This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

nancial markets, but also ties their health to that of other ?nancial We do so by focusing on bank executives’ equity portfolio (i.e., stock and option) “vega,” which captures the sensitivity of their equity portfolio’s value to their firm’s stock return volatility. Wang (discussed on the Forum here ). Banks’ role in ?nancial

Definition of Optimal CapitalStructure. The optimal capitalstructure of a firm is the right combination of equity and debt financing. It allows the firm to have a minimum cost of capital while having the maximum market value. The lesser the cost of capital, the more the market value of the company.

The following chart from GF Data shows the average capitalstructure over the past 5 years for middle market business acquisitions. Over that time equity contributions have varied only slightly over that time, in the range of 46% to 49%. Overall there was a slight rise during COVID, but nothing major.

Corporate finance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. What Are Corporate Finance Jobs? not banks or investment firms).

Understanding your company’s capitalstructure is essential for maximizing its value and ensuring long-term stability. Whether you're deciding how much debt to take on or how to manage equity financing, the right mix can lower your cost of capital and boost growth. Why capitalstructure matters for business performance.

Guest post from an Equidam partner: Bianca Iulia Simion , Marketing Lead at SeedBlink As the world of startups continues to evolve and mature, navigating the intricacies of equity management has emerged as a critical aspect of successful entrepreneurship. This leads to confusion and potential conflict during fundraising rounds.

A few weeks ago, we observed private equity investors learning a lesson about liquidity risk, which family shareholders have always known. A couple of weeks ago, the Wall Street Journal noted that — amid a sluggish M&A market — PE-backed companies were increasingly turning to… Source

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded common… Source

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded common… Source

The theory suggests that a company’s capitalstructure and the average cost of capital does not have an impact on its overall value. . It doesn’t matter whether the company raises capital by borrowing money, issuing new shares, or by reinvesting profits in daily operations. Definition of the Modigliani-Miller Theorem.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded common.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded.

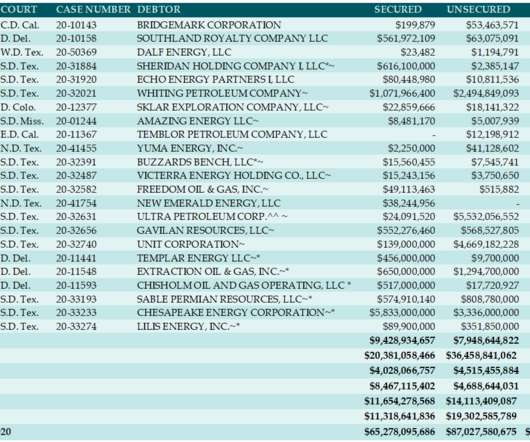

The challenges and complexities of energy markets make reorganization plans hard to properly formulate. The challenge for counsel and financial advisors has to with the often-severe price volatility common to oil and gas markets. Why is Energy Different? We have discussed this in a separate article recently published on our site.

Mercer Capital has its finger on the pulse of the minerals market. Due to a variety of corporate structures (including master limited partnerships and Up-Cs) and complex capitalstructures (including preferred equity and non-traded common… Source

It involves the partial sale of the company to private equity firms or venture capitalists. Recapitalization helps stabilize the capitalstructure of a company by restructuring its equity and debt. They gain both capital resources and access to professional strategic counsel to maximize business value.

Entrepreneurial business owners can gain a substantial competitive edge in the lower middle market by recognizing the benefits of balance sheet restructuring, particularly when private equity collaborates as a partner for a defined period of time or a family office serves as your evergreen business partner.

Weight average cost of capital (WACC) is a calculation of a firm’s cost of capital which includes all sources of capital such as common stocks, preferred stocks, and bonds. A firm uses a mix of equity and debt to minimize the cost of capital. Difference Between Cost Method and Equity Method.

If you’re thinking about exit opportunities and can’t decide between private equity and hedge funds , activist hedge funds might be your solution. Similar to private equity firms, they operate on longer time frames, influence companies’ operations and finances, and might catalyze major changes, such as spin-offs or acquisitions.

Ask anyone interested in distressed debt hedge funds for “the pitch,” and they’ll probably mention one of the following: “It’s like long/short equity or credit , but more interesting!” Distressed investing offers equity-like returns with lower risk.” Distressed assets offer non-correlated returns, similar to global macro.”

Mergers and acquisitions (M&A) have long been strategic maneuvers for companies seeking growth, market dominance, or increased efficiency. The risk of default becomes a looming concern, especially if market conditions turn unfavorable.

Traditional financing methods may seem risky or unfeasible when markets are volatile or unpredictable. Mezzanine Financing: Mezzanine financing sits between equity and debt in the capitalstructure and is often used to fund M&A transactions.

describe the relationship between the capitalstructure of the firm and its value. . It is often used as a benchmark for evaluating the financial decisions of firms and has been influential in shaping how firms approach financing and capitalstructure. . . Suppose also the weighted average cost of capital is 10%.

Since the global financial crisis of 2007-2008, the corporate finance markets have been dramatically transformed. One of the major shifts in corporate finance is the significant rise of private capital financing (e.g., private credit, private equity, venture capital). trillion [1] and projected to grow to $2.3

And it values the company today based on the present value of its dividends and that potential future value (either the stock price or the Equity Value via the Terminal Value calculation). And Equity Real Estate Investment Trusts (REITs) must distribute almost all their Net Income, so the DDM can work well in REIT valuations.

Then I show how the market has developed a new corporate structure designed to solve these problems, which relies on a subtler form of insulation. The second is a motivation problem : Managers can’t give their employees the right incentives to bring the technology to market. But there’s a catch.

Upon closing, the combined company is expected to trade on the Nasdaq CapitalMarket under the symbol "SNWV". · The combined company expects to receive approximately $13.0 million from the SPAC sponsor converting a loan into equity on the same terms as the PIPE. wound care market. Approximately $8.5

What would otherwise be negotiations between insiders on both sides (the board of directors, who are appointed by equity, and equity holders) is transformed into an unconflicted negotiation when the bankruptcy directors are delegated authority by the board of directors.

Different types of discount rates such as risk-free rate, cost of equity, or cost of debt, are used contextually in financial analysis. Cost of Equity: The cost of equity represents the return required by equity investors to compensate them for the risk of owning a company’s shares.

Some key questions asked and argued were: Of relevance to private company investors: what is the standard of review appropriate when there is no market evidence for an appraisal fight, and the Court is forced to decide between a ‘battle of the experts’?

The buyer (the “sponsor”) raises debt and equity to acquire the target. It borrows the majority of the purchase price and contributes proportionately small equity investment. The LBO ratios can go to 90% of debt and 10% of equity. A private equity firm aims a target return of around 20 – 25% (WallStreetMojo, 2018).

Determining a company’s “Cost of Capital” is vital in corporate finance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. The resulting WACC represents the average cost of all the types of capital a company uses to finance its operations.

Determining a company’s “Cost of Capital” is vital in corporate finance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. The resulting WACC represents the average cost of all the types of capital a company uses to finance its operations.

Determining a company’s “Cost of Capital” is vital in corporate finance and valuation, and the Weighted Average Cost of Capital (WACC) provides a specific way of doing so. The resulting WACC represents the average cost of all the types of capital a company uses to finance its operations.

Adjusted Net Book Value Adjusted Net Book Value is the Book Value of a business that has been adjusted to reflect the current market value of the assets and liabilities of a company. what is the value of an asset as listed on the company’s accounting records), or the fair market value of a specific asset or group of assets.

A company executes a share buyback when it pays out cash from its balance sheet to purchase its previously issued shares in the stock market or directly from shareholders. This usually happens when a company is making a deliberate and significant change to its capitalstructure.

Different methods are used, like looking at market prices, predicting future profits, and evaluating assets. Some techniques include comparing companies in the market, estimating future cash flows, and assessing the value of tangible assets. to its market value.

Event-Driven Hedge Funds Definition: Event-driven hedge funds bet on specific corporate actions, such as M&A deals, divestitures, spin-offs, bankruptcies, and business reorganizations, and they profit based on changes in the value of a company’s debt or equity after the action.

This can include valuation comparables , industry data, or market insights. Here’s how: During the Prepare phase, REAG’s expertise in capital stack structuring becomes invaluable for CEPAs and their clients. Sprint 2: Evaluate financing needs, debt capacity, equity requirements.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content