups, and sorted industries, based upon operating margin, from highest to lowest.

To fill in the missing pieces, I redid the valuation picture, adding the revenue growth rate, by year: Download spreadsheet As you look at the sheet, it is worth emphasizing a few estimation details that you may have missed in my original post: First, the revenue growth rate , at least for me, is a means to an end, not an end in itself.

Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. Investors need to reassess their expected returns to reflect riskfreerates & current ERP & default spreads.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low riskfreerates (with the treasury bond rate at 0.93% at the start of 2021).

Risk Differences across Countries In this final section, I will look risk differences across countries, both in terms of why risk varies across, as well as how these variations play out as equity riskpremiums.

Equity Risk across Countries Default risk measures how much risk investors are exposed to, when investing in bonds issued by a government, but when you own a business, or the equity in that business, your risk exposure is not just magnified, but also broader.

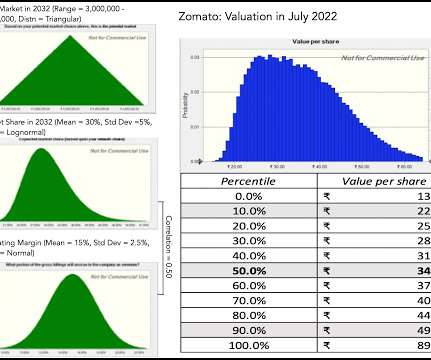

The effects of inflation show up first as higher riskfreerates , across currencies, and next in higher riskpremiums, with both equity riskpremiums and default spreads rising. As a company with the bulk of its business in India, Zomato again is more exposed to these developments.

RiskPremiums : You cannot make informed financial decisions, without having measures of the price of risk in markets, and I report my estimates for these values for both debt and equity markets. I extend my equity riskpremium approach to cover other countries, using sovereign default spreads as my starting point, at this link.

for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic riskfreerate of 8.7%. The Stocks Story As treasury rates have risen in 2021, equity markets have been surprisingly resilient, with stocks up during the first three months.

Download historical data Across the 97 years that I have estimated annual returns, stocks have had their ups and downs, delivering positive returns in 71 years and negative returns in the other 26 years. Historical Context To assess stock returns in 2024, it makes sense to step back and put the year's performance into historical perspective.

At the start of 2024 , the ten-year treasury rate stood at 3.88%, unchanged from its level a year prior, but the 3-month treasury bill rate had climbed to 5.40%. That should come as little surprise, since the forces that cause investors to spike up premiums (fear) or bid them down (hope and greed) cut across both markets.

I am no expert on exchange rates, but learning to deal with different currencies in valuation is a prerequisite to valuing companies. The logical step in looking across countries is measuring risk in countries, and bringing that risk into your analysis, by incorporating that risk by demanding higher expected returns in riskier countries.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content