This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Corporatefinance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. In my view, corporatefinance jobs are not ideal “stepping stone roles.”

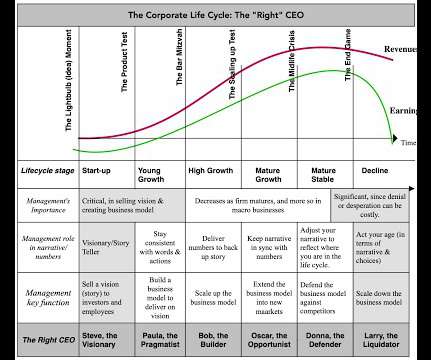

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

Continuing an annual ritual of long standing, ahead of starting my spring teaching at NYU starting in a couple of weeks, I would like to invite you, if you are interested, to come along for the ride. In 1984, I moved on to the University of California at Berkeley, as a visiting lecturer, teaching anything that needed to be taught.

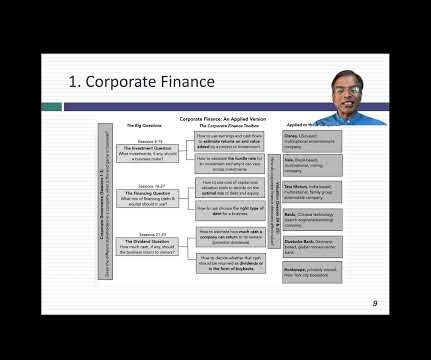

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

As part of that obsession, since September 2008, I have estimated an equity risk premium for the S&P 500 at the start of each month, and not only used that premium, when valuing companies during that month, but shared my estimate on my webpage and on social media.

At the start of every semester for as long as I can remember, I have invited people to sit in informally on my classes at NYU or take the shorter online versions on my website. If you have a bigger budget, I would try to emulate Professor Andrew Lo , who described his astounding set up for teaching last year.)

In this post, I will start with a working definition of riskt that we can get some degree of agreement about, and then look at multiple measures of risk, both at the company and country level. In corporatefinance, this takes the form of a hurdle rate , a minimum acceptable return on an investment, for it to be funded.

I also start thinking about my passion, which is teaching, the spring semester to come, and the classes that I will be teaching, repeating a process that I have gone through every year since 1984, my first year as a teacher. Face up to uncertainty, rather than avoid or deny it : Uncertainty is a feature of investing/ business, not a bug.

Facebook: Filling in the Background It is worth noting that in good times, when earnings are rising and stock prices are upward bound, investors do not seem to have much interest in corporate governance, and it is only when the numbers start to move against them, that they rediscover the importance of the topic.

In this post, I will look at corporate profitability, in all its different dimensions, and how companies across the globe, and across industries, measured up in the most recent years.

But before delving into the best candidates for these roles, typical trades, careers, and more, let’s start with the basic definitions: What is a Convertible Arbitrage Hedge Fund? If the stock price goes up or down by 10%, but the volatility stays the same, you might not earn or lose anything on the trade.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

But then recruiting moved up, the MBA process became more structured, and now we have 4-year-olds aiming for “Target Kindergartens” so they can eventually get into investment banking ~15 years in the future. I’ll answer these questions, but, as usual, we need to start with some descriptions: Table Of Contents What is a Pre-MBA Internship?

In my last post, I talked about the ritual that I go through every year ahead of my teaching each spring, and in this one, I will start on the first of a series of posts that I make at the start of each year, where I look at data, both macro and company-level. That is not true!

Traditionally, the sector was viewed as a defensive play for investors who wanted stable dividends and no drama. But over time, trends like market liberalization, deregulation, the shift to renewables, and the ESG religion “movement” have shaken up a sleepy sector.

In this post, I start by looking at the end game for businesses, and how that choice plays out in investment rules for these businesses, and then examine how much businesses generated in profits in 2023, scaled to both revenues and invested capital. The End Game in Business If you start a business, what is your end game?

But before jumping into the overall advantages and disadvantages, let’s start with the verticals and how banks are set up: Table Of Contents What is Renewable Energy Investment Banking? Dividend yields are frequently cited for these types of companies as well.

But before delving into the exit opportunities and the long-term outlook, let’s start with the fundamentals: Oil & Gas Investment Banking Defined. Because the risk of searching for new energy sources and experimentally drilling is so high, many E&P firms set up joint ventures to distribute the risk.

In my last post, I looked at the Biden Administration's proposal to increase corporate taxes, to provide funding for an infrastructure bill, and concluded that while there is room for raising corporate taxes, it would be more efficient and fairer to do so by reducing the tax credits and deductions in the code, than by raising the tax rate.

The second was that, starting mid-year in 2020, equity markets and the real economy moved in different directions, with the former rising on the expectations a post-virus future, and the latter languishing, as most of the world continued to operate with significant constraints.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings! Sometimes, less is more!

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Beta & Risk 1. Return on Equity 1.

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdle rates, central to both corporatefinance and investing judgments. Analysts often try to bring company-specific components, i.e,

I start with a framework for thinking about how much cash a business can return to its owners, and then argue that, in the real world, this decision is skewed by inertia and me-tooism. I also look at a clear and discernible shift away from dividends to stock buybacks, especially in the US, and examine both good and bad reasons for this shift.

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. In the table below, we compare the changes in regional market capitalizations (in $ millions) over time.

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content