This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have been reading my posts, you know that I have an obsession with equityriskpremiums, which I believe lie at the center of almost every substantive debate in markets and investing. That said, I don't blame you, if are confused not only about how I estimate this premium, but what it measures.

The other is the dangerous notion that measuring risk is the same as managing that risk and, in some cases, the even more insane view that it removes that risk. In corporatefinance, this takes the form of a hurdle rate , a minimum acceptable return on an investment, for it to be funded.

A few of these variables are macro variables, but only those that I find useful in corporatefinance and valuation, and not easily accessible in public data bases. Rather than replicate that data, my macroeconomic datasets relate to four key variables that I use in corporatefinance and valuation.

In my corporatefinance class, I describe all decisions that companies make as falling into one of three buckets – investing decisions, financing decision and dividend decisions. Beta & Risk 1. Return on Equity 1. EquityRiskPremiums 2. Costs of equity & capital 4. Buybacks 2.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. What is a risk free investment? Why does the risk-free rate matter?

If 2022 was an unsettling year for equities, as I noted in my second data post, it was an even more tumultuous year for the bond market. The rise in rates transmitted to corporate bond market rates, with a concurrent rise in default spreads exacerbating the damage to investors.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. When valuing or analyzing a company, I find myself looking for and using macro data (riskpremiums, default spreads, tax rates) and industry-level data on profitability, risk and leverage. Cost of Equity 1.

In my last three posts, I looked at the macro (equityriskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

To fund the business, you can either use borrowed money (debt) or owner's funds (equity), and while both are sources of capital, they represent different claims on the business. Even government-owned businesses fall under its umbrella, with the key difference being that equity is provided by the taxpayers.

Gianfala is a Vice President of the Valuation Advisory group with over 15 years of experience in accounting, corporatefinance, and business valuations. Nene Gianfala | ASA-BV/IA, CPA/ABV | Vice President, Shareholder | Chaffe and Associates Ms. She joined Chaffe & Associates, Inc. Tax Valuation Services.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

With stocks, I compute this pre-personal tax return at the start of every month, using the current level of index and expected cash flows to back out an internal rate of return; this is the basis for the implied equityriskpremium.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Beta & Risk 1. Return on Equity 1.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to riskpremiums, but it is not my preferred habitat. A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses.

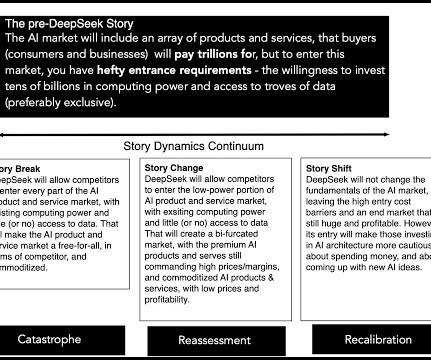

The value per share that I estimate for Nvidia dropped from $87 in September 2024 to $78 in January 2025, much of that change driven by the smaller AI chip market that comes out of the DeepSeek disruption (with the rest of the decline arising for higher riskfree rates and the equityriskpremiums).

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equityriskpremiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in riskpremiums, i.e., my definition of a crisis.

17] See [link] (showing the United States has among the lowest equityriskpremiums in the world); Luzi Hail and Christian Leuz, International Differences in the Cost of Equity Capital: Do Legal Institutions and Securities Regulation Matter?, Division of CorporationFinance, No Action Letter: Latham and Watkins (Mar.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content