This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Correctly calculating adjusted EBITDA is essential in an M&A transaction, and all parties must be familiar with the adjustments. EBITDA is used to evaluate a company’s profitability of its core operations by removing items dependent on capitalstructure, such as interest,

Common metrics include SDE, EBITDA, and Revenue. For physical therapy valuation multiples, the business appraiser calculates the value of a physical therapy practice by using the practice’s SDE, EBITDA, and REV. Common Physical Therapy Valuation Multiples Below we discuss SDE, EBITDA, and REV multiples for a physical therapy practice.

Stephen Carey, Senior Vice President and Chief Financial Officer of ANI said, "ANI's new capitalstructure provides us significant financial flexibility to support the integration of Alimera and continue investing in organic growth initiatives while also significantly reducing our interest expense and increasing cash flow." (1)

This diagram highlights REV, SDE, and EBITDA multiples. EBITDA Multiples for an Apparel Wholesale Company Average EBITDA Multiple range: 3.09x – 4.51x The average EBITDA multiples for apparel wholesalers range between 3.09x – 4.51x. Apply this multiple to EBITDA to determine an implied value of the business.

Below we show SDE, EBITDA, and REV valuation multiples for iron & steel manufacturers. Many small businesses such as iron & steel manufacturers transact on cash flow multiples such as EBITDA and SDE. This is because the EBITDA and SDE multiple consider expenses that impact cash flow. 240,000 X 2.87x= $688,800.

Below, we discuss SDE , EBITDA, and REV multiples for a bar or nightclub. EBITDA Multiples for a Bar or Nightclub Average EBITDA Multiple range: 3.00x – 5.07x According to Peak’s data, bars and nightclubs sell between an average EBITDA multiple range of 3.00x – 5.07x. Each bar and nightclub is unique.

The diagram shows REV, SDE , and EBITDA multiples for primary care physicians. A valuation multiple is a ratio that compares the value of the business to a factor such as earnings, revenue, or EBITDA. To determine what a physician’s office is worth multiply EBITDA by the appropriate EBITDA multiple.

This diagram shows REV, SDE, and EBITDA multiples for paint wholesalers. EBITDA Multiples for a Paint Wholesaler Average EBITDA Multiple range: 3.20x – 4.16x The average EBITDA multiples for a paint wholesaler range between 3.20x – 4.16x. It transacts at an EBITDA multiple of 3.66x.

The visual shows REV, SDE, and EBITDA multiples for chiropractic practices. EBITDA Multiples for Chiropractic Clinics Average EBITDA Multiple range: 2.86x – 3.83x According to our data, the average EBITDA multiple for chiropractic clinics ranges from 2.86x – 3.83x. It transacts at a 3.39x EBITDA multiple.

Below, we discuss SDE, EBITDA, and REV multiples for accounting firms. EBITDA Multiples for an Accounting Firm Average EBITDA Multiple Range: 2.99x – 4.45x The average EBITDA multiples for accounting firms range between 2.99x – 4.45x. Apply this multiple to EBITDA to determine an implied value of the business.

The visual shows REV, SDE, and EBITDA multiples for footwear wholesalers. EBITDA Multiples for Footwear Wholesale Average EBITDA Multiple: 4.74x Using private transaction data, the average EBITDA multiple for a footwear wholesaler is 4.74x. It transacts at a 4.70x EBITDA multiple. The calculation is as follows.

This includes SDE, REV, and EBITDA multiples for an RV dealership. SDE and EBITDA multiples – are cash flow multiples. EBITDA Multiples for RV Dealerships. Average EBITDA Multiple range: 2.32x – 3.69x. In our data, the average EBITDA multiples for RV dealerships fall between 2.32x – 3.69x.

EBITDA Multiples for a FedEx Route Average EBITDA Multiple range: 3.60x – 4.06x The average EBITDA multiples for a FedEx route range from 3.60x – 4.06x. Apply this multiple to EBITDA to determine an implied value of the business. It transacts at an EBITDA multiple of 3.83x. See the calculation below.

The following sections highlight SDE, EBITDA, and REV multiples for tax preparation businesses. EBITDA Multiples for Tax Preparers Average EBITDA Multiple range: 3.42x – 4.51x The average EBITDA multiples for tax preparation businesses range between 3.42x – 4.51x. It transacts at an EBITDA multiple of 4.04x.

This includes REV, EBITDA, and SDE multiples for a tire dealership. Cash flow multiples include SDE and EBITDA multiples. EBITDA Multiples for Tire Dealerships. Average EBITDA Multiple range: 2.68x – 4.89x. To calculate the value of the tire dealership, apply the multiple to EBITDA. 268,000 X 2.56x= $686,080.

This includes SDE, REV, and EBITDA multiples for shoe & footwear manufacturing. EBITDA Multiples for Shoe & Footwear Manufacturing. Average EBITDA Multiple range: 4.08x – 4.76x. On average, according to Peak’s data the EBITDA multiples for a shoe manufacturing business range between 4.08x – 4.76x.

This includes SDE, EBITDA, and REV multiples for metalworking machinery manufacturing. Cash flow multiples include the SDE multiple and EBITDA multiple. EBITDA Multiples for Metalworking Machinery Manufacturing. Average EBITDA Multiple range: 3.35x – 4.12x. EBITDA X Multiple = Value of the Business.

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

The ratio used might be EV/EBITDA, EV/Sales, P/E or another, depending on the valuation performed and the type of business being valued. So another major assumption when adopting this method, is that the type of ratio chosen as the comparison point, such as P/E or EV/EBITDA should be similar across similar firms. .

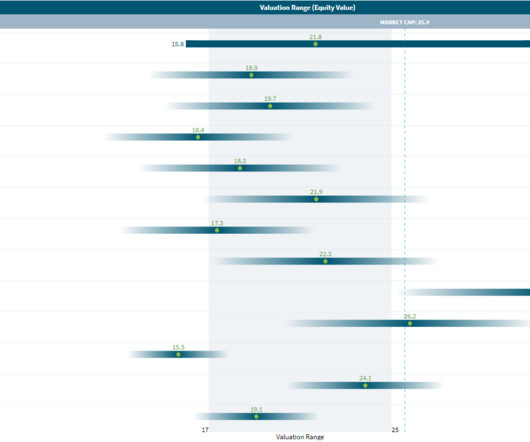

2022 saw a robust cash and capitalstructure with a staggering USD 967 million adjusted EBITDA in Q4, up by 14% from the previous year. billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. The Discounted Cash Flow analysis produced a value of USD 21.8 billion using a WACC of 10%.

The visual shows REV, SDE, and EBITDA multiples for dry cleaning businesses. EBITDA Multiples for Dry Cleaners Average EBITDA Multiples: 2.49x – 4.14x According to private transaction data, the average EBITDA multiples for a dry cleaning business are between 2.49x – 4.14x. Know that these numbers are just a guide.

As per Macabacus (2018), the typical credit statistics can be (those can change with market conditions): Total Debt / EBITDA 4.5x -5.5. Senior Bank Debt / EBITDA 3.0x. CapitalStructure of an LBO.

Its financial profile now looks like this: Its Debt / EBITDA is now 10x, its EBITDA / Interest has fallen below 1x, the Secured Debt is trading at 90% of its face value, and the Unsecured Debt is down to 60%. A few years later, the company’s industry declined, and it was slow to cut costs and enter new markets.

Discretionary cash flow will initially be directed at strengthening the Company's financial position, with Enerflex targeting its bank-adjusted net debt to EBITDA ratio to be below 2.5 CAPITALSTRUCTURE. times within 12 to 18 months.

In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies. These cash flows typically include operating income, tax payments, and changes in working capital and capital expenditures.

In the CCA method, valuation multiples such as P/E ratio, EV/Revenue ratio, and EV/EBITDA ratio, provide benchmarks for estimating value by comparing financial metrics to publicly traded companies. These cash flows typically include operating income, tax payments, and changes in working capital and capital expenditures.

Even if you pick the right company, though, the DDM is more difficult to set up and use than a standard DCF because it requires more assumptions and knowledge of the company’s capitalstructure. Dividend Discount Model, Part 3: CapitalStructure Projections You don’t want to “rock the boat” too much with Cash and Debt in this model.

million Adjusted EBITDA of $237.6 million Adjusted EBITDA of $68.2 million Adjusted EBITDA of $237.6 million Adjusted EBITDA of $68.2 We will work quickly to realize synergies to drive improved Adjusted EBITDA margins and cash flows as we focus on investing in innovation and reducing our overall net leverage."

million of Adjusted EBITDA 2 in 2023. The proceeds from the sale of our Tower business will provide Shentel with additional growth capital to support the planned expansion of our Glo Fiber line of business to approximately 600,000 homes and business passings by the end of 2026. million in revenue, $9.5

This method is common in industries where valuations are commonly expressed as a multiple of Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) or Earnings Before Interest and Taxes (EBIT). It indicates how much an investor is willing to pay for a company’s operating earnings (EBITDA).

These ratios, like the EBITDA multiple, compare a company’s financial performance (EBITDA, revenue, etc.) Analysts use financial metrics and multiples such as Price to Earnings (P/E), Enterprise Value to EBITDA (EV/EBITDA), and Price to Book (P/B) ratios and apply them to the target company’s financials.

Regulation – This affects everything from firms’ capitalstructures to their revenue, margins, and favored fuel sources, so the impact could be minimal or very large in either direction, depending on what the government changes. It’s safe to say that they have encouraged more deal activity. Power & Utilities Overview by Vertical.

.'s (the "Company's") dividend expectations and its operations, its facilities and its financial results, statements regarding the likelihood, terms, timing and/or consummation of the transactions described above, the potential benefits, opportunities, and results with respect to the transactions, including the Company's future relationship (..)

Post management expects the Pet Food Business to generate substantial incremental free cash flow, complementing Post's cash generation-focused business model and preserving Post's flexibility to manage its capitalstructure. * Additional Information Barclays Capital Inc.

Practitioners assume the business is sold as a multiple of some financial metric like EBITDA, based on what they can see today for other businesses that were sold, and what these comparable trading multiples are. . EV/EBITDA Multiple. So here is the EBITDA and FCF year on year for our entire 5-year forecast period: Period.

The successful closing of this strategic acquisition not only approximately doubles SMGI's annual revenue and increase its adjusted EBITDA, but also brings operational and revenue diversification, strengthens the Company's balance sheet and adds exceptional expertise to its leadership team. million (including $2.5

EBITDA multiple , matching its own. EBITDA since it’s only growing at 2-3% per year vs. 5-10% per year for Jacobs. CapitalStructure Trades – Or you could focus on Jacobs’ ~$4 billion in debt and long or short some of their bonds (or use credit default swaps) if you believe its credit rating will change once the deal takes place.

Concept of notional interest : It is proposed to introduce notional interest, the idea of which is to allow the deduction during 10 consecutive years of this "synthetic" interest, within the famous limit of 30% of the company's EBITDA. The CMU aims to better balance bank financing against capital market financing.

SEPA is a strong, value-add partner, and this transaction will allow SANUWAVE to simplify its capitalstructure and gain a listing on the Nasdaq Capital Market while funding the Company for the exciting growth ahead.

When comparing financial metrics, it is advisable to focus on those that directly impact valuation multiples commonly used in CCAs, such as EV/Sales, EV/EBITDA, P/E, and EV/EBIT. These metrics help ensure that the chosen peers have similar financial performance, which is crucial for meaningful valuation comparisons.

27] Unitranche Debt The other trend in private credit financing arrangements is the rise of single-tranche or unitranche loans, which eliminate the complex capitalstructure of first- and second-lien debt in favor of a single facility. [28] 18] maximum expenditure on capital assets for a given period. [19]

It is typically the highest risk/highest potential return portion of a company’s capitalstructure. EBITDAEBITDA refers to Earnings Before deducting Interest, Taxes, Depreciation, and Amortization costs, and is often used by buyers and sellers as a proxy for operating cash flow in a business (i.e.,

If Midstream companies want to grow beyond the fee increases written into their contracts and possible volume growth, they need to spend on Growth CapEx and estimate the incremental EBITDA from that spending: Further adding to the complexity is the GP (General Partner) / LP (Limited Partner) structure used at most MLPs.

One simplistic proxy for this cash generating capacity is EBITDA as a percent of enterprise value (EV), with higher (lower) values indicating greater (lesser) cash flow generating capacity. Debt to EBITDA, Interest Coverage Ratios If debt to capital is not a good measure for judging over or under leverage, what is?

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content