This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

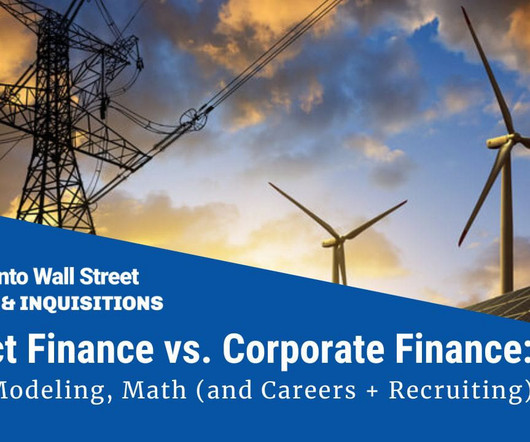

With the craze over renewable energy and infrastructure over the past few years, we’ve received more and more questions about Project Finance vs. CorporateFinance. And yes, coincidentally, we have a new Project Finance & Infrastructure Modeling course.

Furthemore, adjusted underlying EBITDA was £11.1m, up 14% compared with the same period last year (£9.7m). The corporatefinance market is highly active as capital continues to be deployed. Geoff Rowley, CEO, said: “The markets we operate in have been mixed.

These three categories have a lot in common: External Parties – Unlike corporatefinance roles such as FP&A , in credit, you always analyze external parties such as customers, borrowers, or clients paying for ratings. EBITDA / Interest: This company is at 3x vs. 5x for peer companies.

Snaitech generated $285 million of adjusted EBITDA in 2023 and NSX is expected to report $34 million of adjusted EBITDA for 2024, according to New York-based investment bank Needham & Company. The sports betting giant spent roughly $3 billion in total; both acquisitions are expected to close in the second quarter of 2025.

Leveraged Buyout (“LBO”) is a quite common term in CorporateFinance field. It refers to acquiring a company (or its part) and financing it with debt. Senior Bank Debt / EBITDA 3.0x.

By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. EV/EBIT and EV/EBITDA 4. Cost of Capital 3.

In my corporatefinance class, I describe all decisions that companies make as falling into one of three buckets – investing decisions, financing decision and dividend decisions. Financing Flows 5. EBIT & EBITDA multiple s 5. Dividend yield & payout 3. Default Spreads 3. Margins & ROC 3. Tax rates 4.

Its financial profile now looks like this: Its Debt / EBITDA is now 10x, its EBITDA / Interest has fallen below 1x, the Secured Debt is trading at 90% of its face value, and the Unsecured Debt is down to 60%. A few years later, the company’s industry declined, and it was slow to cut costs and enter new markets.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Of course, just as there are companies that choose other dysfunctional corporatefinance choices.

In fact, that objective of value maximization drives every aspect of the business, as can be seen in this big picture perspective in corporatefinance: For some companies, especially mature ones, value and profit maximization may converge, but for most, they will not.

One simplistic proxy for this cash generating capacity is EBITDA as a percent of enterprise value (EV), with higher (lower) values indicating greater (lesser) cash flow generating capacity. Debt to EBITDA, Interest Coverage Ratios If debt to capital is not a good measure for judging over or under leverage, what is?

Let’s dive in! Introduction Leveraged Buyouts (LBOs) are some of the most intriguing yet complex mechanisms in corporatefinance. Start by evaluating profitability metrics such as EBITDA, operating margins, and net income. Start by projecting the target company’s income statement, including revenue, costs, and EBITDA.

And in fields like corporatefinance , much of the recruiting happens at schools that are “semi-targets” for investment banking, such as ones in the #30 – #50 range in the U.S. But the problem is that revenue will also fall if advertisers flee, so even if the company’s margins improve, cash flow, EBITDA, etc.,

If Midstream companies want to grow beyond the fee increases written into their contracts and possible volume growth, they need to spend on Growth CapEx and estimate the incremental EBITDA from that spending: Further adding to the complexity is the GP (General Partner) / LP (Limited Partner) structure used at most MLPs.

That gets you thinking about materials companies that might benefit from this trend, so you research the sector and run a screen looking for companies with FCF yields >= 10%, revenue growth >= 10%, and TEV / EBITDA multiples <= 15x.

The fundamentals do not relate to EBITDA , Free Cash Flow , or valuation multiples but to factors like the weather, human behavior, geopolitics, and supply and demand. You think about these issues and commodity-specific factors, such as pipeline/plant capacity, outages, and new drilling activity for oil, to predict how prices might change.

When profits are scaled to revenues, you get margins, and as with absolute earnings, margins come in various forms, as can be seen below: In addition to margins based upon income measures (gross, operating, after-tax operating and net), there are other margin variations, with EBITDA and after-tax operating margins coming into play.

And in that short time, it’s imperative to focus on value creation and EBITDA. Shareholder value creation was the overriding thesis, but the journey to getting there was going to be impossible for them with their current balance sheet and financial structure. That is almost always the guiding north star.

Accounting 101 I am not an accountant, and have no desire to be one, but I have used their output (accounting statements) as raw material in valuation and corporatefinance. billion, which results in an adjusted PE ratio of about 6.

It is 100% possible to use standard valuation multiples, such as P / E and TEV / EBITDA , to value power/utility companies, and you’ll see many examples in the Fairness Opinions below. Books: Fisher Investments on Utilities , Principles of Utility CorporateFinance , and a metric ton of books on renewables.

Finally, many renewable energy debt deals take place within Project Finance teams at banks – but Project Finance and corporatefinance are very different ! If you look at the presentations and valuations below, you will still see standard valuation multiples like TEV / Revenue, TEV / EBITDA, and P / E.

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdle rates, central to both corporatefinance and investing judgments.

We’re particularly happy that this represents a significant increase in our offering for Venture Capital and CorporateFinance firms across the 70 countries Valutico is already being used in. CEO of Valutico, Paul Resch stated: “We’re extremely excited to announce the new VC method as part of Valutico’s ever-expanding toolbox.

Users can also delve into in-depth deal specifics, like stake purchases, deal amounts, and crucial multiples such as EV/Sales, EV/EBITDA, EV/EBIT and P/E. Detailed information on deals, buyer profiles, and industry medians can also be found within the system, making it an impressive and full-bodied tool for finance professionals.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Financing Flows 5. Book Value Multiples 3.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. The EBITDA margin is an intermediate stop, and it serves two purposes.

Country Risk in Business Most corporatefinance classes and textbooks leave students with the proposition that the right hurdle rate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content