This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

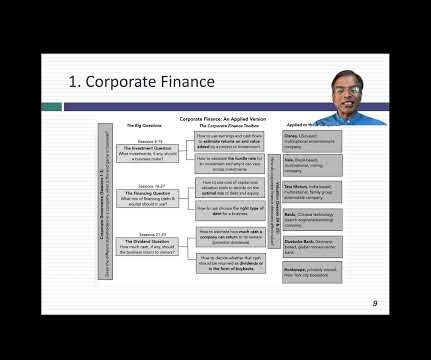

The six classes that I prepped for in those two years ranged from banking to investments to corporate finance, and while I have never worked harder, much of what I teach today came out of those classes. In 1984, I moved on to the University of California at Berkeley, as a visiting lecturer, teaching anything that needed to be taught.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

In the world of finance and investing, the concept of beta plays a vital role in assessing an investment’s risk and volatility. Beta, in finance, is a measure of a stock or portfolio’s sensitivity to market movements. Step 3: Calculate Covariance Determine the covariance between the asset returns and the market returns.

Other corporate distributions that have a similar effect on ownership are cash financed acquisitions and going private transactions. The overall impact of corporate aggregate distributions depends on the magnitude of such distributions and their covariation with institutional-level flows. Equity Market,” available here.

The portfolio return variance is calculated by multiplying the squared weight of each asset by its variance and adding two times the weight of each asset multiplied by the covariance of the asset pair. The covariance of the assets is sqrt(0.3)*sqrt(0.2) The portfolio standard deviation is the square root of the portfolio variance.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content