This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

” Intangible assets are increasingly seen to be driving enterprisevalue creation across sectors and industries. Bradford Cornell United States Emeritus Professor of Finance, UCLA. Alexandre Pierantoni Brazil Managing Director and Head of Brazil CorporateFinance, Kroll. Former Deputy Chair, IOSCO.

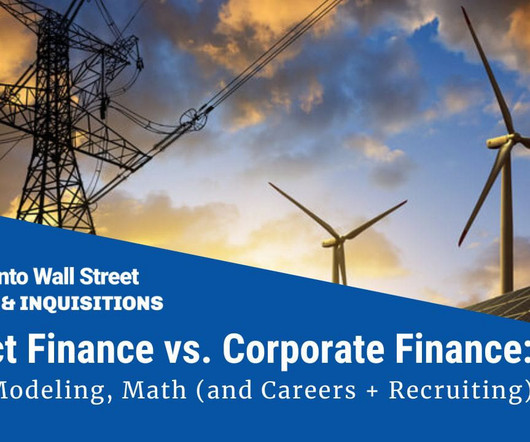

With the craze over renewable energy and infrastructure over the past few years, we’ve received more and more questions about Project Finance vs. CorporateFinance. And yes, coincidentally, we have a new Project Finance & Infrastructure Modeling course.

Among those who study corporate financial distress and reorganization, the notion that senior lenders are in control is deeply ingrained. Celebrated papers in the law and corporatefinance literatures attribute lender influence during periods of distress to blue-sky contracting practices. [1] 917 (2003); Douglas G. 751 (2002).

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive.

It is 100% possible to use standard valuation multiples, such as P / E and TEV / EBITDA , to value power/utility companies, and you’ll see many examples in the Fairness Opinions below. EnterpriseValue / Capacity ($ per MW): Finally, for power generation companies, capacity is the key top-line driver that determines revenue.

Specifically, private equity is not feasible from most ECM or DCM teams, hedge funds are also challenging, venture capital is a stretch, and you won’t have the right skills for corporate development. If you want a long-term finance career (stay in banking or switch to private equity, corporate development, hedge funds, etc.),

There can be certain aspects around a new drug release that can make or break the enterprisevalue of a target. Telecom, for example, requires a significant level of government scrutiny. Also, pharma. Many complications come into the mix. But I would argue that geopolitics create a lot of challenges.

Let’s dive in! Introduction Leveraged Buyouts (LBOs) are some of the most intriguing yet complex mechanisms in corporatefinance. This price is often calculated using valuation multiples, such as EnterpriseValue to EBITDA (EV/EBITDA). Ready to master the art of LBOs?

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. If you use it at their jobs as corporatefinance or equity analysts, I am glad to take some of that burden off you, and I hope that you find more enjoyable uses for the time you save.

7] I was serving as counsel to then-Commissioner Michael Piwowar at the time and was given a briefing by then-director [of the Division of CorporationFinance] Keith Higgins on the reversal. While shareholder proposals that limit management entrenchment can add value to a company, [27] others may not. 67] See supra note 12. [68]

Cash generating capacity : Debt payments are serviced with operating cash flows, and the more operating cash flows that firms generate, as a percent of their market value, the more that they can afford to borrow.

Country Risk in Business Most corporatefinance classes and textbooks leave students with the proposition that the right hurdle rate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content