This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This eleventh post in the Deja Vu series involving restricted stock studies addresses an issue that is rarely mentioned in the context of the studies – of the impact of dividends on restricted stock discounts (RSDs). This 2008 version had information on 477 restricted stock transactions, up from 430 transactions in the 2004 version.

Historical Data: 1930-2019 To see how this framework works in practice, let's start by looking at the performance of US stocks, across the decades, and look at the returns on stocks, broadly categorized based on marketcapitalization and price to book ratios.

I will follow up by looking at the mechanics that connect stock prices to inflation, and examine why the damage from higher inflation can vary across companies and sectors. The first is the dividends you receive, while you hold stocks, a cash flow stream that provides a measure of stability to investors who seek it. Stocks: The What?

While stocks had their ups and downs during the year, they ended the year strong, and recouped, at least in the aggregate, most of the losses from 2022. Stocks ended the year well, with November and December both delivering strong up movements, and while this left investors feeling good about the year, it was a rocky year.

I am just not good at it, and the first six months of 2023 illustrate why market timing is often the impossible dream, something that every investor aspires to be successful at, but very few succeed on a consistent basis. Markets, as is their wont, live to surprise, and the first six months of 2023 has wrong-footed the experts (again).

In this post, I will begin by looking at how to value banks and follow up with an examination of investor views of banking have changed, by looking at pricing, before examining divergences in how banks are priced in the market today. Note the differences between the bank FCFE and bank dividend discount models.

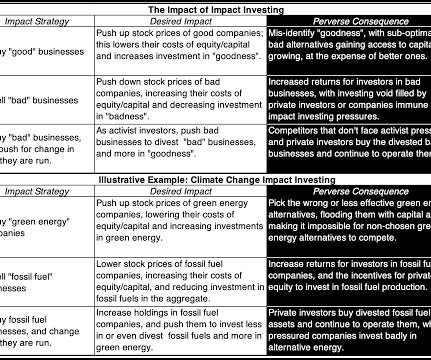

The effect of impact investing in the inclusionary and exclusionary paths is through the stock price , with the buying (selling) in inclusionary (exclusionary) investing pushing stock prices up (down), which, in turn, decreases (increases) the costs of equity and capital at these firms. in the 1998-2010 time period to 5.95

That drop of more than $200 billion in marketcapitalization in response to what looked like good news, at least on the surface, puzzled market observers, though, as is their wont, they had found a reason by day end. on June 18, 2024, and a low of $92.06, on August 5, before ending at $125.61

Second, they have all been in the news in the last few weeks, with Starbucks getting a new CEO, Walgreens announcing that they will be shutting down hundreds of their stores and Intel coming up in the Nvidia conversation, often as a contrast.

Investors, used to a decade of better-than-expected earnings and rising stock prices at these companies, have been blindsided by unexpected bad news in earnings reports, and have knocked down the marketcapitalization of these companies by hundreds of billions of dollars in the last few weeks.

The automobile business has been in trouble for quite a while, struggling with anemic revenue growth in the aggregate, and abysmal profit margins, with even the very best in the group struggling to earn returns that match, let alone beat, their costs of capital. In sum, the company's market cap has risen from $2.8

In this post, I will look at corporate profitability, in all its different dimensions, and how companies across the globe, and across industries, measured up in the most recent years. Not surprisingly, then, the net effect of growth will depend on how much is reinvested back, relative to what the company can harvest as future growth.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

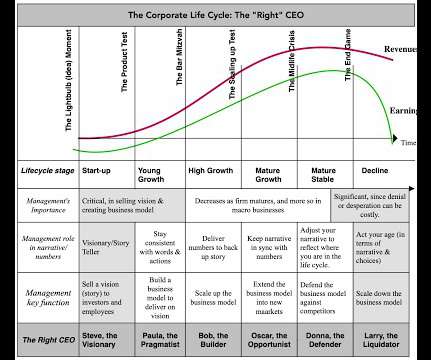

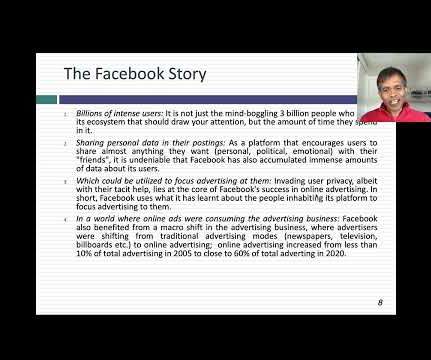

In my first two posts on Facebook, I noted that its most recent earnings report, and the market reaction to it, offers an opportunity for us to talk about bigger issues. Why stories matter in a numbers world If you are a numbers valuation, you start with some advantages.

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

This was primarily based on revenue growth, which registered a heady 30% rise, allowing the bank to distribute its highest full-year dividend since 2008. The NIM at Japan’s three largest banks hit 56 bps, the highest since the BOJ started its negative interest rate regime in 2012. billion after-tax profit versus $8.3 billion in 2022.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

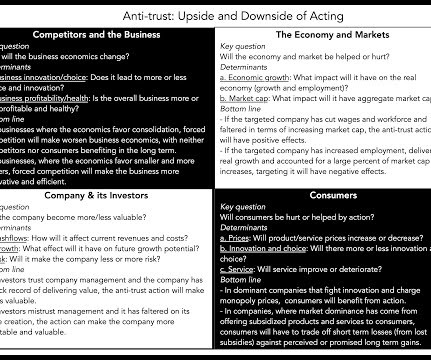

In a court filing on October 9, 2024, the US Department of Justice (DOJ) let it be known that it was considering a break-up of Alphabet, with the addendum that it would also be pushing for the company to share the data it collects across its multiple platforms with competitors. In oil, it was John D.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year.

The Biden Administration's $ 2 trillion infrastructure plan, announced with fanfare a few weeks ago, has opened up a debate about not only what comprises infrastructure, but also about how to pay for it. Not surprisingly. It thus weights bigger companies more than smaller companies. billion in accrual taxes and $15.98

Note that we start with net income , earnings that is already after interest expenses and taxes, and that we consider reinvestment in both short term assets (change in non-cash working capital) as well in long term assets (as the difference between capital expenditures and depreciation).

The DLVR occurs because investors are willing to pay a lower price for a stock with limited decision-making power, even if it has the same potential for dividends and capital appreciation as a stock with full voting rights. Schedule a demo now and start exploring the power of business valuation software for free !

The Lead In As noted in the introductory paragraph, I start from a position of ignorance about the Adani Group, and it thus made sense to fill in that gap. First, they are infrastructure businesses , requiring large up-front investments and having long gestation periods, with regulatory and government oversight.

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. In the table below, we compare the changes in regional marketcapitalizations (in $ millions) over time.

In my last post , I noted that the US has extended its dominance of global equities in recent years, increasing its share of marketcapitalization from 42% in at the start of 2023 to 44% at the start of 2024 to 49% at the start of 2025.

A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses. Much of the confusion in applying cost of capital comes from not recognizing that it morphs, depending on where it is being used.

That was the thought that came to mind, as I was writing about the US government's plans to break up big tech, and chronicling how much the big tech companies have struggled, trying to enter new businesses, notwithstanding the capital and brainpower that they have at their disposal.

In addition, Rule 14a-8 only allows for a supporting statement of up to 500 words. go back) 4 For example, the shareholder’s pre-approval was required before the Board issued stock, declared a dividend, incurred debt, appointed or removed specified officers, entered into a merger, or approved the annual budget. (go go back)

I will start with a couple of confessions. When I started my teaching journey at the University of California at Berkeley in 1984, business education was dollar-centric, with business schools around the world using textbooks and cases written with US data and starring US companies.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content