This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The results are similar if you break stocks down based upon price to book ratios or revenue growth rates. The Implied ERP - Start of 2022 I have computed the implied equity riskpremium at the start of every month, since September 2008, and during crisis periods, I compute it every day.

Exacerbating the pain, corporate default spreads rose during the course of 2022: While default spreads rose across ratings classes, the rise was much more pronounced for the lowest ratings classes, part of a bigger story about risk capital that spilled across markets and asset classes.

Relative Risk Measures Before we embark on how to measure relative risk, where there can be substantial disagreement, let me start with a statement on which there should be agreement. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Beta & Risk 1. Equity RiskPremiums 2. Book Value Multiples 3. Working capital needs Thus, I compute pricing multiples based on revenues (EV to Sales, Price to Sales), earnings (PE, PEG), book value (PBV, EV to Invested Capital) or cash flow proxies (EV to EBITDA). Return on Equity 1. Debt Details 1.

In fact, the standard practice that most analysts and investors follow to estimate the risk free rate is to use the government bond rate, with the only variants being whether they use a short term or a long term rate. and the reverse will occur, when risk-free rates drop.

When combined, they can paint a picture of a company that might be cooking its books faster than a chef in a Michelin-starred kitchen. A high M-Score could indicate higher risk, warranting a higher discount rate and thus a lower valuation. It's like adding a riskpremium, but based on hard data rather than gut feeling.

Corporate Bonds: No Shortage of Risk Capital In my last post, I chronicled the movement in the equity riskpremium, i.e. the price of risk in the equity market, during 2021, but the bond market has its own, and more measurable, price of risk in the form of corporate default spreads.

The overriding message in all of this data is that Russia/Ukraine war has unleashed fears in the bond market, and once unleashed that fear has pushed up worries about default and default risk premia across the board.

For example, I have seen it asserted that a stock that trades at less than book value is cheap or that a stock that trades at more than twenty times EBITDA is expensive. I do report on a few market-wide data items especially on riskpremiums for both equity and debt. Price to Book 3. High-Low Price Risk Measure 5.

Consider, for instance, an investor who picks stocks based upon price to book ratios, who finds a stock trading at a price to book ratio of 1.5. buy stocks that trade at less than book value or trade at PEG ratios less than one) for individual stocks.

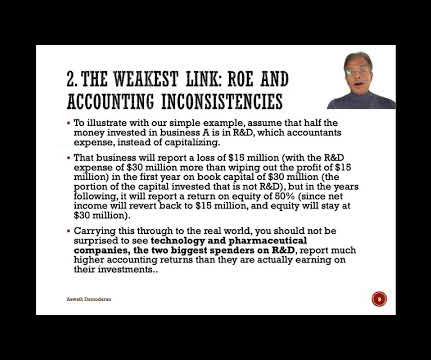

It is to remedy this defect that analysts scale profits to invested capital, with equity and capital variants: In the equity version, you divide net income by book equity to estimate a return on equity, a measure of what equity investors are generating on the capital they have invested in a company.

In my last three posts, I looked at the macro (equity riskpremiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital.

RiskPremiums and Failure Risk : By itself, inflation has no direct effect on equity riskpremiums, but it remains true that higher levels of inflation are associated with more uncertainty about future inflation. Consequently, as inflation increases, equity riskpremiums will tend to increase.

Book a demo here to see how Valutico can help you. Interpreting beta values is crucial for investors to understand an asset’s risk exposure and its relationship with the overall market. Therefore, recalculating beta periodically or when significant events occur is advisable for accurate risk assessment.

The formula implies the return an investor expects from a risk-free investment plus the return from the stock in relation to market volatility. The market riskpremium is calculated from a market rate of return less a risk-free rate. The formula is expressed in the following.

An Optimizing Tool In my second and third data posts for this year, I chronicled the effects of rising interest rates and riskpremiums on costs of equity and capital. Book versus Market : The book debt ratio is built around using the accounting measure of equity, usually shareholder's equity, as the value of equity.

Riskpremiums No effect or even a decrease. Risk premia may rise as inflation increases, because higher inflation is almost always more volatile than low inflation. Riskfree rate will rise.

It needs to incorporate both the project risk and the opportunity cost, typically done using the CAPM method. However, market information required for CAPM, such as beta coefficients and riskpremiums, may not be available for SMEs. Why not book your demo here to find out how Valutico can help you in valuing SMEs.

Insurance industry terminology such as risk, premium, loss, deductibles, coverage limits, and perils are some of the fundamental concepts appraisers must grasp. Different property insurance policies have unique features and limitations.

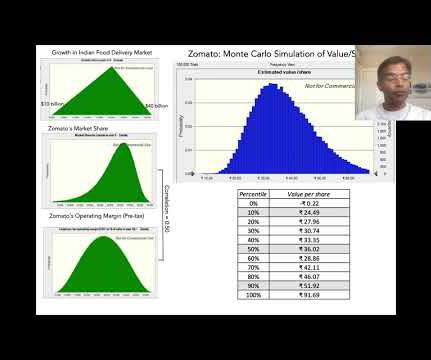

The second is the cost of capital, a number that most valuation classes and books (including mine) belabor to the point of diminishing returns. Finally, dismissing Zomato as an investment, just because it does not make money now, or fails to meet some conventional value tests on pricing (PE, Price to Book), is investing malpractice.

He is a frequent presenter on valuation topics, and is currently a subject matter expert on the Appraisal Foundation’s working group preparing a Valuation Advisory on the Company-Specific RiskPremium. He specializes in the valuations of business enterprises and their intangible assets.

Rf = Risk-free Rate. Rm – Rf) = Equity Market RiskPremium. Cp = Cost of Equity Premium. Try booking a demo , if this applies to you. The details of how the CAPM works is beyond the scope of this article but in short, the formula is as follows: Ce = Rf + B x (Rm – Rf) + Cp. Ce = Cost of Equity.

Thus, as you peruse my historical data on implied equity riskpremiums or PE ratios for the S&P 500 over time, you may be tempted to compute averages and use them in your investment strategies, or use my industry averages for debt ratios and pricing multiples as the target for every company in the peer group, but you should hold back.

With these characteristics, the accounting balance sheets for these companies will be identical right after they start up, and the book value of equity will be $60 million in each company. The first is that if markets are efficient, the price to book ratios will reflect the quality of these companies.

14] Investment Company Institute, 2024 Investment Company Fact Book , at 22-23. [15] 17] See [link] (showing the United States has among the lowest equity riskpremiums in the world); Luzi Hail and Christian Leuz, International Differences in the Cost of Equity Capital: Do Legal Institutions and Securities Regulation Matter?,

Using this distinction, all interest-bearing debt, short term and long term, clears meets the criteria for debt, but for almost a century, leases, which also clearly meet the criteria (contractually set, limited role in management) of debt, were left off the books by accountants.

The logical step in looking across countries is measuring risk in countries, and bringing that risk into your analysis, by incorporating that risk by demanding higher expected returns in riskier countries. The answers, to you, may seem obvious, but I find it useful to organize the obvious into buckets for analysis.

We organize all of the trending information in your field so you don't have to. Join 8,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content