This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Corporatefinance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. In my view, corporatefinance jobs are not ideal “stepping stone roles.”

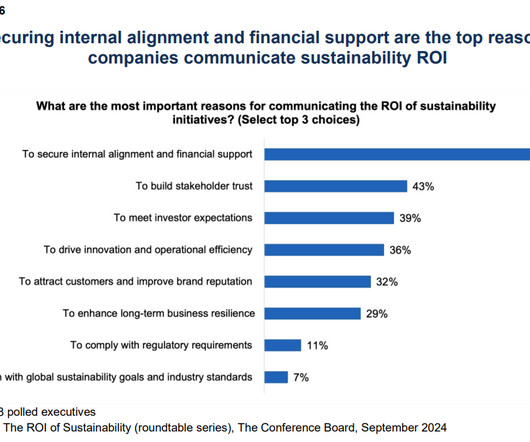

Accurately measuring sustainability ROI can be challenging: corporate sustainability teams should start the process by aligning their language with that of the corporatefinance function. Discussions on the value of sustainability will continue, making it essential for companies to measure sustainability ROI.

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

Kothari is the Gordon Y Billard Professor of Accounting and Finance at MIT Sloan School of Management; and Parth Venkat is an Assistant Professor of Finance at the University of Alabama Culverhouse College of Business. Posted by Nicholas Guest (Cornell University), S.P.

Speaker: Wayne Spivak - President and Chief Financial Officer of SBA * Consulting LTD, Industry Writer, and Public Speaker

Join Wayne Spivak, experienced CFO and corporatefinance expert, for an insightful discussion on managing cash flow and company profitability. Attendees will walk away with an in-depth understanding of the following: What is accounting?

These developments have caused much discussion, with some commentators again seeing a fundamental shift in the relevance of public and private markets for corporatefinance and alarmed regulators. In particular, financial history shows various boom-and-bust periods in private market activity (see Kaplan & Strömberg, 2009 ).

I taught six different classes ranging from a corporatefinance class to undergraduates to a central banking for executive MBAs, and while I spent almost all of my time struggling to stay ahead of my students, with the material, it set me on a pathway to being a generalist.

Today, the Staff in the Division of CorporationFinance at the Securities and Exchange Commission published one new and one revised Compliance and Disclosure Interpretation (C&DI) under Regulation 13D-G. This post is based on a Sullivan & Cromwell memorandum by Ms. Dreisiger, Mr. Hearn, Ms. Rodgin Cohen , Robert W.

In The Credit Markets Go Dark , we describe how private credit funds are reshaping corporate governance and corporatefinance and offer new data capturing its meteoric rise. trillion in 2023.

The SEC’s Director of CorporationFinance, Erik Gerding, recently issued two statements regarding a public company’s disclosure obligations in response to a cybersecurity incident. Kurt von Moltke are Partners at Jenner & Block LLP. This post is based on a Jenner & Block memorandum by Ms.

Assess the Impact of SEC Staff Comments The staff of the Disclosure Review Program (DRP) in the SEC’s Division of CorporationFinance has remained quite active. This post is based on their Skadden memorandum. 1] This uptick in comment letters reversed the downward trend of recent years.

There is an extensive body of studies that documents that corporate insiders with access to insider information are able to earn abnormal returns by trading their firms shares. This post is based on their recent paper.

With Staff Legal Bulletin 14L, the SEC Division of CorporationFinance Staff realigned its approach for determining whether a proposal relates to “ordinary business” with a previous standard providing an exception for certain proposals raising significant social policy issues.

The FRP CorporateFinance debt advisory team has supported pan-European specialist pharmaceutical business, Kelso Pharma (Kelso), on its acquisition of Alturix, a UK pharmaceutical company specialising in developing and commercialising originator and niche branded generics.

Posted by Michael Eisenband, FTI Consulting, on Monday, July 29, 2024 Editor's Note: Michael Eisenband is Global Co-Leader of CorporateFinance & Restructuring at FTI Consulting. This post is based on his FTI Consulting memorandum.

Posted by Jillian Grennan (UC Berkeley), on Wednesday, March 13, 2024 Editor's Note: Jillian Grennan is an Associate Adjunct Professor of Finance and Sustainability at the University of California, Berkeley Haas School of Business. Harvey , and Shivaram Rajgopal.

This “meme surge” phenomenon, particularly the dramatic shift in shareholder base away from institutional ownership, presents a unique opportunity for analysts and scholars to (re)evaluate the current understanding of corporatefinance and governance.

This proxy season, companies saw more shareholder proposals than in the past, a change that has been widely attributed to actions by the SEC and its Division of CorporationFinance that had the effect of making exclusion of shareholder proposals—particularly proposals related to environmental and social issues—more of a challenge for companies.

Among other actions, during February 2021, shortly after taking office, then-Acting Chair Allison Herren Lee issued a statement directing the SEC’s Division of CorporationFinance to enhance its focus on climate-related disclosure in public company filings.

Following a tumultuous 2022 shareholder proposal no-action letter season, the 2023 season contained fewer surprises from the Staff of the Division of CorporationFinance (Staff) of the Securities and Exchange Commission (SEC).

It is no exaggeration to say that over its roughly forty-year history, private equity has revolutionized both corporatefinance and corporate governance. This post is based on their article, forthcoming in the Washington University Law Review.

With the accelerating transition away from fossil fuels, awareness of the role of minerals critical to the production of clean energy (including cobalt, copper, lithium, nickel, and rare earth elements) has increased.

Professor of Law and Economics at Harvard Law School and former General Counsel and Acting Director of the SEC’s Division of CorporationFinance; Gerald Davis, Gilbert and Ruth Whitaker Professor of Business Administration at the University of Michigan Ross School of Business; Joseph A. Grundfest, William A.

He has three decades of experience in capital markets, corporatefinance, and valuations. Between 2010 and 2017, Nicolas was a corporatefinance advisor and Investor Relations officer for corporate clients in several industries, including Renewable Energy.

This post is based on a recent article by Professor Yang, Manish Jha , Assistant Professor of Finance at Georgia State University; Jialin Qian, PhD Candidate at Georgia State University; and Michael Weber , Associate Professor of Finance at the University of Chicago. Understanding corporate policies is central to corporatefinance.

On Wednesday, by 3-1 vote, the SEC approved proposed rules aimed at enhancing and standardizing disclosures made by public companies regarding cybersecurity risk management, strategy, governance and incident reporting, [1] reflecting the third rulemaking project the Commission has proposed in connection with cybersecurity in the past year. [2]

In May, the SEC’s Division of CorporationFinance issued an illustrative letter with sample comments the Division may issue to registrants, reinforcing disclosure obligations related to matters that directly or indirectly impact a company’s business.

In November 2021, the staff of the Division of CorporationFinance (the “Staff”) of the SEC issued Staff Legal Bulletin No. Pinedo , and David A. Proxy Voting Matters SHAREHOLDER PROPOSALS Shareholder Proposals in the 2023 Proxy Season. 14L (“SLB 14L”), [1] rescinding Staff Legal Bulletins Nos. 14I, 14J and 14K.

The former director of the SEC Division of CorporationFinance, Bill Hinman, suggested engagement between shareholders and management might improve if the SEC could “get out of the way.”. Moreover, even the SEC has debated whether its involvement in this process adds value. more…).

Arnold Daum Chair in CorporateFinance and Law and the Associate Dean for Faculty Development at the University of Iowa College of Law. This post is based on his recent paper forthcoming in the Journal of Corporation Law and is part of the Delaware law series ; links to other posts in the series are available here.

Posted by Matthew Fust, on Wednesday, July 13, 2022 Editor's Note: Matthew Fust serves as a board member for several publicly traded and venture-backed biopharmaceutical companies and is a corporatefinance and strategy advisor in the life sciences industry. This post is based on an NACD BoardTalk publication.

When a company intends to exclude a shareholder proposal from its proxy materials, the company typically requests no-action relief from the Staff of the SEC’s Division of CorporationFinance (Staff).

Posted by Burcin Yurtoglu (WHU Otto Beisheim School of Management), on Tuesday, April 19, 2022 Editor's Note: Burcin Yurtoglu is Chair of CorporateFinance at WHU Otto Beisheim School of Management. This post is based on a recent paper authored by Prof. Yurtoglu; Bernard S. Black , Nicholas D.

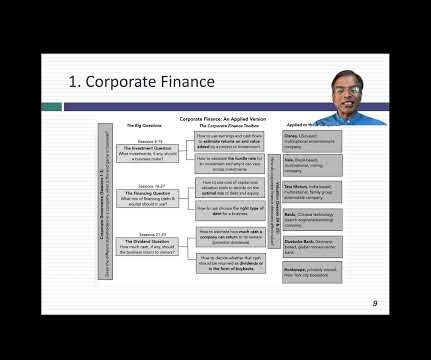

The six classes that I prepped for in those two years ranged from banking to investments to corporatefinance, and while I have never worked harder, much of what I teach today came out of those classes. I describe my corporatefinance class as an applied, big-picture class.

Berger (University of Chicago), Wei Cai (Columbia University), and Lin Qiu (Purdue University) , on Monday, June 26, 2023 Tags: Board culture , Board of Directors , CEOs , Corporate culture , dei , Diversity Demonstrating Pay and Performance Alignment Posted by Mike Kesner, Linda Pappas and Ed Sim, Pay Governance LLC, on Monday, June 26, 2023 Tags: (..)

He has three decades of experience in capital markets, corporatefinance, and valuations. Between 2010 and 2017, Nicolas was a corporatefinance advisor and Investor Relations officer for corporate clients in several industries, including Renewable Energy.

In 2011, “the Division of CorporationFinance issued interpretive guidance providing [its] views concerning operating companies’ disclosure obligations relating to cybersecurity.” [1] 3] We do not need additional regulations.

Prior work interprets this finding as prima facie evidence of a causal link between shareholder litigation rights and corporate governance. A fast-growing stream of studies in corporatefinance and accounting relies on the adoption of UD laws to identify cause-and-effect links between management entrenchment and various firm outcomes.

On May 21, 2024, Erik Gerding, director of the SEC’s Division of CorporateFinance, issued a statement to clarify that public companies are only required to disclose a cybersecurity incident under Item 1.05 of Form 8-K if the incident is “determined by the registrant to be material.”

Prior to joining PIF, Doug was a CorporateFinance Partner and Global Valuation Leader for KPMG. Hakim has 14 years of experience in valuation and corporatefinance, and he specializes in the valuation of illiquid securities, businesses and intangible assets.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content