This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

billion in netdebt, reducing total debt to GBP 17.5 (USD Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD Due to these high earnings, the company was able to pay back GBP 7.5 (USD Since publishing these figures, BP’s share price has risen by more than 15%.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation. Calculating EV/EBITDA: $2.5

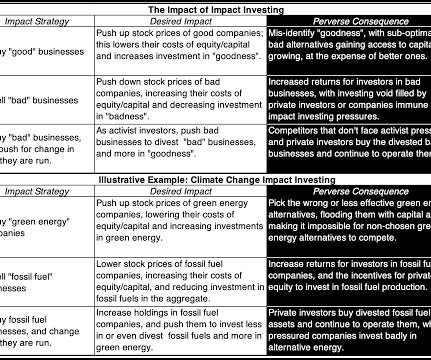

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. in the 1998-2010 time period to 5.95 in the 2011-2023 time period.

billion, and the assumption of netdebt of approximately $600 million, subject to required court, LifeWorks shareholder, stock exchange and regulatory approvals (the " Transaction "). (TSX: LWRK ) pursuant to which TELUS will acquire all of the issued and outstanding common shares of LifeWorks for $33.00

Including the Company's pro-rata share of joint venture cash and debt of $4.5 million, respectively, results in a third quarter 2022 netdebt to annualized adjusted EBITDA ratio of 7.0x. million of undrawn forward equity, the netdebt to annualized adjusted EBITDA ratio would be 6.0x. to $1.05.

The Transaction implies a multiple of less than 9x the projected forward Adjusted EBITDA and is immediately accretive, with DCF per share accretion in the mid-teens 4 , 5 , 6. The Dividend Equivalent Payment will be made on the later of the closing date of the Transaction and the date the dividend is paid to holders of Common Shares.

Enhancing Financial Profile: Expected to be immediately accretive to adjusted net earnings per share 3 with significant further opportunities for Adjusted EBITDA margin 3 enhancement and revenue and cost synergies. million), reflects POWER's estimated 2024 pre-IFRS 16 adjusted EBITDA 3 at a multiple of 15.2x, or 12.5x

billion of netdebt. On a trailing 12-month basis through September 30, 2024, H&E generated $696 million of adjusted EBITDA on total revenues of $1,518 million, translating to an adjusted EBITDA margin of approximately 45.8%. adjusted EBITDA for the trailing 12 months ended September 30, 2024, or 5.8x

Equity is cheaper than debt: There are businesspeople (including some CFOs) who argue that debt is cheaper than equity, basing that conclusion on a comparison of the explicit costs associated with each interest payments on debt and dividends on equity.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content