This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equity riskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

Definition of Equity RiskPremium. It is the difference between expected returns from the stock market and the expected returns from risk-free investments. What Impacts the Equity RiskPremium? How Do You Calculate Equity RiskPremium? Why is the Equity RiskPremium Important?

Capital Asset Pricing Model (CAPM): According to CAPM, the expected return on a stock has two main components: the risk-free rate and a riskpremium. The risk-free rate represents the return an investor can get without taking on any risk, typically derived from government bonds.

Investors all talk about risk, but there seems to be little consensus on what it is, how it should be measured, and how it plays out in the short and long term. In closing, I will talk about some of the more dangerous delusions that undercut good risk taking.

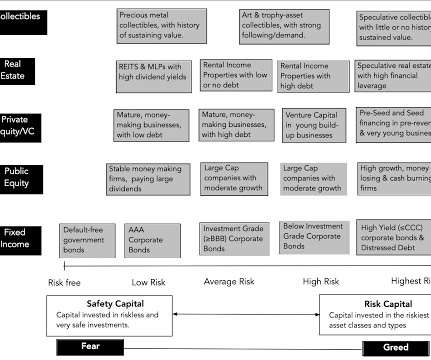

In this post, I will argue that almost everything that we are observing in markets, across asset classes, can be explained by a pull back on risk capital, and that understanding the magnitude of the pull back, and putting in historical perspective, is key to gauging what is coming next. Risk Capital: What is it?

Risk Free Investments: Definition, Role and Measures The place to start a discussion of risk-free rates is by answering the question of what you need for an investment to be risk-free, following up by seeing why that risk-free rate plays a central role in corporate finance and investing and then looking at the determinants of that risk-free rate.

Definition of Capital Asset Pricing Model. It helps an investor understand what to expect to earn in relation to the risk-free rate and the market return. CAPM assumes that the minimum a rational investor would earn is the risk-free rate by buying the risk-free asset. How Do You Calculate the Capital Asset Pricing Model?

Definition of the Arbitrage Pricing Theory. It is a model based on the linear relationship between an asset’s expected risk and return. The return on assets is determined by systematic factors such as changes in inflation , riskpremiums, interest rates, etc. What Impacts the Arbitrage Pricing Theory? ER(x) = Rf + ??1

A high M-Score could indicate higher risk, warranting a higher discount rate and thus a lower valuation. It's important to remember that the M-Score is a probabilistic tool, not a definitive verdict. It's like adding a riskpremium, but based on hard data rather than gut feeling.

There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdle rate for a business? as mature markets. for Ford).

When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Debt breakdown 2.

The definition of "net equity" is as follows: equity of the company = sum of subscribed capital, share premiums, revaluation reserves, reserves and retained earnings, minus the tax value of the company's holdings in associated companies and the tax value of its own shares. Two limitations are already apparent.

Implicit in this definition are two key components of inflation. The first is that to define purchasing power, you have to start with a definition of what you are purchasing, and this detail, as we will see, can lead to differences in inflation measured over a given period, across measures/services.

If it looks like I am over reaching, I start my corporate finance class with the simple proposition that any decision that involves money is a corporate finance decision, and by that definition everything that businesses do falls under its umbrella. The links to all of these classes are at the end of this post.

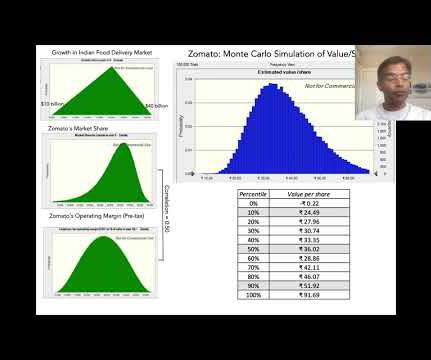

Raising or lowering the cost of capital has an effect on value, but changing my assumptions about riskpremiums, betas or debt ratios has a much smaller effect that changing assumptions that alter cash flows. The Zomato IPO clocks in at 420 pages , much of it designed to bore readers into submission.

The purpose and definition of the valuation engagement in accordance with BVS–I General Requirements for Developing a Business Valuation, including the applicable standard (type) and premise of value. Every appraisal must have a stated purpose and definition of the valuation (i.e., the standard of value).

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. In computing the latter, I used the current debt ratios for firms, but made no attempt to evaluate whether these mixes were "right" or not.

In my last post , I described the wild ride that the price of risk took in 2020, with equity riskpremiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year.

The second is that what comprises default in the sovereign CDS market may not coincide with investor definitions of default , though there are approaches that can be used to back out the likelihood of default from a CDS value. in my July 2023 update) and apply this scalar to the default spread, to arrive at a country riskpremium.

Risk Surge and Economic Viability : In my last post, I noted the surge in Russia's default spread and country riskpremium, making it one of the riskiest parts of the world to operate in, for any business. That is easier said than done, though, because as with all things ESG, those risks are in the eyes of the beholder.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

Even assuming away default risk, a ten-year treasury is not risk free, with a one time horizon, and a 3-month treasury is definitely not riskfree, if you have a 10-year time horizon. Data Links Intrinsic risk free rates and Nominal interest rates Bond Default Spreads and Equity RiskPremiums

In fact, the working definition that some commenters used for return on equity was obtained by dividing the net income by the market value of equity. As I noted at the start of this post, it was motivated by trying to clear up a fundamental misunderstanding of what return on equity measures.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity riskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content