This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage.

While the universe of companies is diverse, with approximately half of all firms from emerging markets, it is more concentrated in marketcapitalization, with the US accounting for 40% of global marketcapitalization at the start of the year. Macro Data I do not report much macroeconomic data for two reasons.

In this section, I will lay out a mechanism for evaluating the effects of borrowing on the cost of funding a business, i.e., the cost of capital, and talk about why firms may under or overshoot this optimal.

Regional Breakdown My data sample for 2022 includes every publicly traded firm that is traded anywhere in the world, with a marketcapitalization that exceeds zero. A few of these variables are macro variables, but only those that I find useful in corporatefinance and valuation, and not easily accessible in public data bases.

Since I am lucky enough to have access to databases that carry data on all publicly traded stocks, I choose all publicly traded companies, with a market price that exceeds zero, as my universe, for computing all statistics. Equity RiskPremiums 2. Return on (invested) capital 2. Costs of equity & capital 4.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity riskpremiums , and the latter by default spreads.

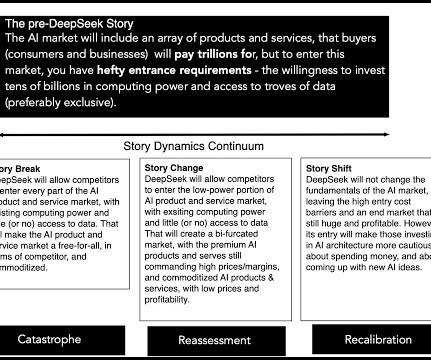

Since the companies involved in building the AI infrastructure are the ones that are most tangibly (and immediately) benefiting from the AI boom, they are also the companies that have seen the biggest boost in market cap, as the AI story heated up.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content