This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporate finance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

In this post, I will begin by chronicling the damage done to equities during 2022, before putting the year in historical context, and then examine how developments during the year have affected expectations for the future. Actual Returns Your returns on equities come in one of two forms. at the start of that year.

If you have been reading my posts, you know that I have an obsession with equity risk premiums, which I believe lie at the center of almost every substantive debate in markets and investing. How, you may ask, can equity risk premiums be that divergent, and does that imply that anything goes?

Corporate finance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. Can we speed up the data consolidation processes? Your total compensation in U.S.-based

When I started offering financial modeling training , I never expected to get questions about a methodology like the Dividend Discount Model (DDM). Otherwise, the written version follows: Why Use a Dividend Discount Model? If you sum up these numbers, you can see whether the company is valued appropriately.

In a post at the start of 2021 , I argued that while stocks entered the year at elevated levels, especially on historic metrics (such as PE ratios), they were priced to deliver reasonable returns, relative to very low risk free rates (with the treasury bond rate at 0.93% at the start of 2021). The year that was.

Just look at the handy chart the Financial Times put together to see the horrifically bad numbers: In January 2022, everything seemed quite frothy, with mega-deals happening left and right and crypto and equity prices still at high levels. Treasuries: 19% [Up 19%]. Real Estate (Equity Funds + Owned Properties): 15% [Up 5%].

In my last post , I discussed how inflation's return has changed the calculus for investors, looking at how inflation affects returns on different asset classes, and tracing out the consequences for equity values, in the aggregate.

This eleventh post in the Deja Vu series involving restricted stock studies addresses an issue that is rarely mentioned in the context of the studies – of the impact of dividends on restricted stock discounts (RSDs). This 2008 version had information on 477 restricted stock transactions, up from 430 transactions in the 2004 version.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Return on Equity 1. Dividends and Potential Dividends (FCFE) 1. Beta & Risk 1.

If you search for “how to start a private equity firm” online, you’ll find results that range from useless to tangentially useful to occasional nuggets of real wisdom. That said, much of it is better than the junk found on generic websites about how to start a hedge fund. How Does It Work?

Heading into 2023, US equities looked like they were heading into a sea of troubles, with inflation out of control and a recession on the horizon. While stocks had their ups and downs during the year, they ended the year strong, and recouped, at least in the aggregate, most of the losses from 2022. increase in market capitalization.

In my early 2021 posts on inflation, I argued that while the higher inflation that we were just starting to see could be explained by COVID and supply chain issues, prudence on the part of policy makers required that it be taken as a long term threat and dealt with quickly. in the NY Fed survey. in the NY Fed survey.

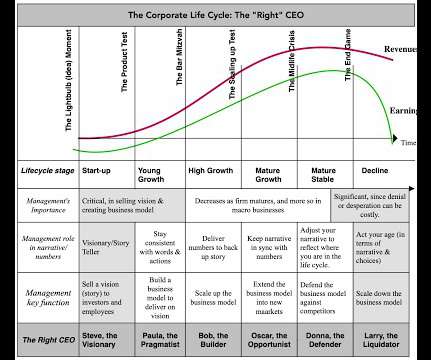

My version of the corporate life cycle is built around six stages with the first stage being an idea business (a start-up) and the last one representing decline and demise. Here again, the problem is that high growth industry groups begin to mature, just as companies do, and this has been true for some segments of the tech sector.

In this post, I will begin by looking at how to value banks and follow up with an examination of investor views of banking have changed, by looking at pricing, before examining divergences in how banks are priced in the market today. All Equity, All the time!

In most time periods, those recalibrations and resets tend to be small and in both directions, resulting in the ups and downs that pass for normal volatility. Clearly, we are not in one of those time periods, as markets approach bipolar territory, with big moves up and down.

At the start of the year, the consensus of market experts was that this would be a difficult year for markets, given the macro worries about inflation and an impending recession, and adding in the fear of the Fed raising rates to this mix made bullishness a rare commodity on Wall Street. That pessimism was not restricted to market outlooks.

In this post, I will start with a working definition of riskt that we can get some degree of agreement about, and then look at multiple measures of risk, both at the company and country level. In closing, I will talk about some of the more dangerous delusions that undercut good risk taking. What is risk?

Private equity firms provide meaningful investment capital to growth-oriented businesses. Unlike venture capital firms, they do not invest primarily in start-ups. Businesses seeking expansion, change of investors, or even exit may benefit from private equity firms.

A long time ago, we received one complaint/criticism more than any other: “All your models start from templates ! What about case studies where I have to start from a blank Excel sheet and do not get any data, formatting, or schedules?”. usually takes at least 30 minutes and sometimes up to several hours.

My portfolio did “OK” (up 10% for the year), but it greatly underperformed the S&P 500 , which was up 24%. With better decisions, I could have been up 15 – 20% for the year and slightly above my levels from 2 years ago. Gold did well (up around 13%), but I had 10% or less in it the whole time.

In this post, I will look at corporate profitability, in all its different dimensions, and how companies across the globe, and across industries, measured up in the most recent years. As companies from around the globe look to Asia for growth, the ensuing competition is pushing margins down there, relative to the rest of the world.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings! Sometimes, less is more!

With technology speeding up the filing process, a 2002 rule changed those requirements to 60 days, for annual reports, and 40 days for quarterly reports, for companies with market capitalizations exceeding $700 million. The pre-game show is not restricted to analysts and investors, and markets partake in the expectations game in two ways.

Convertible bonds are hybrid instruments with elements of debt and equity, and some groups that trade convertible bonds also combine elements of S&T and IB. But before delving into the best candidates for these roles, typical trades, careers, and more, let’s start with the basic definitions: What is a Convertible Arbitrage Hedge Fund?

Yesterday, ConocoPhillips also disclosed that it expects to increase its ordinary base dividend per share by 34% to $0.78 starting in the fourth quarter of 2024. It targets repurchasing over $7 billion in shares in the first full year (up from over $5 billion standalone) and over $20 billion in shares in the first three years.

Second, they have all been in the news in the last few weeks, with Starbucks getting a new CEO, Walgreens announcing that they will be shutting down hundreds of their stores and Intel coming up in the Nvidia conversation, often as a contrast. and that lesson gets reinforced in business schools and books about business success.

When I started in finance, buybacks were almost unheard of; now, companies prefer to distribute cash through buybacks. companies have distributed more money through buybacks than through dividends. Finally, some lazy managers may use buybacks as a tool to manipulate short-term returns on equity and the stock price.

As I have valued Tesla over the years, I have come to the realization that it is the most 'uncar-like" automobile company in the world, and its uniqueness shows up on two dimensions. Put simply, the company has been able to scale up more quickly, while reinvesting less in capacity, than any other automobile company.

Traditionally, the sector was viewed as a defensive play for investors who wanted stable dividends and no drama. But over time, trends like market liberalization, deregulation, the shift to renewables, and the ESG religion “movement” have shaken up a sleepy sector.

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

Facebook: Filling in the Background It is worth noting that in good times, when earnings are rising and stock prices are upward bound, investors do not seem to have much interest in corporate governance, and it is only when the numbers start to move against them, that they rediscover the importance of the topic.

With equities, the metric that has been in use the longest is the PE ratio, modified in recent years to the CAPE, where earnings are normalized (by averaging over time) and sometimes adjusted for inflation. The other is the corporate bond market is under estimating both the risk and the consequences of default.

But before delving into the exit opportunities and the long-term outlook, let’s start with the fundamentals: Oil & Gas Investment Banking Defined. Midstream: 85 (mix of asset deals, M&A, debt, and even some private equity activity). Downstream: 31 (mix of everything, but no private equity activity).

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?),

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

According to some, you do almost no modeling or technical work in this group, and it’s one of the easier jobs in IB, similar equity or debt capital markets. But if you read other accounts, FSG runs models, Analysts get hands-on technical work, and the hours could be longer and more stressful because your clients are private equity firms.

Value play with strong dividend growth potential. However, most recently, the 50 DMA started to rise, and it seems like it can cross the 200DMA very soon. Instead of exporting to China, Volvo aims to ramp up sales by establishing a production site in the country. With the acquisition, Volvo aims to ramp up its sales in China.

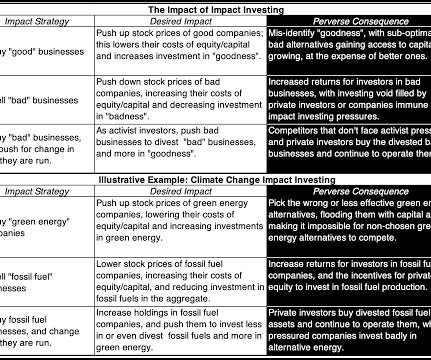

The effect of impact investing in the inclusionary and exclusionary paths is through the stock price , with the buying (selling) in inclusionary (exclusionary) investing pushing stock prices up (down), which, in turn, decreases (increases) the costs of equity and capital at these firms. in the 1998-2010 time period to 5.95

Currently, revenue from broadband makes up 20% of its service revenue. In March 2021, the China-backed company Dito started its commercial operations. In 3Q21, it recorded 51m users, up 10x compared to 2019. In 2019 and 2020, Globe recognized more than PHP4bn equity loss from its investment in Mynt. In 2021, it reached 1.4m

But then recruiting moved up, the MBA process became more structured, and now we have 4-year-olds aiming for “Target Kindergartens” so they can eventually get into investment banking ~15 years in the future. I’ll answer these questions, but, as usual, we need to start with some descriptions: Table Of Contents What is a Pre-MBA Internship?

SaaS start-ups are valued at 10x Sales”. Equity Vs. Enterprise Multiples – Which To Use? The ratio is either related to the Equity Value or ratios related to the Enterprise Value. . An example of an equity multiple: Price / Earnings. Common Types of Equity Valuation Multiples. Which Year to Use?

SaaS start-ups are valued at 10x Sales”. Equity Vs. Enterprise Multiples – Which To Use? The ratio is either related to the Equity Value or ratios related to the Enterprise Value. . An example of an equity multiple: Price / Earnings. Common Types of Equity Valuation Multiples. Which Year to Use?

Comment: If an applicable corporation sells a corporate subsidiary, that corporate subsidiary can get a fresh start in determining its applicable corporation status. In determining how to implement this rule, Treasury considered a “top-down” approach and a “bottom-up” approach for determining the adjustment.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content