This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When I started offering financial modeling training , I never expected to get questions about a methodology like the Dividend Discount Model (DDM). Otherwise, the written version follows: Why Use a Dividend Discount Model? If you sum up these numbers, you can see whether the company is valued appropriately.

per share, implying a total enterprisevalue of $5.6 With Smucker announcing the acquisition of Hostess Brands, some investors may be eyeing potential gains from the company’s dividends. As of now, Smucker has a dividend yield of 3.22%, which is a quarterly dividend amount of $1.06 Smucker Co. a share ($4.24

Marathon Oil Corporation (NYSE: MRO ) and ConocoPhillips (NYSE: COP ) stocks are moving in opposite directions on Wednesday after they disclosed a definitive deal in which ConocoPhillips will acquire Marathon Oil in an all-stock transaction with an enterprisevalue of $22.5 The acquisition price represents a 14.7%

In a final assessment, I break down companies based upon operating cash flows (EBITDA as a percent of enterprisevalue) and dividend yield (dividends as a percent of market capitalization).

Several analysts expressed their views on ConocoPhillips’ (NYSE: COP ) deal to acquire Marathon Oil Corporation (NYSE: MRO ) in an all-stock transaction with an enterprisevalue of $22.5 Yesterday, ConocoPhillips also disclosed that it expects to increase its ordinary base dividend per share by 34% to $0.78

By analysing factors such as the price-to-earnings (P/E) ratio, the price-to-book (P/B) ratio, and the enterprisevalue-to-EBITDA (EV/EBITDA) ratio, companies can determine whether their shares are undervalued or overvalued relative to its peers. A higher yield suggests an attractive income investment.

By analyzing factors like the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and enterprisevalue-to-EBITDA (EV/EBITDA) ratio, companies can determine if their shares are undervalued or overvalued compared to peers. Dividend Discount Model DDM estimates the present value of expected future dividends from owning a stock.

Absolute valuation is calculated through the discounted dividend model (DDM) method and discounted cash flow (DCF) method where you only focus on the stock and look at its dividends, cash flow, and growth. Often companies don’t pay dividends every quarter or every year hence making their payouts irregular. D0 = D1 ÷ (r – g).

Consequently, you can only value the equity in a bank, and by extension, the only pricing multiples you can use to price banks are equity multiples (PE, Price to Book etc.). The notion of computing a cost of capital for a bank is fanciful and fruitless, and any attempt to compute an enterprisevalue for a bank is destined to end in failure.

Example: Here’s an example of a particular metric you might use: In order to determine the EnterpriseValue of the business, you find the EBITDA from the business you’re valuing, and then multiply this by the EBITDA multiple observed from the other comparable companies. SaaS start-ups are valued at 10x Sales”.

Example: Here’s an example of a particular metric you might use: In order to determine the EnterpriseValue of the business, you find the EBITDA from the business you’re valuing, and then multiply this by the EBITDA multiple observed from the other comparable companies. SaaS start-ups are valued at 10x Sales”.

How does negative equity affect dividends? Is negative equity value common in startups? Introduction Brief Explanation of Equity Value Equity value, a cornerstone concept in finance, fundamentally represents the ownership interest in a company after all liabilities have been accounted for.

With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat. In decline, multiples of book value will become more common, with book value serving as a (poor) proxy for liquidation or break up value.

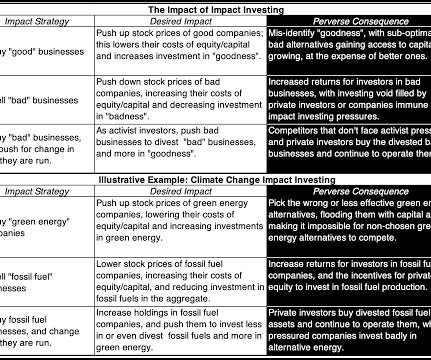

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. trillion of cumulated enterprisevalue at fossil fuel companies. in the 1998-2010 time period to 5.95

Uncover the intricacies of financial modeling, from understanding fundamental concepts like Free Cash Flow to Firm and Dividend Discount Model, to navigating advanced methodologies such as LBO and DCF. It provides a clearer picture of a company's ability to reward its shareholders with dividends or share buybacks.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation.

The transaction is expected to be more than 10% accretive to earnings per share and more than 20% accretive to cash available for dividend per share in 2025, and will enable us to continue investing in our business while increasing shareholder returns and maintaining a strong balance sheet."

Traditionally, the sector was viewed as a defensive play for investors who wanted stable dividends and no drama. Companies tend to offer high, stable dividend yields, and they finance their massive capital expenditures primarily with debt , with the highest leverage ratios of any industry outside of financial institutions.

At the company-level, I provide data on risk, profitability, leverage and dividends, broken down by industry-groups, to be used in both corporate finance and valuation. Financing Flows Accounting Returns Dividends & Ownership Risk Premiums 1. Dividend Payout & Yield 1. Dividends/FCFE & (Dividends + Buybacks)/ FCFE 2.

per share in cash, with the total value of the common shares equaling approximately $2.1 This transaction represents an enterprisevalue of approximately $7.4 Prior to closing, Textainer intends to maintain its current quarterly dividend on both the Textainer common and preference shares.

The transaction has an enterprisevalue of approximately $2.6 At the current time, the Company is not permitted to pay dividends on its outstanding shares of common stock under its existing indebtedness agreements. Riley Financial, Inc. billion, including the Company's net debt and outstanding preferred stock.

("BIP") (NYSE: BIP , TSX: BIP ), through its subsidiary Brookfield Infrastructure Corporation ("BIPC") and its institutional partners (collectively, "Brookfield Infrastructure"), jointly announce a definitive agreement for Triton to be acquired in a cash and stock transaction valuing the Company's common equity at approximately $4.7

Discounted Cash Flow Value Discounted Cash Flow Value refers to the calculation of a company’s EnterpriseValue on the basis of its ability to generate free cash flow over time. EBITDA Multiple EBITDA Multiple refers to the multiple of EBITDA used to determine a company’s enterprisevalue.

("Urstadt Biddle" or "UBP") (NYSE: UBA ) today announced that the two companies have entered into a definitive merger agreement (the "Agreement") by which Regency will acquire Urstadt Biddle in an all-stock transaction, valued at approximately $1.4 billion, including the assumption of debt and preferred stock.

billion 1 in enterprisevalue. Tyman shareholders will also be entitled to receive the final dividend of 9.5 Based on Quanex's last closing share price of $34.64 on April 19, 2024, the Consideration represents: A premium of approximately 35.1% to the closing price of the Tyman shares of 296.0 pence per Tyman Share.

However, there are some additional metrics and multiples that are useful for benchmarking sponsors, such as EnterpriseValue / Assets Under Management (TEV / AUM), “FRE” (Fee-Related Earnings), and assets under management vs. “ permanent capital.”. Your clients need to do deals to stay in business, so less “selling” is required.

million common shares as part of the Transaction, representing an equity value of approximately US$276 million on a fully diluted in-the-money basis, and an enterprisevalue of US$516 million. Alamos expects to issue approximately 20.3

VAALCO to acquire, through an indirect wholly-owned subsidiary, each TransGlobe share for 0.6727 of a VAALCO share; Implied TransGlobe equity value of US$307 million (with premium), and enterprisevalue of US$273 million assuming cash of US$37 million and debt of US$3 million as of March 31, 2022; A 24.9 percent and 45.5

The transaction values Newsight at US$215 million, which together with US$102.5 million cash in VSAC's trust account, assuming no redemptions in the business combination and the addition of proceeds of a possible financing of up to $40 million outlined below, results in a combined pro forma enterprisevalue of US$380 million.

EXAMPLE: Let’s say you’re planning to have 10 portfolio companies in your first fund, and the average Purchase EnterpriseValue will be $50 million. Distributions: How frequently will you distribute dividends, cash flows, interest, and realized gains to your LPs?

If you are comparing across companies in these sectors, that may not be an issue, but if you are valuing companies and want to find a target value for margins or accounting returns, you will be better served using my archived values for these variables from 2019.

Strictly speaking, the result to be taken into account should be the free cash flow generated by the company, i.e. the cash flow actually available to a buyer to repay acquisition debt, through the distribution of dividends: this is the DCF method (for Discounted Cash-Flows), which is detailed below. RCAI, RN, CIF.

An intuitive reading of the FCFE is that it is cash available to be returned to equity investors, either in the form of dividends or as cash buybacks. It is the rare firm that follows a residual cash policy, returning its FCFE every year as dividends and/or buybacks.

NASDAQ: PYCR ) in an all-cash transaction representing an enterprisevalue of around $4.1 Paychex plans to maintain its dividend policy and strong balance sheet, with committed financing in place for the. (NASDAQ: PAYX ) shares are trading higher on Tuesday after the company disclosed a deal to fully acquire Paycor HCM, Inc.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprisevalue) as recently as ten years ago, and barely making the top ten list five or six years ago.

Growth Equity Interview Questions: Technical Concepts As with private equity interviews , they could potentially ask you about anything: Accounting , equity value and enterprisevalue , valuation and DCF analysis , and even merger models and LBO models. Explain how the Equity Value, EnterpriseValue, and ownership change.

d/b/a H&E Rentals (NASDAQ: HEES ) ("H&E") today announced their entry into a definitive agreement under which United Rentals will acquire H&E for $92 per share in cash, reflecting a total enterprisevalue of approximately $4.8 Notably, the transaction will not impact the company's current dividend program.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content