This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When I started offering financial modeling training , I never expected to get questions about a methodology like the Dividend Discount Model (DDM). Otherwise, the written version follows: Why Use a Dividend Discount Model? The main argument in favor of the DDM is that it best represents what happens in real life when you buy a stock.

By analysing factors such as the price-to-earnings (P/E) ratio, the price-to-book (P/B) ratio, and the enterprise value-to-EBITDA (EV/EBITDA) ratio, companies can determine whether their shares are undervalued or overvalued relative to its peers. A higher yield suggests an attractive income investment.

In a final assessment, I break down companies based upon operating cash flows (EBITDA as a percent of enterprise value) and dividend yield (dividends as a percent of market capitalization).

By analyzing factors like the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and enterprise value-to-EBITDA (EV/EBITDA) ratio, companies can determine if their shares are undervalued or overvalued compared to peers. Dividend Discount Model DDM estimates the present value of expected future dividends from owning a stock.

Kronos acquired the 50% joint venture interest that it did not already own for an upfront cash payment of $185 million (subject to working capital adjustments) and a potential earn-out payment of up to $15 million based on Kronos' aggregate consolidated net income before interest expense, income taxes and depreciation and amortization expense, (..)

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat. With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdle rate being the pay off.

The transaction is expected to be more than 10% accretive to earnings per share and more than 20% accretive to cash available for dividend per share in 2025, and will enable us to continue investing in our business while increasing shareholder returns and maintaining a strong balance sheet." third quarter of 2024 annualized adjusted EBITDA.

The income-based approach determines a company’s value by assessing its anticipated future income-generating potential, employing methodologies such as Discounted Cash Flow (DCF) Analysis, Capitalization of Earnings, the Income Multiplier Method, Dividend Discount Model (DDM), and Earnings-Based Valuation. Calculating EV/EBITDA: $2.5

– Net Proceeds are expected to be used for general corporate purposes including, but not limited to, additional debt repayment and dividend payments –. EBITDA multiple on 2019 results and a $455K per key valuation –. Price implies a blended 2.9% cap rate and 27.0x PHILADELPHIA, Sept.

Through our diversified and primarily contracted clean energy portfolio, Clearway Energy endeavors to provide our investors with stable and growing dividend income. Our portfolio comprises approximately 11.7 GW of gross capacity in 26 states, including 9 GW of wind, solar, and battery energy storage and over 2.7 Clearway Energy, Inc.'s

Uncover the intricacies of financial modeling, from understanding fundamental concepts like Free Cash Flow to Firm and Dividend Discount Model, to navigating advanced methodologies such as LBO and DCF. It provides a clearer picture of a company's ability to reward its shareholders with dividends or share buybacks.

If a transaction is completed, it is anticipated that the free cash flow, Adjusted EBITDA and Non-GAAP EPS of Franchise Group would significantly increase.

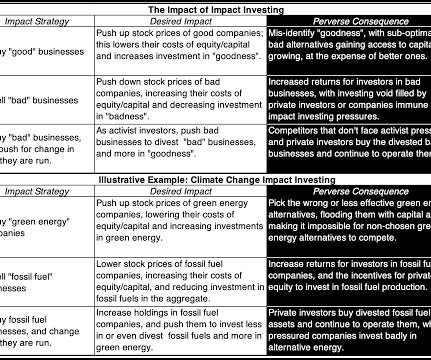

Even when you are successful in dissuading these companies from "bad" investments, but may not be able to stop them from returning the cash to shareholders as dividends and buybacks, rather than making "good" investments. in the 1998-2010 time period to 5.95 in the 2011-2023 time period.

"On the strength of the contracted cash flows from this acquisition, we are increasing our annual dividend growth guidance to 6% through 2025 from the previous 5%. Subject to Board approval, this will include a 6% dividend increase for 2022 and represents our ninth consecutive year of dividend increases," stated Mr. Vaasjo. . "We

Adjusted EBITDA rose by. Adjusted EPS was $3.21, up from $2.49 a year ago, above the consensus of $2.86. Adjusted EBIT increased 18% Y/Y to $392 million, with margin expanding to 17% from 15% prior year quarter. Full story available on Benzinga.com

Per the company's chief executive, Sean Reilly, "The revenue gain, combined with continued discipline on expenses, allowed us to produce adjusted EBITDA growth of nearly 7% and diluted AFFO per share growth of 9.5%. Also, we continue to pace at the top end of our previously provided guidance of $7.75

net principal debt-to-annualized EBITDA ratio for 1Q‘24 (vs. per share cash dividend declared _ (1) A reconciliation of GAAP net income to FFO is provided at the end of this press release. For the first quarter of 2024, ROIC's net principal debt-to-annualized EBITDA ratio was 6.4 per share cash dividend.

million Adjusted EBITDA of $237.6 million one-time special dividend payment, $59.0 million Adjusted EBITDA of $68.2 million Adjusted EBITDA of $237.6 million one-time special dividend payment, $59.0 million Adjusted EBITDA of $68.2 Full Year 2023 Highlights 1 Revenues of $763.8 million Net Income of $37.3

RSDs are not value drivers like EBITDA, gross profit, number of cases, or any other value drivers. Company A’s annual dividend for the 10% interest is $100,000, which provides a 10% expected dividend yield based on the MM/FC value of the interest. An RSD simply measures the difference between two prices.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporate finance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

Based on the first-quarter financial performance, Devon declared a fixed-plus-variable dividend of $0.72 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. Despite a decline in realized prices for all commodities, the company upholds steady growth. billion using a WACC of 11.7%. billion to USD 35.4

1) This transaction is consistent with Berry's shareholder return model, which provides that 20% of annual post-fixed dividend Adjusted Free Cash Flow (2) will be returned to shareholders through variable dividends and the remaining 80% will be used for stock and debt repurchases, as well as bolt-on acquisitions such as this one.

Adjusted EBITDA and EPS Guidance Affirmed, Outlook Updated to Reflect FX Translation Global Restructuring Expected to Yield $40 Million in Profit Growth in 2023 Balanced Capital Allocation Strategy Includes NoteMachine Acquisition and Continued Share Repurchases. GAAP net income up 1% to $19 M; adjusted EBITDA up 11% to $189 M.

If you want to understand how to value a business, the first question is whether to look at a multiple of SDE , EBITDA or Revenue. SDE vs. EBITDA vs. Revenue. Crucially, any owner salary/dividends can be added back to the profit number, too. If you want an accurate valuation, you can receive a free one via our page here.

Additionally, NVIDIA returned USD 99 million in cash dividends to shareholders, exemplifying its financial robustness. The Trading Comparables analysis resulted in a valuation range of USD 60 billion to USD 277 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. and Cisco Systems, Inc.

Furthermore, there are concerns regarding IBM’s uncertain dividend and recent acquisition spree. The Trading Comparables analysis resulted in a valuation range of USD 106 billion to USD 235 billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. and Alphabet Inc.

Furthermore, the company increased dividends by 10% and announced that it will buy back GBP 2.3 (USD The Trading Comparables analysis resulted in a valuation range of GBP 98 (USD 199) billion to GBP 137 (USD 166) billion by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B. billion worth of shares.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B.

At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. Valutico Analysis.

At this level the dividend yield is 2.8%. . The Trading Comparables analysis resulted in a valuation range of CHF 47 to 83 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT and P/E. ABB performed particularly well in the COVID years 2020-2021, almost doubling its share price during this period. Valutico Analysis.

This strong share price performance was further bolstered by an average gross annual dividend yield of roughly 6% over the past 10 years. Our Trading Comparables analysis produced a valuation range of €178 billion to €222 billion, by applying the observed trading multiples EV/EBITDA, EV/EBIT, P/E and P/B.

times estimated 2023 adjusted EBITDA multiple. Targa now estimates standalone 2022 adjusted EBITDA to be between $2.675 billion and $2.775 billion and year-end leverage ratio of about 2.7 Underpinned by long-term high-quality producer dedications. billion acquisition price represents approximately 7.5 times and improving thereafter.

net principal debt-to-annualized EBITDA ratio for 4Q‘22 (vs. per share cash dividend paid _ (1) A reconciliation of GAAP net income to Funds From Operations (FFO) is provided at the end of this press release. Additionally, ROIC's net principal debt-to-annualized EBITDA ratio for the fourth quarter of 2022 was 6.6

net principal debt-to-annualized EBITDA ratio for 3Q‘24 (vs. per share cash dividend declared _ (1) A reconciliation of GAAP net income to FFO is provided at the end of this press release. For the third quarter of 2024, ROIC's net principal debt-to-annualized EBITDA ratio was 6.3 per share cash dividend.

million in Horizon Adjusted EBITDA in 2022. 2022 Horizon Adjusted EBITDA multiple net of synergies 2 Approximately $51,000 per fiber route mile Financing Shentel intends to fund the Transaction with a combination of existing cash resources, revolving credit facility capacity and an amended and upsized credit facility. 3 Includes $9.6

4) Big payouts – dividends and stock buyback. (5) Estimate Terminal Value – Terminal Value is then estimated either by using a terminal exit multiple (usually an EBITDA multiple) or with a Terminal Growth Rate ( Gordon Growth Method). 2) Shrinking or negative margins. (3) 3) Asset divestitures. (4)

Activist Directors – Determinants Our research shows that activists are more likely to demand or acquire board representation if the firm has higher levels of institutional ownership, a smaller market capitalization, worse stock market performance, and, in particular, lower dividend payouts.

billion in sales and adjusted EBITDA of $340 million, an increase of 47% compared to the $232 million of adjusted EBITDA generated during fiscal year 2021. For fiscal year 2022, Worthington's Consumer Products, Building Products and Sustainable Energy Solutions businesses delivered $1.3

Even more specifically, private equity firms want to see at least 20 to 25 percent annual profit, which may require the company to improve EBITDA, obtain economies of scale or synergies, and earn high margins. The target company’s facts and figures must support those forecasts.

million, respectively, results in a third quarter 2022 net debt to annualized adjusted EBITDA ratio of 7.0x. million of undrawn forward equity, the net debt to annualized adjusted EBITDA ratio would be 6.0x. As previously announced, the Board of Trustees declared a fourth quarter 2022 regular cash dividend of $0.13 to $1.05.

—Fifth Consecutive Quarter of Gross Margin Expansion— —Industry-Leading Operational Performance at Pre-Pandemic Levels— —34% Growth in Adjusted EBITDA Year-Over-Year— JASPER, Ind., Adjusted EBITDA of $15.4 Adjusted EBITDA of $15.4 Adjusted EBITDA increased year-over-year by 34% to $15.4 Net income of $5.7 million, up $3.9

Strictly speaking, the result to be taken into account should be the free cash flow generated by the company, i.e. the cash flow actually available to a buyer to repay acquisition debt, through the distribution of dividends: this is the DCF method (for Discounted Cash-Flows), which is detailed below. EBITDA and EBIT). EBE and ENE.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content