This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

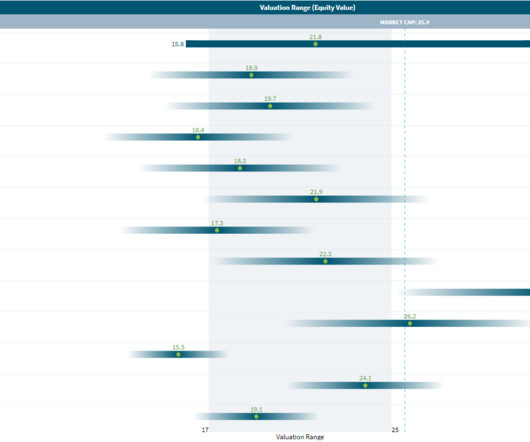

2022 saw a robust cash and capitalstructure with a staggering USD 967 million adjusted EBITDA in Q4, up by 14% from the previous year. billion by applying the observed trading multiples EV/Sales, EV/EBITDA, EV/EBIT and P/E. The Discounted Cash Flow analysis produced a value of USD 21.8 billion using a WACC of 10%.

An example of an enterprise multiple: EV/Sales, EV/EBITDA, EV/EBIT and practically all non-financial multiples (e.g. On the other hand, if we use the P/E multiple (with Earnings being the last line item on the P&L), we have already taken the operating, capital and asset structures of the respective companies into consideration.

An example of an enterprise multiple: EV/Sales, EV/EBITDA, EV/EBIT and practically all non-financial multiples (e.g. On the other hand, if we use the P/E multiple (with Earnings being the last line item on the P&L), we have already taken the operating, capital and asset structures of the respective companies into consideration.

This method is common in industries where valuations are commonly expressed as a multiple of Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) or Earnings Before Interest and Taxes (EBIT). A lower EV/EBIT ratio indicates a potentially better value for investors.

When comparing financial metrics, it is advisable to focus on those that directly impact valuation multiples commonly used in CCAs, such as EV/Sales, EV/EBITDA, P/E, and EV/EBIT. These metrics help ensure that the chosen peers have similar financial performance, which is crucial for meaningful valuation comparisons.

DCF WACC—similar to the above except that it calculates a different WACC in each forecast period based on a changing capitalstructure (D/E) and thus a changing beta in each period. Tax (from tax rate and EBIT). Non-cash working capital. The CapEx, tax, and in this case non-cash working capital, are negative. .

Thus, we start with operating income or earnings before interest and taxes (EBIT) replacing net income. (I The Life Cycle Effect In a corporate life cycle structure, you trace a business from start-up (birth) to the toddler years (very young businesses) through their teenage years into middle and old age.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content