This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Accurately measuring sustainability ROI can be challenging: corporate sustainability teams should start the process by aligning their language with that of the corporatefinance function. Discussions on the value of sustainability will continue, making it essential for companies to measure sustainability ROI.

Corporatefinance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. In my view, corporatefinance jobs are not ideal “stepping stone roles.”

Kothari is the Gordon Y Billard Professor of Accounting and Finance at MIT Sloan School of Management; and Parth Venkat is an Assistant Professor of Finance at the University of Alabama Culverhouse College of Business. This post is based on their recent paper.

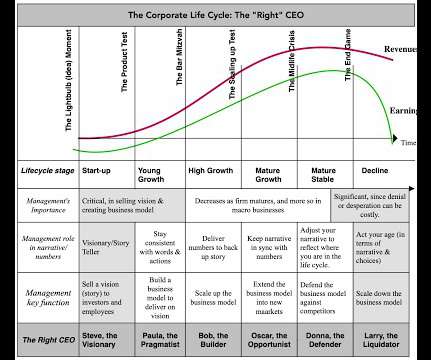

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

Large, stable corporations almost never cut dividends as a strategic choice. Instead, they reduce dividends only when they have low earnings or when challenging economic conditions force their hand.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

The six classes that I prepped for in those two years ranged from banking to investments to corporatefinance, and while I have never worked harder, much of what I teach today came out of those classes. In 1984, I moved on to the University of California at Berkeley, as a visiting lecturer, teaching anything that needed to be taught.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

On January 31, 2024, the company announced that it would clash its quarterly dividend from 4.17 With high interest rates, New York City rent control policies, and changing demand for commercial real estate in New York City, investors are concerned about the bank's future performance. 05, a 70 percent cut.

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online. The place to start is with accounting.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Dividends and Potential Dividends (FCFE) 1. Dividend yield & payout 3.

Access to finance was a huge concern at the start of the pandemic [in 2020] as thoughts turned to the global financial crisis and a potential repeat of bank insolvency,” notes Kristen Roberts, partner and head of the London corporate debt practice at HSF. “So It’s a predicament that started to emerge as far back as 2018. Now it’s 13%.

Within corporatefinance, the agency problem is considered as the conflict of interest between the company’s managers and its stockholders. A secondary conflict is that managers want to re-invest profits in the business, while shareholders may prefer more dividends paid out. Definition of the Agency Problem.

That said, it is my experience with markets that has also made me skeptical about the over selling of both notions, since we have an entire branch of finance (behavioral finance/economics) that has developed to explain how more data does not always lead to better decisions and why crowds can often be collectively wrong.

As a capital allocation decision, share buybacks intersect all three of the main corporatefinance activities of investing, financing, and dividends [1]. Buybacks for Financing A company can alter the debt-to-equity ratio of its capital structure by issuing debt and/or buying back shares.

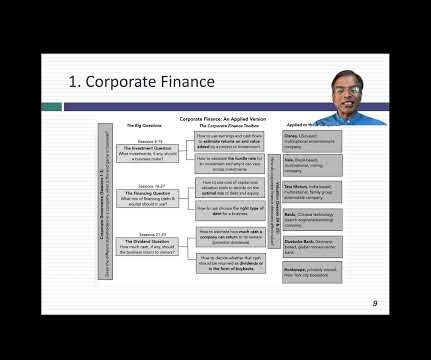

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

Other corporate distributions that have a similar effect on ownership are cash financed acquisitions and going private transactions. Our article formalizes these insights, showing how fund fees, capital gains returns, dividend and capital gains distributions, and balance sheet effects shape institutional growth.

CorporateFinance : The role of the equity risk premium in determining the expected return on a stock makes it a key input in corporatefinance, as well, because that expected return becomes the company's cost of equity.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. The second is that in my line of work, which is corporatefinance and valuation, the numbers I need lie in micro or company-level data, not in the macro space. Dividend Payout & Yield 1. Return on Equity 1.

As we showed in the text, dividends and stock repurchases affect a company and investors in much the same way. The tax may push companies toward dividends, although since the new tax wouldn't take effect until 2023, analysts are expecting large repurchases to be completed by the end of 2022.

In the four decades that I have been teaching finance, I have always started my discussion of risk with a Chinese symbols for crisis, as a combination of danger plus opportunity: Over the decades, though, I have been corrected dozens of times on how the symbols should be written, with each correction being challenged by a new reader.

Traditionally, the sector was viewed as a defensive play for investors who wanted stable dividends and no drama. Companies tend to offer high, stable dividend yields, and they finance their massive capital expenditures primarily with debt , with the highest leverage ratios of any industry outside of financial institutions.

Your answer to that question will determine not just how you approach running the business, but also the details of how you pick investments, choose a financing mix and decide how much to return to shareholders, as dividend or buybacks.

Integrated Oil & Gas can also work, but at the large banks, you’ll mostly advise huge corporations on prospective asset deals and the occasional financing. Finally, these companies are so big and geopolitically sensitive that significant corporate-level M&A deals are rare. meaning there are few sell-side M&A targets.

Determining a company’s “Cost of Capital” is vital in corporatefinance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. These costs are then combined into a “weighted average” which represents the overall cost of financing a business.

Determining a company’s “Cost of Capital” is vital in corporatefinance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. These costs are then combined into a “weighted average” which represents the overall cost of financing a business.

Determining a company’s “Cost of Capital” is vital in corporatefinance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. These costs are then combined into a “weighted average” which represents the overall cost of financing a business.

trillion to buy back their shares, which is significantly more than these firms spent on dividend payments to their shareholders (Lazonick, Sakinç, and Hopkins, 2020). We, like many who recently studied finance and accounting, consider a firm’s CSR ratings as a sign of commitment to ethical behavior. Accounting & Finance.

These pre-MBA programs are the most prominent in consulting , finance, and technology , which makes sense since most MBA students target these industries. We’ll return to this point later, but in finance, it’s more common to do a pre-MBA internship at a small VC/PE firm or boutique bank rather than a bulge bracket bank.

In the textbook, we discussed how buybacks have a tax advantage over dividends because it results in a lower effective tax rate for shareholders. A new law being proposed in the Senate would levy a 2 percent excise tax on all funds used for share buybacks.

Of course, you will never receive a dividend and have no say in the operations of the Packers. The Green Bay Packers are offering 300,000 shares of stock at a price of $300 per share.There are currently a little over 5 million shares of the Packers outstanding.

Finally, many renewable energy debt deals take place within Project Finance teams at banks – but Project Finance and corporatefinance are very different ! The same criteria as always apply: High grades, a good university or business school, previous finance internships, and a good amount of networking and interview prep.

On November 21, 2023, the staff of the Securities and Exchange Commission’s (SEC’s) Division of CorporationFinance issued eight new Compliance & Disclosure Interpretations (C&DIs), and revised two previously issued C&DIs, relating to the final pay-versus-performance (PVP) disclosure rules adopted last year. Answer: Yes.

For simplicity, I am ignoring the interest, dividends, borrowing costs, and other fees, but this example is the general idea with convertible arbitrage. Convertible Securities: A Complete Guide to Investment and CorporateFinancing Strategies. billion, up from $4.7 The increased volatility is the key.

That would have left you lagging the 181% price appreciation that you would have earned on the S&P 500 during the period, and even more so, if you consider the fact that you would have earned no dividends on Facebook, while generating about a 2% dividend yield, every year on the index.

A Life Cycle View If you have been reading my posts for a while, you know that I find the corporate life cycle a useful device in explaining everything from what companies should focus on, in corporatefinance, to the balance between stories and numbers, when investor value companies.

The staff of the Securities and Exchange Commission’s (SEC’s) Division of CorporateFinance recently issued guidance to address open questions related to the final pay-versus-performance (PVP) disclosure rules adopted in 2022. However, it is not clear whether or how this informal guidance from 2014 applies to the PVP rules.

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. If you use it at their jobs as corporatefinance or equity analysts, I am glad to take some of that burden off you, and I hope that you find more enjoyable uses for the time you save.

In this post, I look at risk, a central theme in finance and investing, but one that is surprisingly misunderstood and misconstrued. I do believe that, in finance, we have significant advances in understanding what risk, I also think that as a discipline, finance has missed the mark on risk, in three ways. What is risk?

The Taxation of Investment Income In much of the world, income from investments (interest, dividends) is treated differently than earned income (salary, wages), by the tax code, and the reasons for the divergence are both practical and political: 1.

The oil giant cut its dividend to balance shareholder payouts with rising capital investments amid lower crude prices and evolving market conditions. Saudi Arabian Oil, better known as Aramco, is recalibrating its dividend strategy as it navigates weaker oil prices and rising capital investment demands. billion from $121.3

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Dividends and Potential Dividends (FCFE) 1.

I also look at a clear and discernible shift away from dividends to stock buybacks, especially in the US, and examine both good and bad reasons for this shift. Some of that cash will be held back in the company as a cash balance, but the balance can be returned either as dividends or in buybacks.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content